A prepayment penalty is a fee you might incur if you pay off your mortgage early. Mortgage lenders rely on interest payments over the life of the loan to generate revenue, and some loan agreements contain prepayment penalties to protect the lender’s profits against homeowners who sell or refinance after only a few years.

But most consumer mortgages don’t have prepayment penalties. Some government-backed loan programs prohibit them, federal law limits them on most conventional loans, and you can avoid prepayment penalties entirely if you know what to look for. We’ll cover everything you need to know about prepayment penalties to help you choose a mortgage lender that won't penalize you for paying early and saving money on interest.

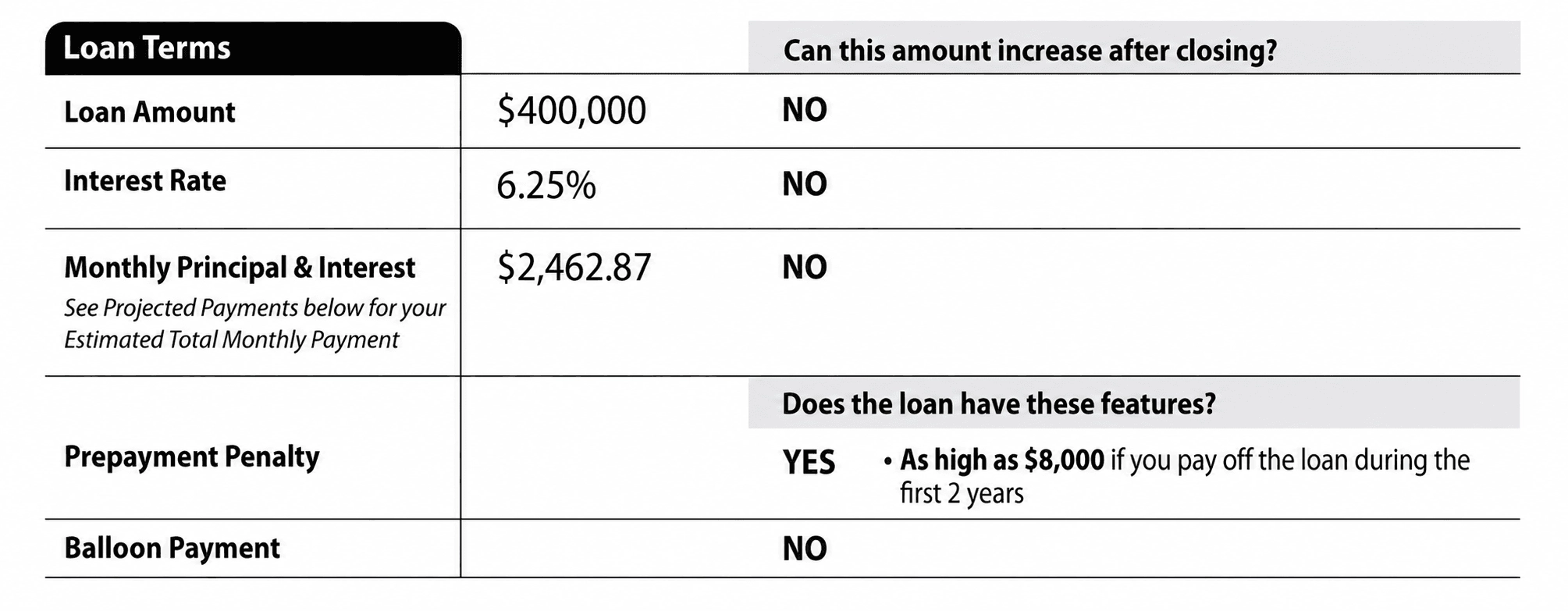

What is a prepayment penalty?

When you sign a mortgage agreement, you agree to repay the loan balance with interest over a specific term. Some mortgage lenders charge a prepayment penalty if you repay the entire balance early within a certain number of years — for example, by selling your home or refinancing. In other cases, a prepayment penalty could apply if you pay off a large amount of your balance with a single payment.

Some other types of loans can also include prepayment penalties, but in most cases they're increasingly rare. For example, very few personal loan lenders charge prepayment penalties.

Mortgage prepayment penalties are uncommon among traditional lenders. “Most standard mortgage products, including conventional and government-backed loans, do not include prepayment penalties,” says Jeff Grove, mortgage loan officer at DFCU Financial in Florida. If your mortgage does have a prepayment penalty, the lender is legally required to disclose the fee.

But Grove says you should still take steps to verify that your loan agreement doesn’t contain a prepayment penalty:

- Check with your loan officer prior to applying.

- Review your Loan Estimate, a legally required document you receive after applying for a mortgage that details estimated loan costs, including any prepayment penalties.

- Confirm there isn’t a prepayment penalty on your Closing Disclosure or promissory note before signing.

What are the types of prepayment penalties?

There are two main categories of prepayment penalties. The table below shows how they compare.

How is a prepayment penalty calculated?

Lenders typically calculate prepayment penalties in one of three ways:

- Percentage of outstanding balance: Some lenders charge a percentage of your remaining loan balance, such as 1% or 2%.

- Months of interest: Some lenders charge a certain number of months’ worth of interest charges you would have paid if your loan remained outstanding.

- Step-down structure: Some lenders establish a tiered or sliding scale fee structure, so that the penalty grows smaller the further you get in the loan term. For example, you could owe 2% of the remaining loan balance if you prepay the loan within the first year but only 1% if you prepay in the second or third year.

Federal law prohibits prepayment penalties on some mortgage types and caps the amount on others. Prepayment penalties are prohibited for certain government-backed loans, such as VA loans, USDA loans, and FHA single-family mortgages.

Conventional mortgages from private lenders, including fixed-rate and adjustable rate mortgages, can have prepayment penalties, but they typically need to meet certain legal requirements such as:

- The penalty can’t apply after year 3 of the loan term.

- The penalty can’t exceed 2% of the outstanding loan balance if charged in the first 2 years or 1% of the outstanding loan balance if charged in the third year.

In addition, lenders that charge prepayment penalties are required to offer an alternative loan option that doesn’t include the penalty.

However, you may not have the same protections with certain types of commercial mortgage loans, like a loan for an investment property.

When does a prepayment penalty apply?

Prepayment payment penalties are uncommon among most conventional mortgages, but you should check with your lender before making an early payment. “Some non-traditional, investor, and portfolio loan products carry prepayment penalties, and those can be steep,” says Frederick Blum, broker and owner at Blum Realty Group of the San Diego area.

If your mortgage does have a prepayment penalty, you’ll likely be charged the fee only if you repay the entire mortgage balance, whether through a lump sum payment, selling, or refinancing, within a certain time period. For consumer mortgages covered under Regulation Z of the Truth in Lending Act (TILA), a prepayment penalty can’t apply for more than three years from the consummation date.

Your loan servicer is unlikely to penalize you for making small extra payments on your mortgage. But that doesn’t necessarily mean they’ll make it easy for you to make extra payments toward your principal balance faster, according to Blum.

“Loan servicing companies are not incentivized to facilitate early payoffs for the borrower, as once the loan is paid the income from that loan ceases,” says Blum. “Importantly, I always advise borrowers to get confirmation from the loan servicer in writing that any extra payment will be applied purely to the principal loan balance.”

How do you avoid a prepayment penalty?

The best way to avoid a prepayment penalty is to avoid taking out a home loan that has one. Check the Loan Estimate and Closing Disclosure sections of a loan agreement before signing to make sure it doesn't stipulate a prepayment penalty. There are plenty of mortgage products that offer the flexibility of early repayment, so compare options before applying.

If you already have a mortgage, make sure you’re well informed before you make any financial decisions. “If your loan includes a prepayment penalty, review the terms carefully so you understand what actions could trigger it and avoid those situations,” says Grove.

FAQ

Do all mortgages have prepayment penalties?

Open

How do you find out if your mortgage has a prepayment penalty?

Open

Can you negotiate a prepayment penalty with your lender?

Open

Does making extra mortgage payments trigger a prepayment penalty?

Open