While owning a home is a big step that requires high upfront costs, there are plenty of long-term advantages that aren’t always obvious. Aside from getting a place to call home, buyers also build equity, have predictable housing payments, and enjoy several other perks.

1. More stable housing costs

Buying a home comes with a lot of upfront expenses, including the down payment and closing costs. There are plenty of ongoing maintenance costs to consider, too.

But with a fixed-rate loan, one homeownership cost remains consistent: the monthly payments on your mortgage. Even if the costs of property taxes and homeowners insurance increase over time, your housing payments will remain relatively stable from year to year.

Meanwhile, renters have to deal with potential price increases every time they renew a lease or find a new apartment.

2. An appreciating investment

Home appreciation is a moving target that’s largely based on local market trends. But generally, home prices increase over time — providing one of the major benefits of owning a home.

According to a report by mortgage data firm Black Knight, the 25-year average appreciation rate of homes in the U.S. is 3.9% per year.

For example

If you buy a home today worth $200,000 and it increases in value by 3.9% annually, your home would be worth about $233,073 after five years.

Of course, home values vary widely in every corner of the U.S. and may fluctuate more during some years compared to others. You can use the U.S. Federal Housing Finance Agency’s House Price Calculator to estimate your home’s current value based on your closing date and purchase price.

3. Opportunity to build equity

Your home equity is the portion of your home that belongs to you, calculated by subtracting your mortgage balance from the home’s market value. There are two ways to build home equity:

- Make your monthly mortgage payments

- Track your home’s appreciation over time

You receive that home equity as cash when you sell your home. Renters, on the other hand, won’t recoup any housing costs they spent while living in their homes.

Take a look at one example of how you might come out ahead with buying rather than renting:

- Buying a house: You put down 20% on a $200,000 home with a 3% interest rate and a monthly principal and interest payment of $872. Five years later, you sell the home for $220,000. After paying off the mortgage balance, you get to keep $77,713. That dollar figure comes from your down payment ($40,000), the principal payments you made ($17,713), and the value appreciation ($20,000).

- Renting an apartment: You’re not sure about your career plans, so you rent a great apartment at $870 a month instead of buying a house. At the end of five years, you’ve spent $52,200 on rent payments — and you receive none of it back when you move out.

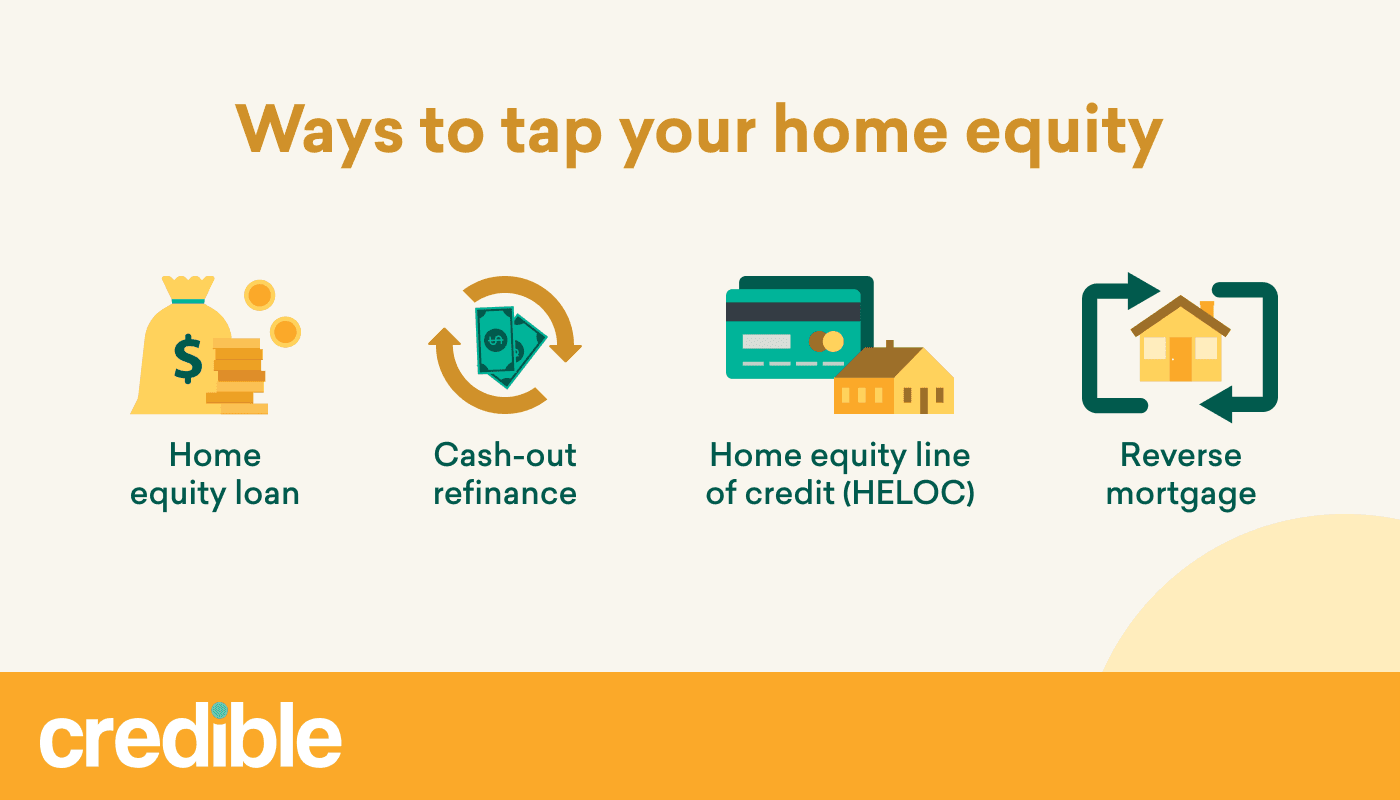

4. A source of ready cash

Another benefit of owning a house is that you can tap your equity to help fund home improvements or pay off personal debt.

With the following options, you can borrow money and use your home as collateral. While this could put your home at risk if you fall behind on payments, these options could be cheaper than some alternatives.

Here’s a more thorough breakdown of what each option entails:

Home equity loan

This is a second mortgage. You receive a lump sum of money upfront, then pay it back in installments over several years.

How much can you borrow? Around 85% of the equity in your home.

Home equity line of credit

Also, a second mortgage, a HELOC, provides access to a line of credit. You can borrow from the line of credit anytime during a “draw period.” When that period ends, you have a certain amount of time to pay down the balance.

How much can you borrow? Around 75% to 85% of the value of your home, minus your mortgage balance.

Cash-out refinance

You take out a new mortgage for more than you currently owe, use the proceeds to pay off the original loan, cover closing costs, and pocket the difference.

How much can you borrow? About 80% of your home’s total value, less whatever you still owe on your mortgage.

Reverse mortgage

Homeowners who are at least 62 years old can apply for this type of loan. Once you receive the money, you’ll pay off your mortgage balance and use the remaining funds as you see fit.

The loan is repaid when you die, sell the home, or move out.

How much can you borrow? The amount is based on the equity you have in your home.

5. Tax advantages

There are tax advantages to owning a home, too. From mortgage interest deductions to capital gains, these may help you save money each year.

Mortgage interest deduction

Through the 2023 tax year, you can deduct any mortgage interest you paid on your federal income tax return.

To take the tax break, you’ll need to itemize your deductions on Schedule A. Your state may also offer a deduction.

Dollar limit: Deduct mortgage interest paid on the first $750,000 ($375,000 if married filing separately) for mortgages taken out after Dec. 17, 2017; for mortgages taken out before that date, you can deduct interest paid on up to $1 million ($500,000 if married filing separately).

Mortgage insurance premiums

As of 2022, you can no longer deduct money paid toward mortgage insurance premiums on your federal income tax returns.

Property tax deduction

If you itemize on your federal tax return, you may deduct property tax payments, local income taxes, and sales taxes you paid to your state and local governments.

Dollar limit: Up to $10,000 per year ($5,000 if you’re single or married filing separately).

Capital gains

If you make a profit when selling your home, you might not have to pay taxes on the earnings. You’ll need to show you lived in your home for at least two out of the five years before selling.

Dollar limit: Eligible homeowners can exclude up to $500,000 in profits on their federal income tax returns (up to $250,000 for single filers or married couples filing separately).

Learn More: First-Time Homebuyer Tax Credits: Everything You Need to Know

6. Helps build credit

Taking out a mortgage can positively impact your credit, which is an important part of your financial health. Making on-time payments every month could help improve your credit scores, while simply having a mortgage could help you diversify your credit mix and increase the length of your credit history.

Your credit utilization also decreases as you reduce your loan balance, which positively influences your credit scores.

Keep in mind: Late payments will hurt your credit, and if the default leads to foreclosure, your credit score could take a dive.

So if you’re taking out a mortgage to buy a home, prioritize making timely payments. You’ll build credit over time, which allows you to finance future purchases at favorable rates.

7. Freedom to personalize

Owning a piece of property gives you almost complete control over the projects you want to take on. As long as those home improvements follow local laws, you can renovate and update the home to your liking. This is one of the major benefits of buying a home that renters can’t enjoy.

If you’re ready to take out a mortgage, learn about how to get a pre-approval and find out how much you can afford.