Buying enough home insurance coverage is essential to minimizing your out-of-pocket expenses if your house is damaged by an unforeseen event, or peril, and you need to file a claim.

What does homeowners insurance cover?

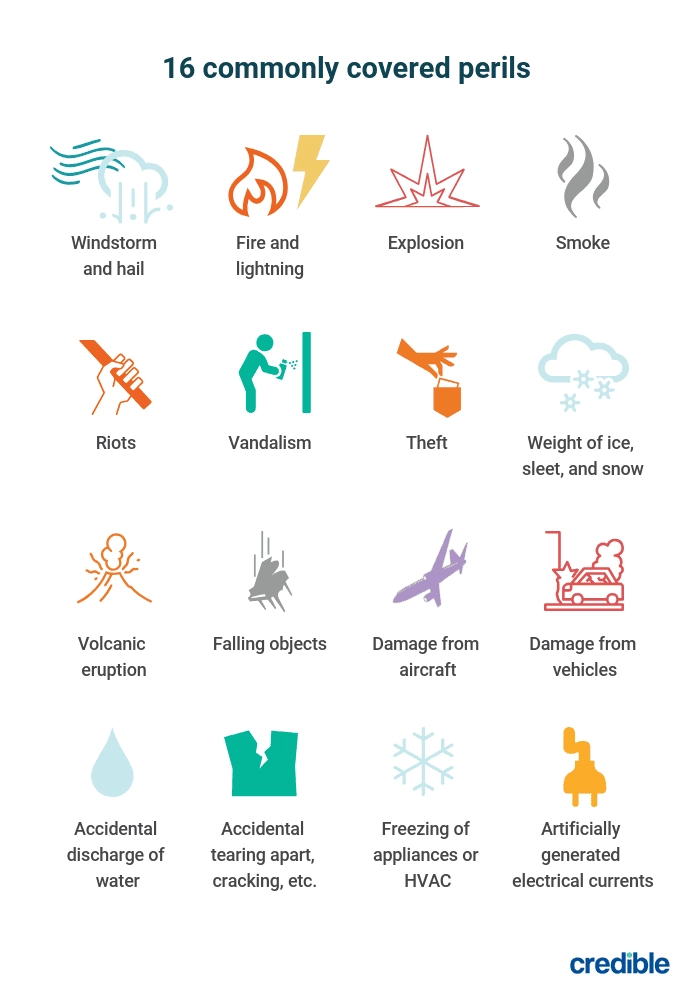

Homeowners insurance policies cover your house and personal property if perils — such as fire — cause damage or loss. A standard home insurance policy typically covers the following 16 named perils.

Here are the most common types of homeowners insurance forms:

Named perils vs. open perils

When you purchase homeowners insurance, you can choose an open perils policy or a named peril policy.

- Named peril policy: Named peril coverage only reimburses you for damage or losses from perils specifically listed in your insurance policy. Any event not listed won't be covered.

- Open perils policy: Open perils coverage reimburses you for damage or losses from all events except those specifically excluded from your policy. Insurance brokers sometimes refer to this type of coverage as "all risks" coverage.

The peril coverage you receive depends on the type of homeowners insurance you have.

For example, basic homeowners insurance (HO-1) may only cover 10 named perils instead of all 16.

Here are the most common types of homeowners insurance forms:

HO-3 coverage is the most popular homeowners insurance type, according to the National Association of Insurance Commissioners (NAIC). There are also different forms for condominium (HO-6), mobile home (HO-7), and renters insurance (HO-4). The coverage benefits are similar but are more tailored to fit the property type.

How much homeowners insurance do I need?

You should buy enough coverage to cover the full costs of rebuilding your home and replacing your belongings. In the event of a total loss, being underinsured may force you to draw on your savings or borrow money to cover the remaining costs.

If you have a mortgage, your lender will also require you to have a minimum amount of home insurance.

Your home insurance policy typically includes six different coverage types.

Dwelling coverage

Recommended coverage: 100% of your house replacement cost

Dwelling coverage is the most important benefit as it insures the physical structure of the house. While you can choose your dwelling coverage limit, strongly consider a limit that covers up to 100% of rebuilding or repair costs.

The NAIC states that if your dwelling coverage limit drops below 80% of the full replacement cost, your insurer may reduce the amount it pays you on a claim.

When estimating your replacement cost, you'll want to include the cost of building materials and labor. Look into average construction costs for the square footage of your house, and consider getting a few quotes from local builders for a more accurate estimate.

Other structures coverage

Recommended coverage: 10% of your dwelling coverage limit

Any detached structure on your property is eligible for other structures coverage. The coverage limit is usually 10% of your dwelling coverage. For instance, if you have a $350,000 dwelling insurance limit, your policy covers up to $35,000 in damage to other structures on your property.

Structures typically covered include:

- Detached garages

- Fences

- Gazebos

- Guest houses

- Storage sheds

- Swimming pools

Structures attached to your house — such as a deck or porch — are covered under your dwelling insurance.

Personal property coverage

Recommended coverage: 50% to 70% of your dwelling coverage limit

Personal property coverage will pay to repair or replace your personal belongings if they're stolen or destroyed by a covered peril. It's typically between 50% and 70% of your dwelling coverage limit. Many belongings in your house are eligible.

Consider making a home inventory list for these items:

- Appliances

- Clothing

- Decorations

- Electronics

- Furniture

- Jewelry

High-value items such as fine jewelry, artwork, and collectibles may qualify. However, the coverage limits can be less than your property's full value. If you own items like these and want more protection than what your current policy offers, you may need to add a personal articles floater — also known as scheduled personal property coverage — to your existing policy.

Tip

Taking pictures and keeping paper records of your possessions can make it easier to claim reimbursement.

Loss of use coverage

Recommended coverage: 20% of your dwelling coverage limit

When you can't live in your house due to damage from a covered peril, loss of use coverage — also known as additional living expenses (ALE) insurance — can reimburse you for reasonable housing, meal, and storage costs. It's usually 20% of your dwelling limit.

Personal liability coverage

Recommended coverage: Between $100,000 and $500,000

Personal liability insurance covers you if you are sued because of an accident resulting in bodily injury or property damage. Liability coverage may also cover incidents stemming from pets, such as if your dog bites someone at the park.

Liability coverage can reimburse you for these expenses:

- Legal fees if someone sues you

- Lost wages of someone injured at your house

- Repair bills for others' property damage

Your insurance policy may let you choose your coverage amount. Liability coverage limits typically start at $100,000. However, this might be insufficient for an expensive lawsuit. Consider carrying between $300,000 and $500,000 of liability coverage, or as much as you can afford. If you want more coverage, consider umbrella insurance.

Medical payments coverage

Recommended coverage: $5,000

Medical payments coverage pays small medical bills for guests injured on your property. It doesn't cover medical payments for your injuries or injuries to any family members living with you.

Most insurance carriers let you choose between $1,000 and $5,000 of coverage. So, if you elect the maximum $5,000 benefit, you'll be responsible for paying the remaining balance on any medical bills that exceed $5,000.

Compare home insurance from top carriers

- Fully digital experience — Fill out all of your insurance forms online, no phone call required!

- Top-rated carriers — Choose from a mix of highly reputable national and regional home insurance carriers.

- Data privacy — We don’t sell your information to third parties, and you won’t receive any spam phone calls from us.

Replacement cost coverage

In addition to coverage limits, you have a few options when it comes to reimbursement. You can insure your home and personal property for actual cash value or replacement cost value, and you can even upgrade to extended replacement cost coverage or guaranteed replacement cost coverage.

Here's a look at each of these coverage types:

- Actual cash value: An actual cash value (ACV) policy reimburses you for the cost to replace your damaged or stolen property, minus depreciation. This means you'll receive a payout for the item's current value, not what it was worth when you first bought it. An actual cash value policy provides less coverage, but it also costs less than replacement cost coverage, so you may want to purchase ACV if you're on a tight budget.

- Replacement cost: A replacement cost value (RCV) policy pays the cost to replace or repair your home and personal belongings, up to your policy's limit, without deducting for depreciation. If a covered peril damages your sofa, replacement cost coverage will pay for a new sofa of similar quality at today's prices.

- Extended replacement cost: You may also be able to purchase extended replacement cost coverage, which increases your replacement cost by 25% to 50%. This coverage is designed to help cover rising construction and material costs, and can offer more peace of mind.

- Guaranteed replacement cost: This policy pays to replace or repair your home and personal belongings even when costs exceed your policy limits. This is the highest level of coverage and generally the most expensive option.

Homeowners insurance exclusions

Not every event or mishap occurring on your property is covered under your home insurance policy. Some common home insurance policy exclusions are:

- Flood damage or a sewer backup

- Earthquakes, mudslides, and sinkholes

- Neglect or intentional loss

- Legal ordinance or government action

- War

It's possible to purchase separate flood insurance and earthquake insurance policies to cover these exclusions.

Other exclusions might be non-insurable. For example, when the peril stems from building code noncompliance or neglected maintenance.

Additional coverage you may need

While your homeowners insurance policy covers many situations, you might need additional coverage for peace of mind. In some cases, you can add endorsements to your home insurance instead of buying a separate product.

Flood insurance

Most home insurance policies don't cover damage caused by flooding. Instead, you can purchase a separate flood insurance policy.

If you live in an area prone to flooding, your mortgage lender may require that you carry flood insurance.

Earthquake insurance

Most insurance policies don't cover damage from earthquakes unless you add an endorsement or purchase a separate policy. Basic earthquake insurance includes dwelling coverage, personal property coverage, and loss of use coverage.

Personal articles floater

If you have any luxury items, the coverage limits are likely lower than your standard personal property coverage limits.

A personal articles floater, or rider, supplements your home insurance for valuables like:

- Antiques

- Cameras

- Fine art

- Jewelry

- Musical instruments

- Watches

- Wedding rings and engagement rings

This policy may require a verified home inventory and professional appraisal to activate coverage. A personal articles floater only insures items individually listed in the policy.

Tip

Alternatively, you can add a broader valuable items endorsement that covers damages or losses in a specific category. For example, you may be able to add an endorsement to cover all your jewelry.

Alternatively, you can add a broader valuable items endorsement that covers damages or losses in a specific category. For example, you may be able to add an endorsement to cover all your jewelry.

Home business coverage

Homeowners insurance may provide limited coverage for home-based businesses, such as up to $2,500 in business equipment. You might be able to add an endorsement to increase the limit to $10,000.

However, you'll need to purchase a separate business insurance policy for additional liability and equipment protection. A standalone policy may also be necessary if you operate in a business with many customers or additional risks.

Identity theft

Your basic home insurance may only cover the theft of physical items and not your personal information. You might be able to add identity theft protection to your homeowners policy.

Identity fraud protection can cover these expenses:

- Identity and credit restoration services

- Replacement of government-issued IDs

- Lost wages

- Travel expenses

- Attorney fees

Cyber insurance

If you run a home business, cyber insurance can protect you in the event of a data breach or other cyber crime. Your benefits can pay for restoration and recovery services to make your devices safe and function properly again.

Umbrella insurance

An umbrella policy provides financial protection beyond your personal liability coverage limit. It can offer liability coverage for legal defense costs, property damage, and even claims like libel and slander.

How to get homeowners insurance quotes

It only takes a few minutes to request a free homeowners insurance quote with Credible Insurance. You can easily compare home insurance quotes and coverages from several insurance carriers from your area.

Compare home insurance from top carriers

- Fully digital experience — Fill out all of your insurance forms online, no phone call required!

- Top-rated carriers — Choose from a mix of highly reputable national and regional home insurance carriers.

- Data privacy — We don’t sell your information to third parties, and you won’t receive any spam phone calls from us.

Copyright (c) 2023, Credible Insurance, Inc. d/b/a Credible Insurance Agency (CA Lic. # 0M90597). Insurance Services provided through Credible Insurance, Inc., VA: Credible Insurance Agency, Inc., MN SOS: Credible Cover, Inc. Credible Insurance is a subsidiary of Credible Labs Inc. 1700 Market St. Ste. 1005, Philadelphia, PA 19103.