High mortgage rates and rising home prices are two of the primary factors making it more difficult for Americans to afford a home. At the same time, housing expenses comprise more than just a monthly mortgage payment, and prospective buyers don’t always know what to expect when budgeting for homeownership.

A Credible survey asked more than 1,000 homeowners how their housing costs compared to their budget expectations. Most respondents underestimated the true cost of homeownership, and the majority thought first-time homebuyers don’t get enough education about homeownership costs.

Americans are paying nearly $5,000 more per year for homeownership than expected

More than 60% of homebuyers spend more than they expected on homeownership. First-time homebuyers were especially likely to feel like they're in over their heads. For many, homeownership has caused financial stress, and housing costs get in the way of other financial goals, like saving for retirement.

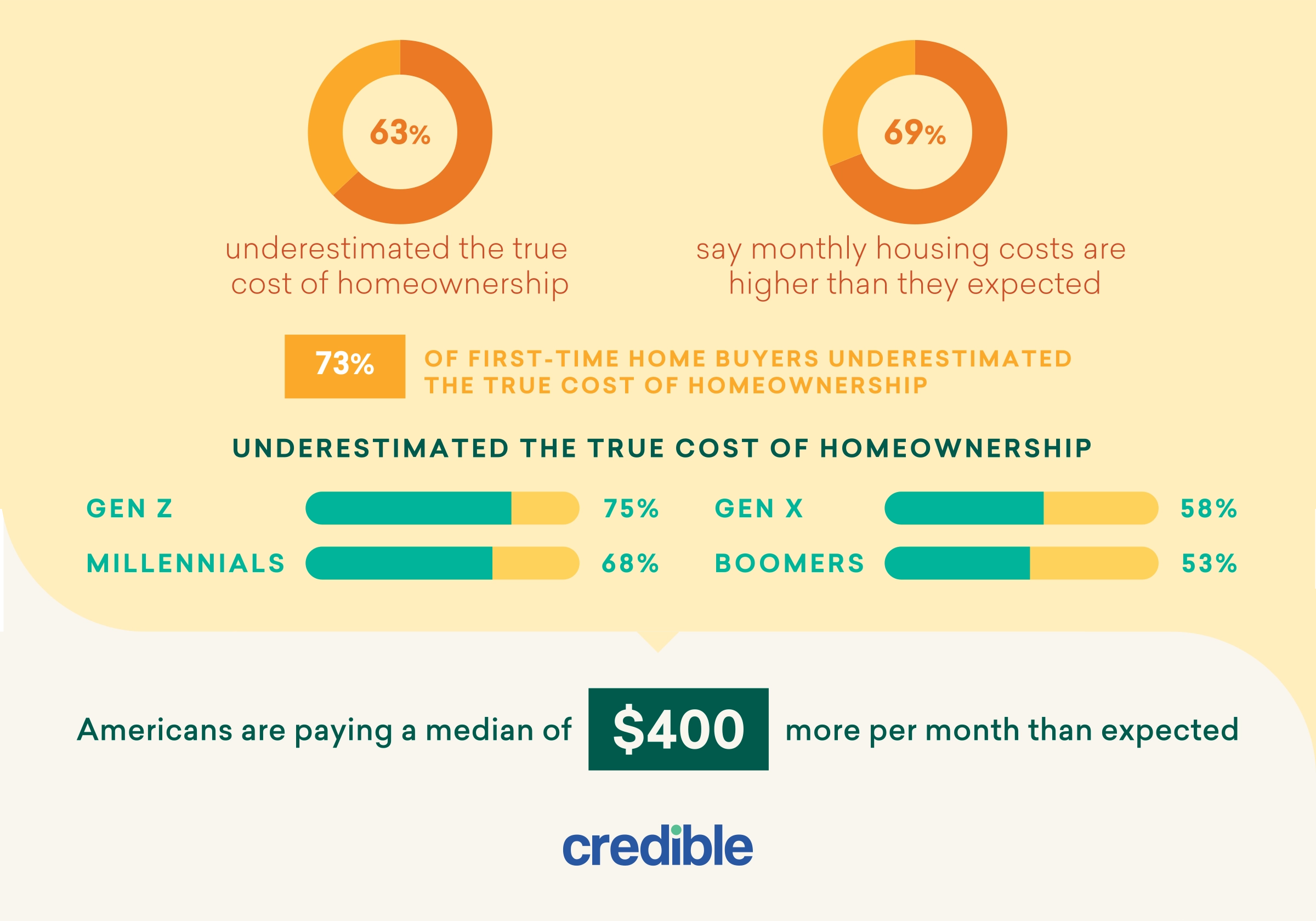

Sixty-three percent of Americans underestimated the true cost of owning a home, including 73% of first-time homebuyers. And they’re paying a median of $400 more per month than expected.

The disconnect between expectations and true costs was especially common among younger generations. Gen Z homeowners were more likely than other respondents to say they underestimated costs (75%), compared with 68% of millennials, 58% of Gen X, and 53% of baby boomers.

Women (65%) were more likely than men (61%) to underestimate the true cost of homeownership.

Commonly overlooked expenses

When budgeting for homeownership, one common pitfall is to focus on the monthly mortgage payment and ignore other property expenses, such as:

- Property taxes

- Homeowner’s insurance, flood insurance, and earthquake coverage

- HOA fees

- Utility bills

- Maintenance and repairs

In fact, 37% of respondents said they currently live with an inconvenience because a home repair is too expensive. That share increases to 42% for first-time home buyers.

Note

More than a third of homebuyers were unprepared for a mishap like an HVAC breakdown or leaky roof — 35% reported they don’t have an emergency fund for home-related problems.

Another mistake is estimating costs based on a mortgage rate you think you might qualify for, without revising your budget to account for your actual rate. Even a small increase in your mortgage interest rate can have an impact on your monthly housing expenses.

For example, if you bought a $500,000 home with a 20% down payment and had a 30-year fixed-rate mortgage, your estimated monthly payment (principal and interest only) with the following interest rates would be:

- 6%: $2,998

- 6.5%: $3,160

You can use a mortgage calculator to understand how your final rate offer affects your monthly payment.

The impact of housing inflation

In recent years, many homebuyers have had another factor to contend with: home prices approaching historic levels relative to income. A study by Harvard University's Joint Center for Housing Studies found that nationwide, median single-family home prices increased 48% between 2019 and 2024 while the median income rose at a rate of just 22%. The study points out that rising price-to-income ratios make affording a home particularly challenging for low- and moderate-income families.

Rising home prices have also made it more difficult for prospective homebuyers to save for a down payment. Twenty-four percent of those surveyed used a first-time homebuyer program to help purchase their home. But the financial strain doesn’t end at closing.

Homeowners who bought in the past four years reported median mortgage payments of around $1,800 to $2,100, compared with $1,200 among those who bought more than 10 years ago and still have a mortgage.

The best defense against budget stress in today’s high-cost environment is careful planning, according to Todd Christensen, housing counseling and education manager at MoneyFit.

“My advice is to reach out to a HUD-approved housing counseling agency from day one, even before you start browsing listings. A counselor can help you clarify your goals, build a realistic budget, assemble a team of trusted professionals, identify down payment assistance programs and grants you may not know exist, and help you stay accountable to your own priorities,” says Christensen.

More than 3 in 5 homeowners say the cost of owning a home causes financial strain

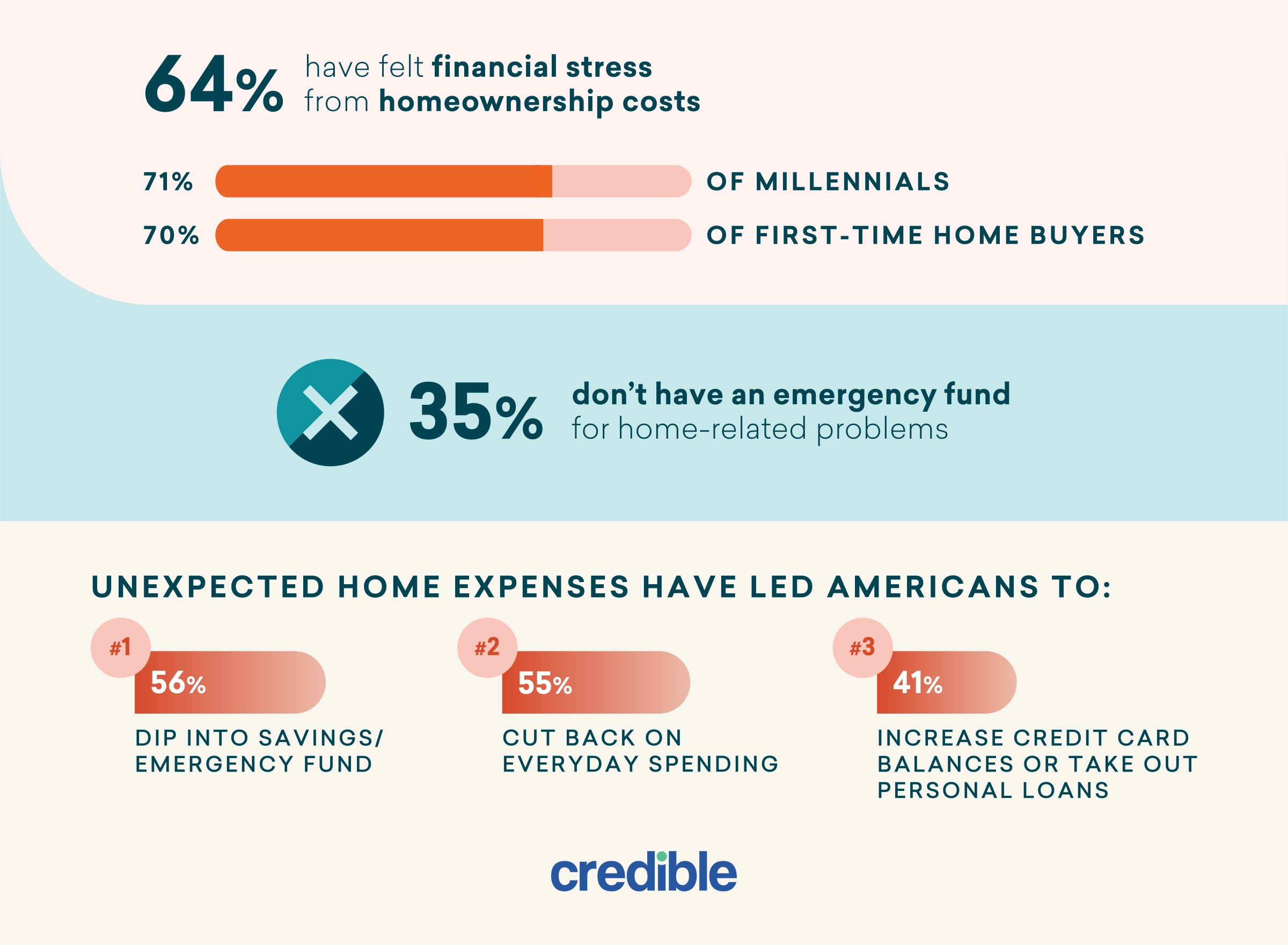

While owning a home can be a source of security and satisfaction, 64% of respondents said homeownership costs have caused them financial stress. Women (69%) were more likely to report financial stress from homeownership costs than men (59%). Millennials (71%) and first-time homebuyers (70%) were especially likely to say homeownership costs were a cause of financial stress.

For many homeowners in the survey, housing expenses have impeded their progress toward other financial goals. Homeowner costs have affected the ability to:

- Save for emergencies (50%)

- Pay off debt (47%)

- Save for retirement and travel (45%)

In addition to dipping into savings or an emergency fund (56%), unexpected home expenses have led many of the survey respondents to:

- Cut back on everyday spending (55%)

- Increase credit card balances or take out personal loans (41%)

Over a third of respondents did not have an emergency fund. And among those who do, only 38% can cover three to six months' worth of expenses. That means if the primary income-earner loses their job, the household could quickly become at risk of defaulting on mortgage payments. Missed payments can lead to late fees, damage to your credit score, and even foreclosure.

“One way to manage costs is to put aside money for maintenance and repairs every year,” says Barry Bridges, personal loans editor at Credible. “One commonly cited rule of thumb is to budget 1% to 4% of your home's value on an annual basis. You can lean toward 1% if your home is newer and closer to 4% if it has a few decades of wear and tear. You don't have to set up a special designated fund — you can just feed the money into your checking, savings, or money market account and maybe even earn a little interest.”

38% of homeowners consider themselves house-poor

A person is considered “house-poor” when they spend a large share of their monthly income on housing costs or when their monthly mortgage payment leaves them so cash-strapped that they can’t keep up with other necessary expenses. The term “house-poor” is subjective, and homeowners may be more likely to feel house-poor in areas with a high cost of living.

Note

“Cost-burdened” is a similar term with a precise definition. The U.S. Department of Housing and Urban Development defines “cost-burdened” as a household with monthly housing costs, including utilities, greater than 30% of its gross monthly income.

More than half of the homeowners in the survey said they put at least 30% of their income toward their total housing costs, which would meet HUD's definition of cost-burdened.

- 30% of homeowners said 40% of their income or more goes toward housing expenses

- 22% of homeowners said they spend between 30% and 35% of their income on housing

Only 35% of homeowners said 29% or less of their income goes toward their total housing costs. While these respondents may be in a better financial situation than their peers, they’re not impervious to financial strain.

Christensen warns not to assume you can afford a home just because you get an approval letter from a mortgage lender. “Too many homebuyers simply accept whatever a lender tells them they can afford. Affordability should be buyer-driven, not lender-driven. Once you add property taxes and the true cost of ownership, a lender's approval number can leave a family stretched dangerously thin.”

Homeownership education gap leaves many buyers unprepared

Many Americans buy their first home without receiving the education they need to prepare for the financial burden of homeownership. For example, former renters accustomed to landlords taking care of repairs and maintenance can lack awareness of how much it costs to handle it on their own.

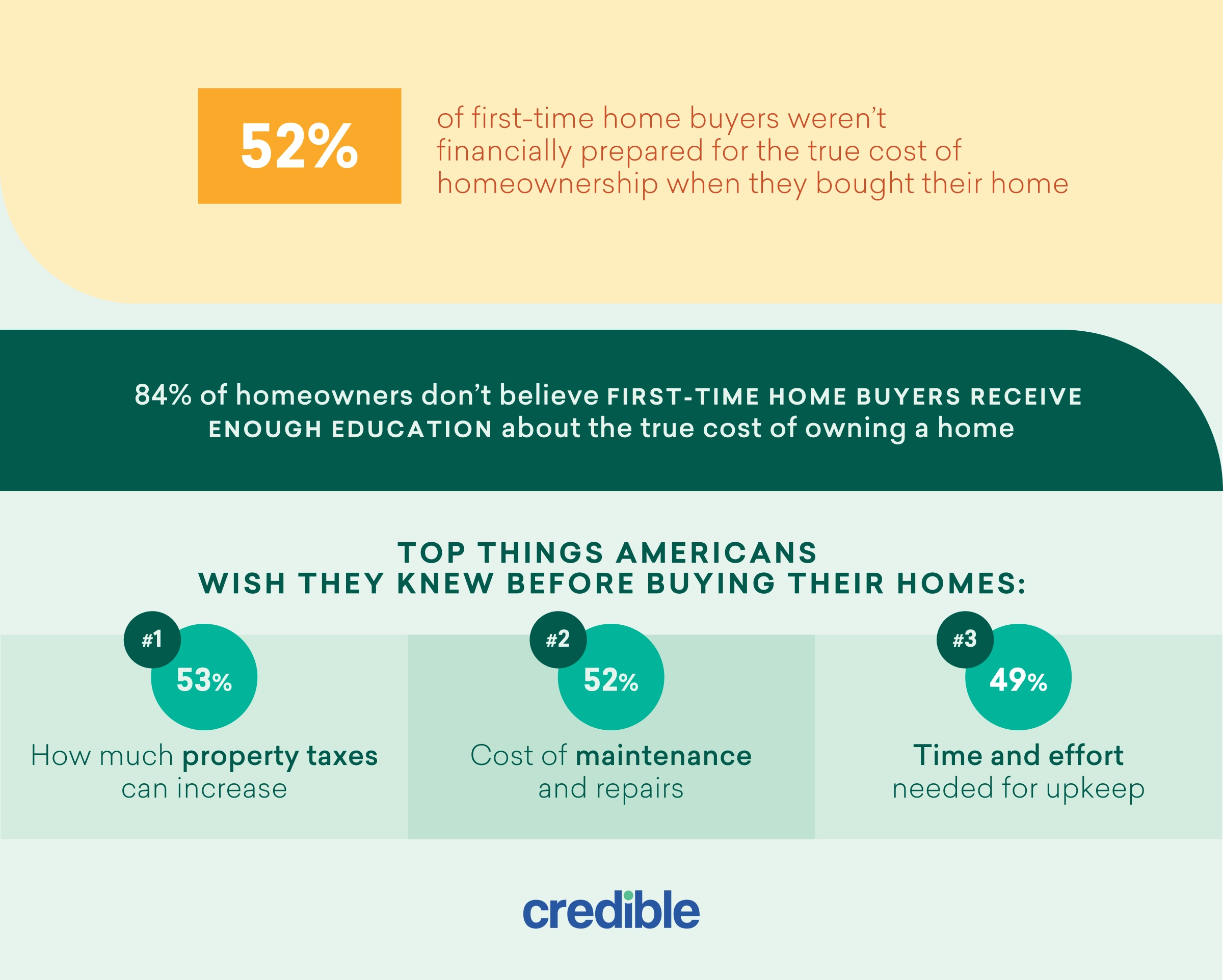

And more than half of respondents (53%) said they wish they’d known how much property taxes could increase. While a rapid increase in home values is a good opportunity to build home equity, it can also mean a larger tax bill each year, depending on state and local property tax laws. The cost of maintenance and repairs (52%) and the time and effort required for upkeep (49%) were other top items homeowners wished they’d known more about.

Nearly half of homeowners ended up with more financial responsibility than they bargained for — 44% of respondents said they weren’t financially prepared for the true cost of homeownership when they bought their home. The share jumps to 52% among first-time homebuyers.

Insufficient counseling or education may be partially to blame. The vast majority — 83% of respondents — think first-time buyers don’t get enough support in that area. More than half said they learned about homeownership from family and friends or online research, but formal education from a housing counselor may be necessary to close the education gap, especially for first-generation homeowners or folks working with a tight budget.

How surveyed homeowners learned about homeownership costs before buying:

- From family/friends (34%)

- From online research (24%)

If prospective buyers focus their research on the home purchase process, they might miss out on important information about homeownership costs that can arise after closing.

For instance, an expensive home repair early on in the mortgage term can be devastating for homeowners who devoted their savings to upfront homebuying costs. Forty-seven percent of respondents had to replace a major appliance or system within the first year of homeownership, and 64% didn’t have a home warranty to help cover certain types of unexpected costs.

“A home warranty can be a boon for a first-time homebuyer, especially if it's included in the sale as a perk, but keep in mind that they're essentially service contracts for appliances, HVAC systems, and other items,” says Bridges. “The drawbacks can include duplication of existing warranty or insurance coverage, limits on reimbursements, complicated claims processes, and hidden costs like fees and deductibles. If your appliances and systems are relatively new and you maintain a robust emergency fund, a home warranty might be an unnecessary expense.”

Repairs and renovations top list of higher-than-expected homeowner costs

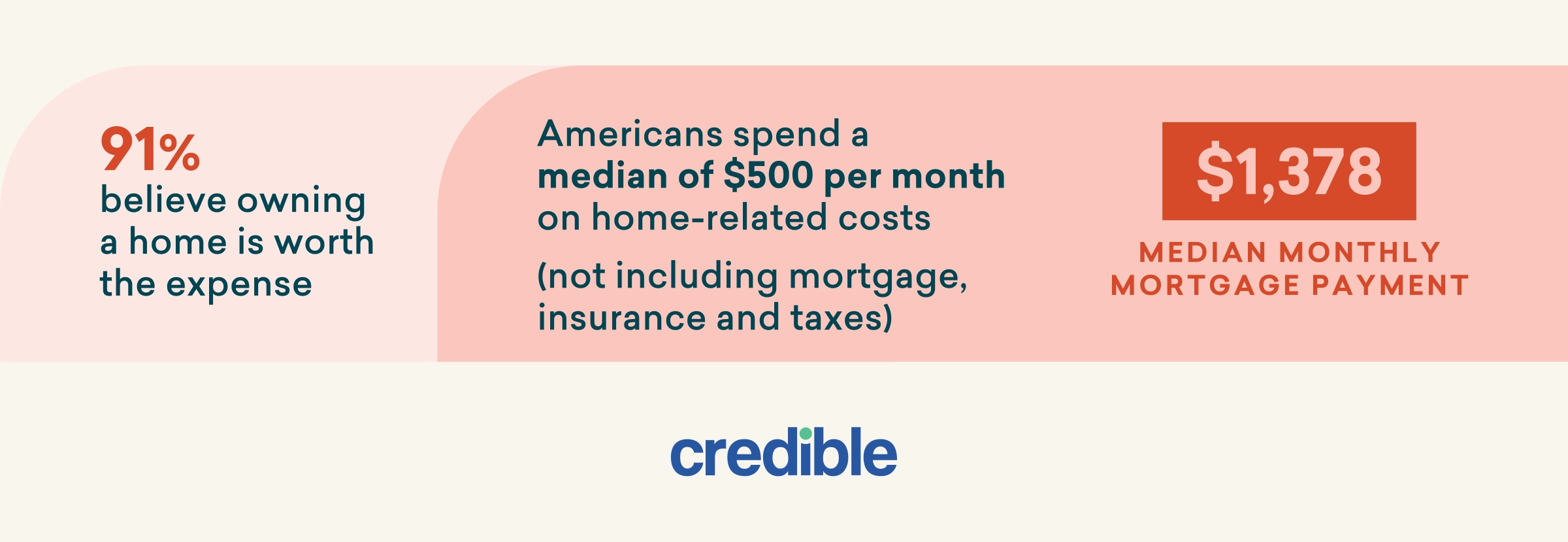

Housing costs tended to exceed what survey respondents expected to spend when shopping for a home. Repairs and renovations were the most common expenses that caught them by surprise, but property taxes and homeowners insurance were also unexpectedly expensive. Still, more than nine out of ten said that owning a home is worth the cost.

Respondents spend a median of $500 per month on home-related costs (not including mortgage, insurance, and taxes). Their median monthly mortgage payment is $1,378. Most commonly, respondents said the following home-related expenses gave them sticker shock:

- Repairs – 64%

- Renovations – 53%

- Property taxes – 52%

- Homeowners insurance – 49%

- Utilities – 47%

- Maintenance – 46%

- Closing costs – 34%

- Monthly mortgage payment – 32%

- Private mortgage insurance – 21%

When budgeting for homeownership, ensure you account for annual increases in expenses like homeowners insurance and utilities. “One of the best ways to offset the rising cost of homeownership is preparing intentionally,” says Landy Liu, CEO of Foyer, a homeownership platform. “A good rule of thumb is to have at least 1% of your home's price saved annually for unforeseen expenses."

Good to know

A Pew Research study found that 71% of homeowners reported increases in home insurance premiums over the last few years, and the U.S. Government Accountability Office found that home insurance rates have increased by 25% or more in some disaster-prone areas in recent years.

Despite the costs and potential financial strain of homeownership, owning a home offers many benefits. Owning a home can allow you to build home equity, which can be a financial resource in a time of need and a way to pass on wealth to future generations. You can enjoy certain tax benefits as a homeowner, including some deductible house-related expenses, and you have more freedom to do what you want with your property than when you rent.

Methodology

In May 2026, Credible commissioned Digital Third Coast and Prolific to conduct a survey of 1,005 homeowners ages 19 to 80 from across the U.S. Among respondents, 49% identified as male, 50% as female, and 1% as non-binary/rather not say. The respondents represented 48 states, plus Washington, D.C., and had a median age of 44.

For media inquiries, contact [email protected].

Fair use

When using this data and research, please attribute it by linking to this study and citing Credible.