The average community college tuition and fees for in-state students totaled $4,150 for the 2025-26 academic year, according to the College Board. That's less than half the $11,950 average at public four-year schools for in-state students. This affordability makes community college an accessible choice for many students.

Finding the right loan for college students starts with federal student loans, which are usually the best first choice, offering low, fixed rates and key borrower protections. Private student loans can fill the gap when federal loans don't cover all your college costs. Although not all lenders offer student loans for associate degree programs, many do.

College Ave, Sallie Mae, Ascent, and Custom Choice stand out among the best lenders in the Credible marketplace for helping students pay for community college due to their competitive rates, no-fee policies, and flexible repayment plans.

Compare current private student loan rates

Can I get student loans for community college?

You can get both federal and private student loans for community college.

To qualify for federal loans, your school must participate in the federal student aid program, which most community colleges do. You also need to be enrolled at least half-time. This means many students in standard two-year programs qualify, while part-time students typically don’t.

Private student loans for community college are also an option. However, these loans often come with higher interest rates and fewer protections. They don’t offer federal benefits like income-driven repayment plans or loan forgiveness programs.

What to watch out for

Federal student loans do have annual and lifetime borrowing limits, but they’re often enough to cover in-state community college tuition in many states. Try to avoid taking out higher-interest private student loans unless you have a clear gap to fill.

Federal student loans for community college

If you're enrolled at least half-time in community college, you might qualify for federal Direct Subsidized Loans, Direct Unsubsidized Loans, or both. Subsidized loan eligibility hinges on financial need, and these loans offer the advantage of not accruing interest until six months after school ends, potentially saving you a significant amount in interest. On the other hand, Direct Unsubsidized Loans begin accruing interest immediately upon disbursement and do not require proof of financial need.

Congress sets the interest rate for federal student loans annually, and they are the same for all borrowers. For the 2026-27 school year, the interest rate for Direct Subsidized and Direct Unsubsidized federal student loans is 6.52% for undergraduate students.

Both of these loan types come with annual and aggregate student loan borrowing limits, as seen below:

Source: U.S. Department of Education

Learn More: Direct Subsidized vs. Unsubsidized Student Loans

The amount you can borrow for community college each year might be lower than the annual loan limits shown. Your eligibility depends on your school's cost of attendance and any other financial aid you receive, such as scholarships, grants, or work-study funds.

To get federal student loans, you have to submit the Free Application for Federal Student Aid (FAFSA) each year you need funding. You'll need to provide details like your Social Security number, net worth, and tax returns. After your application is reviewed, you'll receive a student aid report that breaks down the federal loans and other financial aid you qualify for.

Private student loans for community college

If you don't qualify for federal student loans or hit your borrowing limits, private student loans can help you pay for community college. However, private student loans often have fewer borrower protections and higher interest rates than federal loans.

Private student loan rate trends

Finding the right private student loan for community college

Although not all lenders offer student loans for associate degrees, many do. College Ave, Sallie Mae, Ascent, and Custom Choice are among those that help students pay for community college. Other private lenders, like SoFi, require enrollment in a bachelor's degree program or higher to qualify for a loan.

As you explore your options, it's important to compare lenders to find the most affordable loan. To compare private student loan lenders, prequalify with at least three, and pay attention to factors such as:

- Annual percentage rate (APR): When you prequalify, you can see the rate you’d likely qualify for when you formally apply. The APR encompasses both the interest rate and any fees associated with the loan, so it’s a better representation of the cost of borrowing.

- Loan amounts: Private student loan lenders set both minimum and maximum loan amounts — often $1,000 up to the school-certified cost of attendance, but this varies by lender. It’s important to know if the lender you’re considering can offer you the funds you’re looking for.

- Repayment terms: Common repayment terms include 5, 7, 10, 15, and 20 years, but not every lender offers all of these. Whether you’re looking to spread payments out over a longer period or want a short repayment term, check that the lenders you’re comparing have the loan term you want.

- Fees: Some lenders don’t charge any fees, while others charge late fees, application fees, and prepayment penalties.

- Discounts: Many lenders offer an autopay discount of 0.25 percentage points, but not all do. Student loan lenders may also offer loyalty discounts to existing borrowers or a small principal balance reduction as a graduation bonus.

Adding a cosigner could also improve your chances of approval and help you secure a lower interest rate. A cosigner is typically a parent or family member with good credit who shares responsibility for the loan and agrees to step in if you can't make payments.

Best private student loans for community college students in 2026

Advertiser Disclosure

We receive compensation from the companies below if you purchase a product. Amount of compensation does not impact the ranking or placement of a particular product. Not all available financial products and offers from all financial institutions have been reviewed by this website. This content is not provided by Credible or any of the Providers on the Credible website. Any opinions, analyses, reviews or recommendations expressed here are those of the author’s alone, and have not been reviewed, approved or otherwise endorsed by Credible.

Ascent: Best for No-Cosigner Loans

To determine the best student loan companies, Credible evaluated lenders based on several different categories, including: rates and fees, loan terms, eligibility, repayment options, and customer support. We assigned a score out of five stars to each lender based on our findings.

Read our full methodology.

Min. Credit Score

Does not disclose

Fixed APR

-

Variable APR

-

Loan Amount

$2,001 to $400,000

Term

5, 7, 10, 12, 15, 20

Our take

Ascent stands out for offering private student loans to students without a cosigner and who have limited credit. Its Outcomes-Based Loan uses factors such as academic performance and graduation timeline instead of credit to determine eligibility. Students can also qualify for a cash-back graduation reward and choose from a wide range of repayment plans.

Advertiser Disclosure

We receive compensation from the companies below if you purchase a product. Amount of compensation does not impact the ranking or placement of a particular product. Not all available financial products and offers from all financial institutions have been reviewed by this website. This content is not provided by Credible or any of the Providers on the Credible website. Any opinions, analyses, reviews or recommendations expressed here are those of the author’s alone, and have not been reviewed, approved or otherwise endorsed by Credible.

College Ave: Best for Extended Grace Periods

To determine the best student loan companies, Credible evaluated lenders based on several different categories, including: rates and fees, loan terms, eligibility, repayment options, and customer support. We assigned a score out of five stars to each lender based on our findings.

Read our full methodology.

Min. Credit Score

Does not disclose

Fixed APR

-

Variable APR

-

Loan Amount

$1,000 up to 100% of the school-certified cost of attendance

Term

5, 8, 10, 15 (20 for health professionals)

Our take

College Ave offers a wide range of borrower-controlled features that makes it especially compelling for those who want predictability and planning power with their student loans. From 5 to 20-year terms and multiple in-school payment options to profession-specific grace periods, College Ave offers more structure and flexibility than many of its competitors.

Advertiser Disclosure

We receive compensation from the companies below if you purchase a product. Amount of compensation does not impact the ranking or placement of a particular product. Not all available financial products and offers from all financial institutions have been reviewed by this website. This content is not provided by Credible or any of the Providers on the Credible website. Any opinions, analyses, reviews or recommendations expressed here are those of the author’s alone, and have not been reviewed, approved or otherwise endorsed by Credible.

Sallie Mae: Best for Specialized Loans

To determine the best student loan companies, Credible evaluated lenders based on several different categories, including: rates and fees, loan terms, eligibility, repayment options, and customer support. We assigned a score out of five stars to each lender based on our findings.

Read our full methodology.

Min. Credit Score

Does not disclose

Fixed APR

-

Variable APR

-

Loan Amount

$1,000 up to 100% of school-certified cost of attendance

Term

10 - 20

Our take

Sallie Mae stands out from the competition with one of the broadest selections of specialized private student loans on the market, including a new parent loan option introduced in 2026 that adds a private alternative to parent PLUS as federal borrowing caps tighten.

Advertiser Disclosure

We receive compensation from the companies below if you purchase a product. Amount of compensation does not impact the ranking or placement of a particular product. Not all available financial products and offers from all financial institutions have been reviewed by this website. This content is not provided by Credible or any of the Providers on the Credible website. Any opinions, analyses, reviews or recommendations expressed here are those of the author’s alone, and have not been reviewed, approved or otherwise endorsed by Credible.

Custom Choice: Best for Discounts and Rewards

To determine the best student loan companies, Credible evaluated lenders based on several different categories, including: rates and fees, loan terms, eligibility, repayment options, and customer support. We assigned a score out of five stars to each lender based on our findings.

Read our full methodology.

Min. Credit Score

660

Fixed APR

-

Variable APR

-

Loan Amount

$1,000 up to school-certified cost of attendance (aggregate $300,000 limit for an undergraduate loan, $350,000 limit for a graduate or graduate certificate loan)

Term

5, 7, 10, 15, 20

Our take

Custom Choice offers a compelling combination of rate discounts, graduation rewards, and zero fees. You can reduce your interest rate by 0.25 percentage points with autopay and request a 2% principal reduction after graduating. With no fees, cosigner release available after 12 consecutive on-time monthly principal and interest payments, and hardship forbearance, it's a good option for students seeking both savings and support.

How to get free money for community college

Student loans aren't the only way to cover the cost of attending community college. Explore other financial aid options below:

- Scholarships and grants: Scholarships and grants don't need to be repaid, which makes them one of the best ways to fund your education. Submitting the FAFSA puts you in the running for federal, state, and school-specific scholarships and grants. However, you can also apply for private scholarships and grants for even more free funding.

- Federal work-study program: If you qualify for the work-study program through the FAFSA, you can earn money to help offset your education costs. Work-study jobs are often flexible and designed to fit around your class schedule.

- State-funded aid: Many states offer financial aid specifically for community college students. For example, the California Promise helps make community college more affordable by allowing colleges to waive enrollment fees for first-time, full-time students who don't qualify for the California College Promise Grant (a separate program for low-income students).

- Employer-based tuition assistance: If you're working part- or full-time while attending community college and have already taken out student loans, consider asking your employer if it offers tuition assistance or reimbursement. Employers can provide up to $5,250 in tax-free assistance to each employee annually, which can help you pay for the principal and interest on your student loan.

Editor insight: “I strongly advise exhausting all financial aid options before committing to student loans. Because interest can exponentially inflate your balance, prioritize non-repayable aid like scholarships and grants. It’s also important not to overlook the federal work-study program, which can offset costs while you build professional experience.”

— Kelly Larsen, Student Loans Editor, Credible

Can I go to community college for free?

It’s possible to attend community college without paying tuition if your state has a grant program. As of 2026, more than 30 states offer tuition-free community college through grants. These programs generally fall into two categories:

- First-dollar funding: Covers tuition costs upfront, regardless of other financial aid you receive.

- Last-dollar funding: Kicks in after other financial aid is applied, filling any remaining tuition gaps.

Keep in mind that these programs generally only pay for tuition, meaning you might need to pay for additional educational expenses, such as room and board. However, some states are expanding their programs to help with these costs. Massachusetts, for example, offers allowances of up to $1,200 for books and supplies based on the student's income level.

How to apply for community college loans

If you decide to apply for community college loans, use the steps below as a guide.

- Submit the FAFSA: This form is key to unlocking federal student loans, grants, and work-study opportunities. Schools use the information in your FAFSA to determine your eligibility for federal student aid.

- Search for private scholarships and grants: Apply for scholarships and grants from private organizations, community groups, and your school. These funds don't need to be repaid, so they're one of the best ways to minimize your out-of-pocket costs.

- Fill gaps with private loans: If your scholarships, grants, and federal loans don't fully cover your costs, private student loans can help. Be sure to compare lenders to find loans with competitive rates, flexible repayment terms, and minimal fees.

Community college student loan repayment options

You can choose from several student loan repayment options, depending on whether you take out federal or private loans.

Federal student loan repayment options

Federal student loans for community college offer the most repayment flexibility. Most borrowers start on the Standard Repayment Plan, which features fixed payments over 10 years. If your income is lower or unpredictable, income-driven repayment (IDR) plans adjust monthly payments based on your earnings and family size and may offer forgiveness after 20 or 25 years.

As of July 1, 2026, new federal student loan borrowers will be limited to just two options:

- Standard Repayment Plan: Fixed monthly payments spread over 10 to 25 years, depending on your loan amount

- Repayment Assistance Plan (RAP): Income-based plan with payments adjusted to your income over a fixed 30-year term, with any remaining balance forgiven at the end of the 30 years

Check Out: Guide to Income-Driven Repayment Plans

Private student loan repayment options

Private student loan repayment options vary by lender. Many allow you to defer payments while you’re in school, while others require full, interest-only, or fixed monthly payments. Repayment terms typically range from five to 15 years, and borrowers can often choose between fixed or variable interest rates.

Check Out: Private Student Loan Repayment Options

Tips for managing community college loans

As you navigate community college debt, the tips below can help.

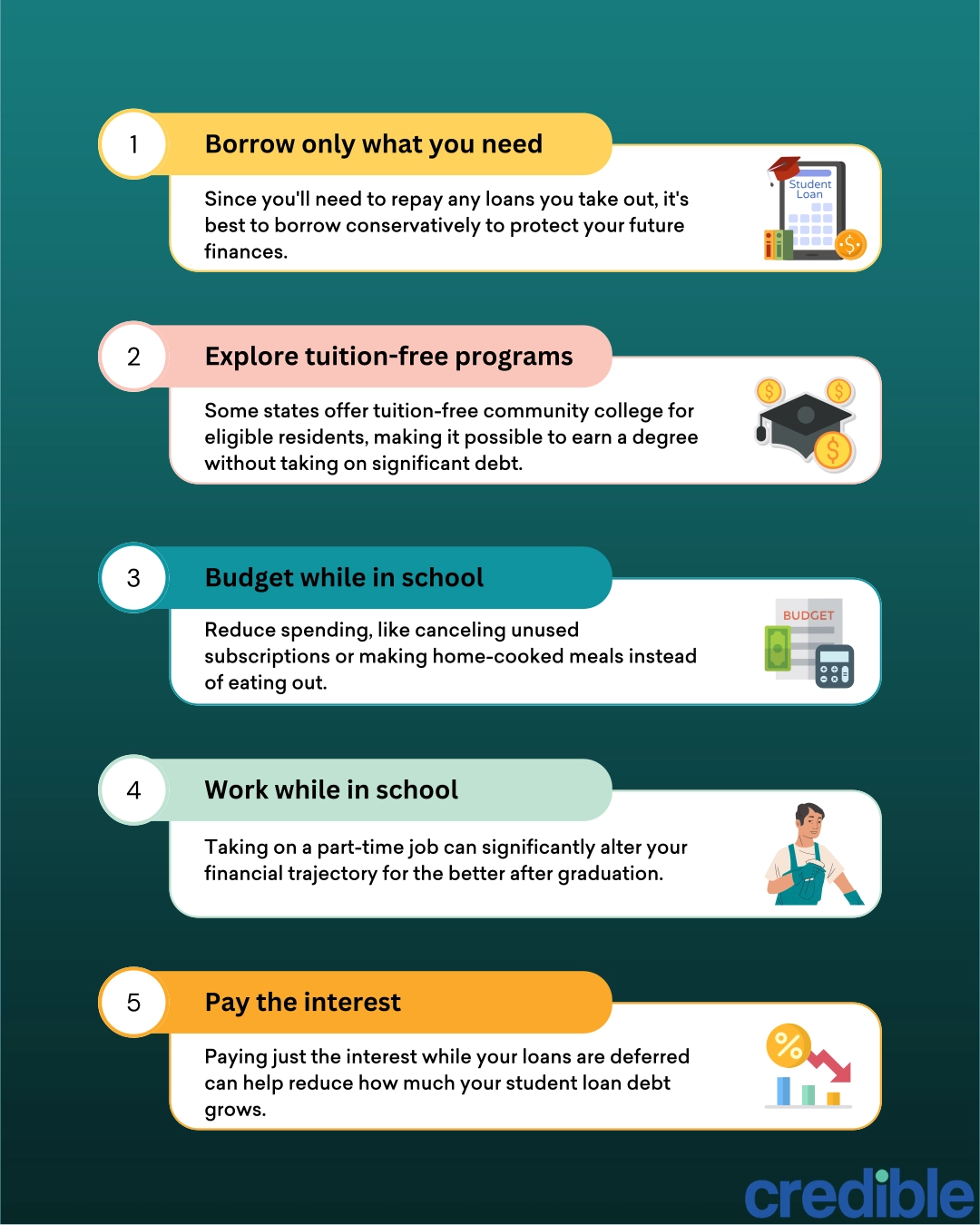

Borrow only what you need

Since you'll need to repay any loans you take out, it's best to borrow conservatively to protect your future finances.

“Investigate all tuition assistance programs or local scholarships specifically tailored to community college students,” says Dr. Shaan Patel, founder and CEO of Prep Expert, a platform offering SAT and ACT preparatory courses.

“These sometimes go under the radar and can be less competitive than larger scholarships. Next, stay focused on completion — taking only classes that align with your degree path helps avoid extra semesters,” adds Patel, who says he received admission to top universities and over $500,000 in college scholarships.

Explore tuition-free programs

Some states offer tuition-free community college for eligible residents, making it possible to earn a degree without taking on significant debt. These programs often have specific requirements, such as maintaining a certain GPA or meeting income limits.

If your state has a tuition-free program, it's worth exploring. Contact your state's education agency or your college's financial aid office to learn about eligibility criteria and how to apply.

Budget while in school

Building and sticking to a budget during community college can help you borrow less and keep your finances in check. Start by calculating your expected expenses, including tuition, textbooks, and living costs, and create a plan to cover them. Look for areas where you can reduce spending, such as canceling unused subscriptions or opting for home-cooked meals instead of dining out.

Expert insight: “Textbooks are another ghost expense because you can easily cut expenses by balancing buying online with asking professors which ones are really required.”

— Reyna Gobel, author of "CliffNotes Graduation Debt: How to Manage Student Loans and Live Your Life”

Work while in school

Balancing work and school is often a challenge. But when you work while attending school, you can use your earnings to offset educational costs and living expenses. Even taking on a part-time job can significantly alter your financial trajectory for the better after graduation.

Pay the interest while in school

Paying the interest on your student loans while you’re still in school can make a big financial difference over time. Even small monthly interest payments can keep your loan balance from growing. By graduation, you’ll owe closer to what you actually borrowed, not hundreds or thousands more.

Additional considerations for community college borrowers

Beyond comparing federal and private loan options, it’s important to be aware of several key factors that can affect borrowing for community college:

- Loan limits: Community college borrowers often qualify for smaller federal loan limits. Be sure to plan for this when estimating costs.

- Repayment terms: Because community college programs are shorter, repayment may begin sooner than at a four-year school. Make sure you fully understand grace periods and repayment schedules.

- Refinancing options: Some lenders allow refinancing once you transfer to a four-year program or graduate from a two-year program.

Why trust Credible?

The Credible editorial team is independent and unbiased. Partners do not influence our editorial content. To help you find the best student loan for your situation, we conduct thorough research and analyze thousands of lender data points. Using data-driven methodologies, we score criteria that are important to you. This allows us to objectively rank student loan lenders and products. To learn more, read our methodology below.

Methodology

To determine the best community college student loan lenders, Credible collected more than 1,000 points of data on two dozen companies and evaluated them on several different categories: repayment options, eligibility, interest rates, loan terms, and customer support. Based on our findings, we assigned a score out of five stars to each lender. Below are the weightings assigned to the general categories for the best student loan companies — which comprise individual criteria that are also weighted.

- Repayment options: 30%

- Eligibility: 25%

- Interest rates: 20%

- Loan terms: 15%

- Customer support: 10%

While the best lender for you will depend on your unique needs and financial circumstances, these findings should help answer your questions and assist you in your search for the best student loan.

Learn more about our methodology.

FAQ

What is the average cost of community college?

Open

Can community college students get loans?

Open

How do student loans work for community college?

Open

Do all community colleges accept FAFSA?

Open

Do community colleges offer student loans?

Open

Can I use federal student loans for part-time community college programs?

Open

How can I maximize financial aid for community college?

Open

What are the best private student loans for community college?

Open

Are student loans worth it for community college students?

Open

Does Sallie Mae work with community colleges?

Open