If you have a large amount of debt or are struggling to balance multiple monthly payments, debt consolidation could be an option. The process involves taking on new debt — often in the form of a personal loan — to pay off other existing debts. You can consolidate multiple accounts and monthly payments down to one, often with a lower interest rate.

Debt consolidation is a relatively simple process, but it’s good to know how it works before you apply for a loan. Additionally, there are other strategies you can use, either instead of or alongside debt consolidation.

1. Check your credit

Before applying for a debt consolidation loan — or any loan, for that matter — it’s important to know the state of your credit. You can find out your credit score, as well as if there’s anything on your credit report that could prevent you from getting a loan (for example, a debt currently in collections).

Generally speaking, you’ll have the best chance of qualifying for a debt consolidation loan — and getting the best interest rate — if you have good or excellent credit (a FICO score of 670 and above). However, some lenders offer loans to borrowers with fair (or even poor) credit.

While you’re checking your credit, now is the time to add up all of your other monthly debts, along with how much you pay on them each month. This will give you a better idea of how much you can afford to pay for your debt consolidation loan.

2. Compare lenders

With so many personal loan lenders to choose from, you should shop around to find the best option for your situation. A few things to consider when comparing lenders are:

- Loan types: Many lenders offer unsecured personal loans, but others may offer secured personal loans, home equity loans, and other borrowing tools.

- Interest rates: Rates are generally based on the current market but can still vary widely. Getting prequalified can help you find which lender will offer you the best rate.

- Repayment terms: Lenders offer a variety of repayment terms, often ranging from one to seven years. Make sure to choose a lender that offers a term you’re comfortable with.

- Fees: Common loan fees include origination fees, late fees, and prepayment penalties, but not all lenders charge them.

Credible rating

Fixed (APR)

6.99% - 25.49%

Loan Amounts

$5000 to $100000

Min. Credit Score

700

Credible rating

Fixed (APR)

7.80% - 35.99%

Loan Amounts

$1000 to $50000

Min. Credit Score

620

Credible rating

Fixed (APR)

-

Loan Amounts

$2500 to $40000

Min. Credit Score

660

Credible rating

Fixed (APR)

8.49% - 17.99%

Loan Amounts

$600 to $50000

Min. Credit Score

760

Credible rating

Fixed (APR)

8.49% - 35.99%

Loan Amounts

$1000 to $50000

Min. Credit Score

600

Credible rating

Fixed (APR)

8.98% - 35.99%

Loan Amounts

$1000 to $40000

Min. Credit Score

660

Credible rating

Fixed (APR)

8.99% - 29.99%

Loan Amounts

$5000 to $100000

Min. Credit Score

Does not disclose

Credible rating

Fixed (APR)

8.99% - 35.99%

Loan Amounts

$2000 to $50000

Min. Credit Score

600

Credible rating

Fixed (APR)

9.95% - 35.99%

Loan Amounts

$2000 to $35000

Min. Credit Score

550

Credible rating

Fixed (APR)

-

Loan Amounts

$5000 to $35000

Min. Credit Score

700

Credible rating

Fixed (APR)

11.69% - 35.99%

Loan Amounts

$1000 to $50000

Min. Credit Score

560

Credible rating

Fixed (APR)

11.72% - 17.99%

Loan Amounts

$3000 to $40000

Min. Credit Score

640

Credible rating

Fixed (APR)

-

Loan Amounts

$20000 to $200000

Min. Credit Score

660

Credible rating

Fixed (APR)

14.30% - 35.99%

Loan Amounts

$3500 to $40000

Min. Credit Score

640

Credible rating

Fixed (APR)

18.00% - 35.99%

Loan Amounts

$1500 to $20000

Min. Credit Score

540

All APRs reflect autopay and loyalty discounts where available | LightStream disclosure | SoFi Disclosures | Read more about Rates and Terms

3. Apply for a debt consolidation loan

Once you’ve narrowed down your loan options, it’s time to complete the application. For most lenders, the debt consolidation loan process is completed entirely online. Here’s how it works:

- Prepare your documents: To apply for the loan, you may need your government ID, pay stubs, proof of assets and liabilities, and more.

- Complete an online application: You’ll provide information about yourself and your financial situation to help the lender determine your eligibility.

- Wait for a response: In some cases, your loan may be approved the same day. In others, the lender will need more time to evaluate your situation.

- Receive your loan offer: Once your application is approved, your lender will let you know the approved loan amount, payment term, interest rate, and more.

4. Finalize the loan and make payments

You’ll have to sign the loan agreement (usually digitally) to finalize the loan and you’ll also have to wait to receive the funds. Depending on your lender, this could take anywhere from hours to days.

Note: It’s important to continue making your other debt payments while you wait for your loan to be processed. Any missed payments during this time could negatively impact your credit.

Finally, you’ll receive the loan funds and use the money to pay off your existing debts (or, in some cases, your lender will). At that point, you’ll only have to make the monthly payment on your new debt consolidation loan. Consider setting up automatic payments or setting a reminder on your calendar to ensure you never miss a payment.

Ways to consolidate debt

If you’re considering consolidating your debt, you have a few different options for how to do so.

Debt consolidation loan

A debt consolidation loan is most often a type of personal loan that’s used to pay off existing debt. This type of loan is usually unsecured, meaning it’s not backed by any collateral.

The good news for you is an unsecured loan doesn’t require that you put any assets at risk. However, because the lender takes on more risk, unsecured loans often have higher interest rates.

Personal loans are installment loans that usually have fixed payment terms, interest rates, and monthly payments. While the interest rate you’re eligible for depends on several factors, rates are often lower than those on credit cards.

You’ll generally need a FICO score of at least 670 to qualify, although some lenders specialize in working with borrowers with bad credit.

For example: Say you have a credit card with a $5,000 balance and a 20% APR and you make the minimum payment of $135 every month. It would take you around five years to pay off the credit card, and you’d pay a total of $2,844 in interest — more than half the original balance.

If you have good credit, you may qualify for an unsecured debt consolidation loan with an interest rate of 10% and a monthly payment of $161 per month. You’d pay off the loan in three years instead of five, and you’d only pay $808 in total interest.

If your credit score is preventing you from getting a debt consolidation loan, consider applying with an eligible cosigner or taking time to improve your credit before applying for a loan.

Balance transfer card

If you have credit card debt, a balance transfer could be an option for consolidation. Many credit card companies offer deals where you can transfer an existing balance to the card and not pay interest for anywhere from a few months to a couple of years. These introductory 0% APR offers give you time to pay off the debt without any of your payments going toward interest.

You’ll typically need a FICO credit score of 670 or higher to be eligible for a balance transfer credit card. Also, there’s typically a balance transfer fee — usually 3% to 5% of the transferred amount — which could offset any savings generated through debt consolidation. Another factor to consider is that the credit limit on the new card may not be enough to transfer all your credit card debt.

Keep in mind: Credit cards have notoriously high interest rates. If you fail to pay off the balance during the 0% intro period, you’ll start paying the card’s standard APR on your balance. Some cards even charge retroactive interest on your entire original balance if you don’t pay off the card by the end of the introductory offer period.

Also be aware that the 0% APR may only apply to balance transfers in some cases. If you use the card for other purchases, you could muddy the waters between your debt and your current spending and end up paying interest.

Check Out: Debt Consolidation Loan vs. Credit Card Refinancing: How To Choose

Home equity loan

A home equity loan allows you to borrow against the equity in your home to pay off other debt. This type of loan works similarly to a personal loan — it’s a fixed-rate installment loan with a predetermined repayment term.

A benefit of a home equity loan is that because the loan is secured by your home, you could be eligible for a lower interest rate. However, if you can’t repay the loan, you risk having your home foreclosed on. Additionally, you may have to pay closing costs like you would with any other mortgage. These types of fees are more easily avoidable with a personal loan.

Good to know: Lenders typically allow you to borrow up to 80% of your home’s equity. So, if you have $25,000 in home equity, you could borrow up to $20,000 to pay off credit cards, likely with a substantially lower interest rate than your unsecured credit cards’ rates.

Learn More: Home Equity Loan vs. Personal Loan: Which Is Right for You?

Other strategies to pay off debt

There are many other debt management strategies that you can use either instead of or alongside debt consolidation.

Utilize a debt payment strategy

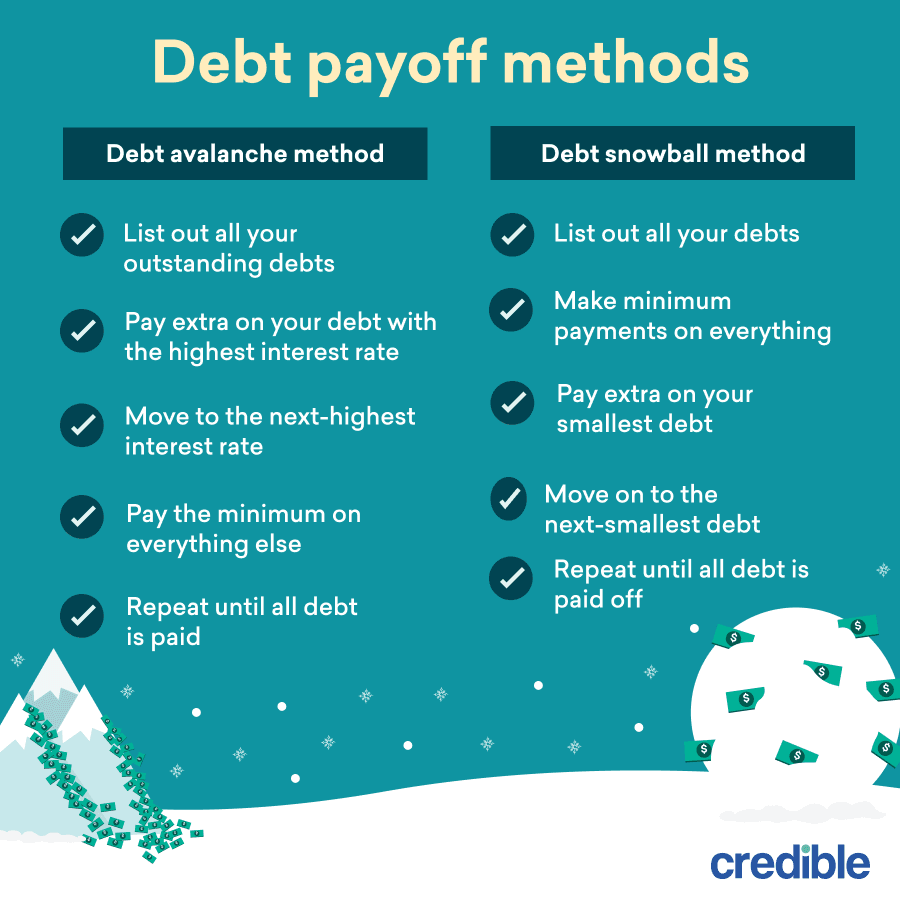

You might consider wiping out your debts with a debt payoff strategy, such as the debt avalanche method or the debt snowball method. Both these strategies may provide a viable path to eliminating your debt:

- The debt snowball method is one of the most popular debt payoff strategies. It involves making minimum payments on all your credit card accounts except one. You’ll prioritize your smallest debt, and any extra money each month goes toward paying that one off. Once you’ve paid off the smallest debt, you focus your efforts on the next-smallest debt until you’ve snowballed all of your money into one large payment that you can use for each debt. This method may be best for those who like seeing progress quickly. Paying off debt in this manner creates small wins that build momentum and motivation.

- A similar strategy is the debt avalanche method, which involves prioritizing the debt with the highest interest rate rather than the smallest debt. You pay the minimum balance on all your credit cards while paying as much as possible toward the credit card with the highest interest rate. Once you pay that credit card off in full, you add that card’s old payment to the pot and use it to pay off the credit card with the next-highest interest, and so on. This strategy can save you money in the long run since you’re paying down your high-interest debt first. However, it may take the longest to see any progress.

Finally, consider what other changes you can make to your budget to free up more money for debt. Can you increase your income, either by getting a raise or taking on additional work? Can you cut back your spending in other areas, even if it’s only temporary?

Ultimately, having a budget and knowing where each dollar is going will help you take control of your finances and be intentional about how much money you put toward debt.

Use our personal loan calculator below to estimate your monthly payments on a debt consolidation loan. Simply enter the loan amount, interest rate, and loan term to see how much you’ll pay over the life of the loan.

FAQ

How do I qualify for a debt consolidation loan?

To qualify for a debt consolidation loan, you’ll have to meet your lender’s credit score and debt-to-income ratio (DTI) requirements. While each lender has different requirements, lenders generally want to see proof that you’re able to (and likely to) repay the loan.

Can I get a debt consolidation loan with bad credit?

Yes, you can get a debt consolidation loan with bad credit. In fact, some lenders specialize in offering loans to borrowers with fair or poor credit. However, you can expect to pay a higher interest rate for this type of loan.

How can I find the best debt consolidation loan rates?

You can find the best debt consolidation loan rates by shopping around rather than applying with just one lender. Many lenders allow you to prequalify without impacting your credit score, meaning you can get rate quotes from multiple lenders. You can either prequalify individually with multiple lenders or by using an online loan marketplace. However, once you apply, the lender will perform a hard credit check, which could temporarily ding your credit. Prequalification is not an offer of credit, so your final rate could be higher than what was estimated.

Will a debt consolidation loan affect my credit score?

Yes, debt consolidation will affect your credit score. You may initially see a negative impact from the hard inquiry on your credit and the appearance of a new debt account. However, the long-term impact could be a positive one if you make your payments on time each month.

What are the alternatives to debt consolidation loans?

Some alternatives to debt consolidation loans include credit counseling, debt management plans, debt settlement, and, as a last resort, even bankruptcy. You can also use debt repayment strategies like the debt snowball or debt avalanche methods to help you prioritize your debt.

Related: Should You Pay Off Debt or Save?