A sweeping overhaul of the federal student aid system will reshape how Americans pay for college beginning July 1, 2026. To understand how prepared borrowers are for these shifts, we surveyed Americans ages 18 to 61 across Gen Z, Millennials, and Gen X and found that many are unprepared for the changes.

Key federal student loan changes taking effect in July 2026 include:

- Elimination of grad PLUS loans, federal loans available to graduate and professional students

- A phaseout of most income-based repayment plans in favor of a single plan, the Repayment Assistance Plan

- New borrowing limits on parent PLUS loans and direct unsubsidized graduate loans

Our nationwide survey explored awareness of the upcoming policy changes, whether borrowers are adjusting their strategies through refinancing or alternative repayment options, and how the changes may influence future borrowing decisions.

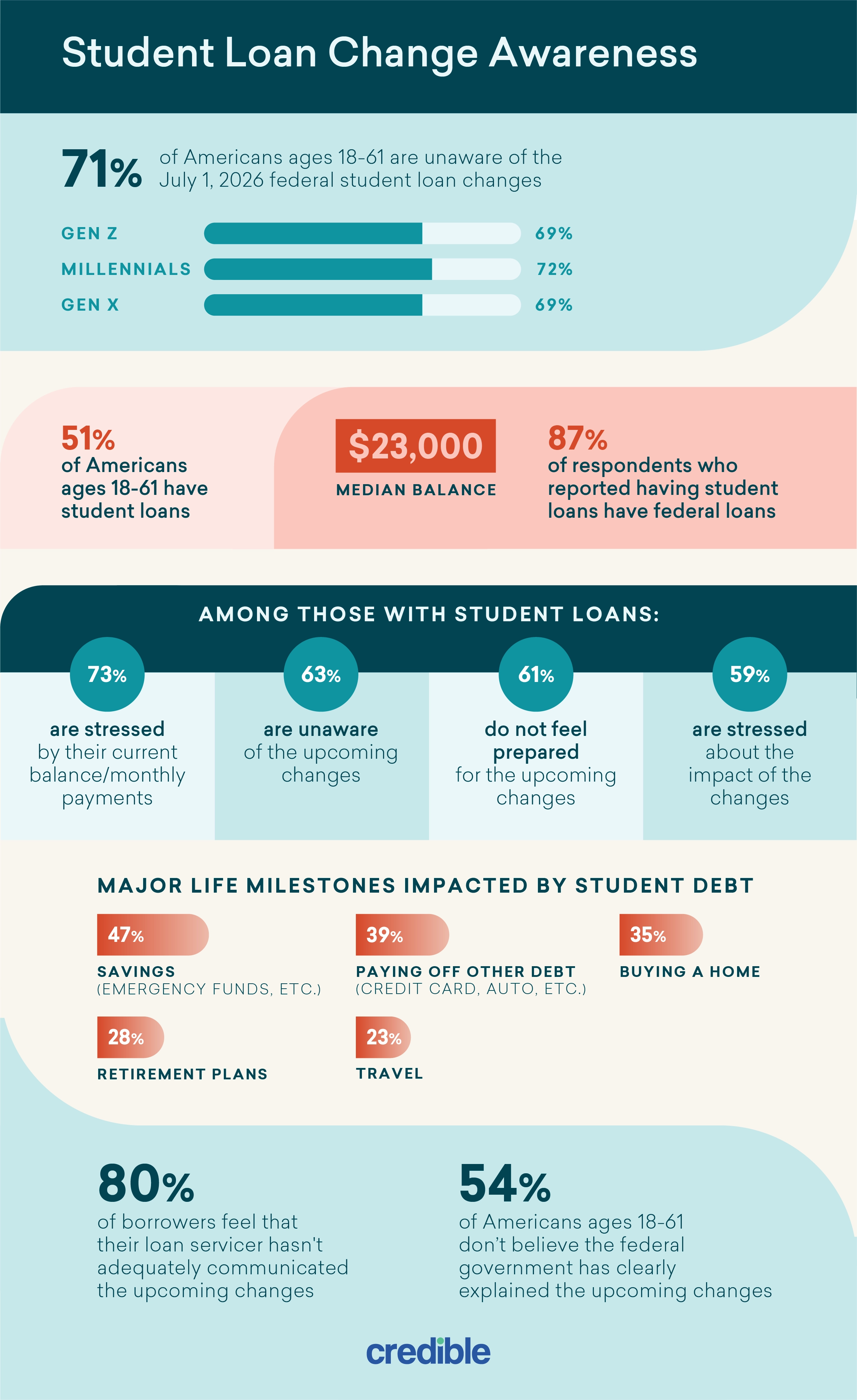

71% are unaware of upcoming student loan changes

A majority of Americans surveyed have low awareness of the July 1 changes. Millennials are the least aware (72%), followed by Gen Z (69%), and Gen X (69%).

Editor insight: “The upcoming policy changes will significantly alter the federal student loan borrowing and repayment experience for millions of people. Because many of these shifts occur automatically at the start of the next academic year, understanding the new rules now is a critical step in maintaining long-term financial stability.”

— Kelly Larsen, Student Loans Editor, Credible

Our survey found 51% of Americans ages 18 to 61 have student loans, with a median balance of $23,000. Nearly 9 in 10 (87%) borrowers have federal loans.

Among those with student loans:

- 73% are stressed by their current balance/monthly payments

- 63% are unaware of the upcoming changes

- 61% do not feel prepared for the upcoming changes

- 59% are stressed about the impact of the changes

Student loan debt influences major financial decisions and long-term goals for many. Borrowers we surveyed reported their debt has delayed several life milestones, including:

- Savings (for example, emergency funds): 47%

- Paying off other debt (credit card, auto, etc.): 39%

- Buying a home: 35%

- Retirement plans: 28%

- Travel: 23%

Many respondents feel like they haven’t received sufficient information about these changes and how they’ll be affected. Four-fifths of borrowers say their loan servicer hasn’t adequately communicated the upcoming changes, and 54% of respondents say the federal government hasn’t clearly explained the new policies.

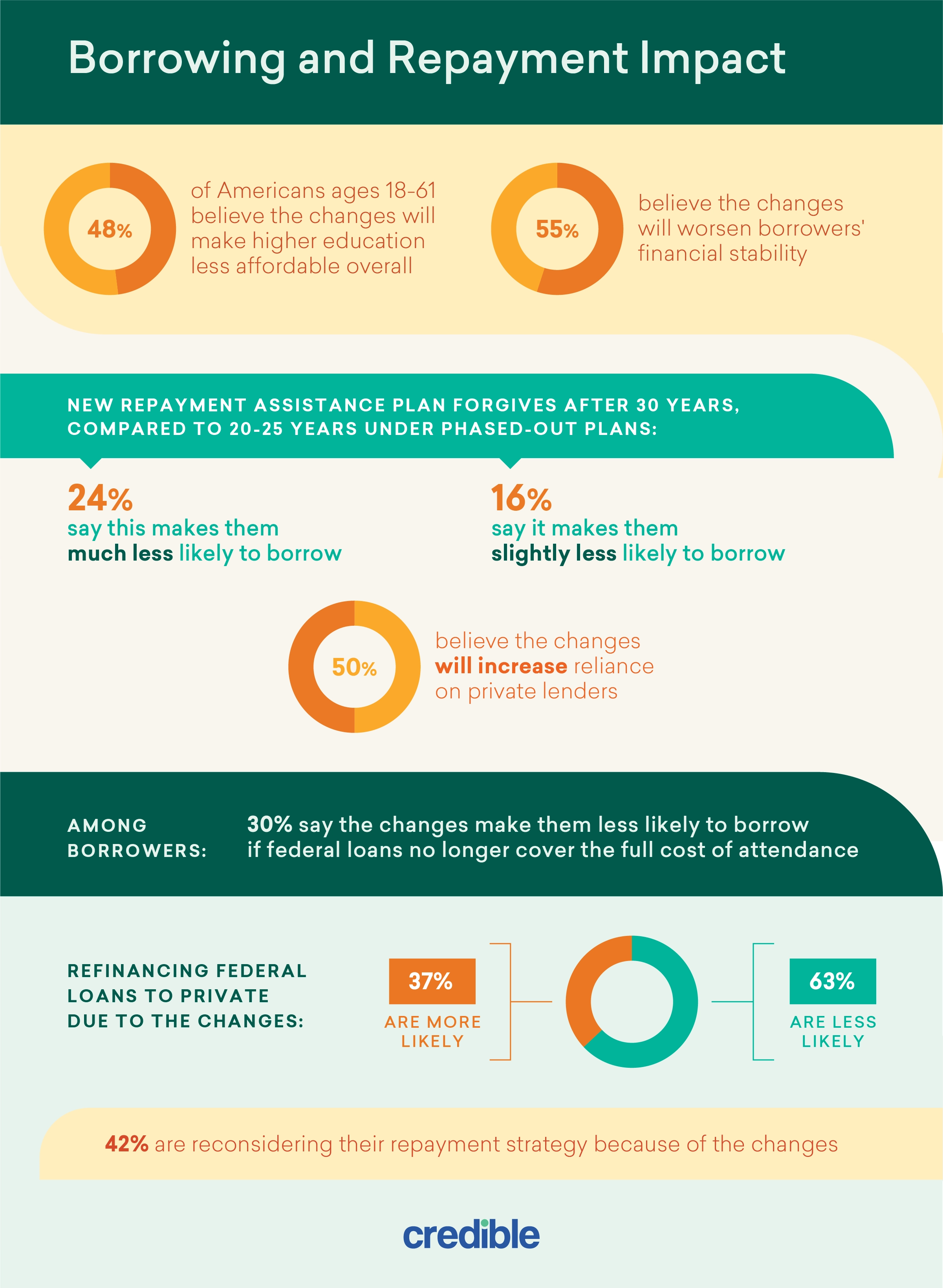

Nearly half of Americans expect student loan changes to worsen borrowers’ finances

Nearly half of respondents (48%) believe the changes will make higher education less affordable, while 55% say the new policies will worsen borrowers’ financial stability.

One of the most notable adjustments involves the new Repayment Assistance Plan, which would forgive remaining balances after 30 years of repayment, compared with 20 to 25 years under income-based plans being phased out. This longer timeline appears to influence borrowing attitudes:

- 24% say this makes them much less likely to borrow

- 16% say it makes them slightly less likely to borrow

Many Americans also anticipate broader ripple effects across the borrowing landscape. Half of the respondents believe the changes will increase reliance on private lenders.

Among borrowers, 30% say the changes make them less likely to borrow if federal loans no longer cover the full cost of attendance. When it comes to refinancing, 63% are less likely to refinance federal loans into private loans, while 37% are more likely. Additionally, 42% are reconsidering their repayment strategy because of the changes.

Editor insight: “The 2026 overhaul replaces more flexible legacy income-driven repayment plans with a 30-year framework. The extended timeline means many borrowers may pay more over the life of their loans than under previous programs. It’s important to understand these nuances so you can determine if it makes sense to continue with income-driven repayment, or if refinancing would be a better option.”

— Kelly Larsen, Student Loans Editor, Credible

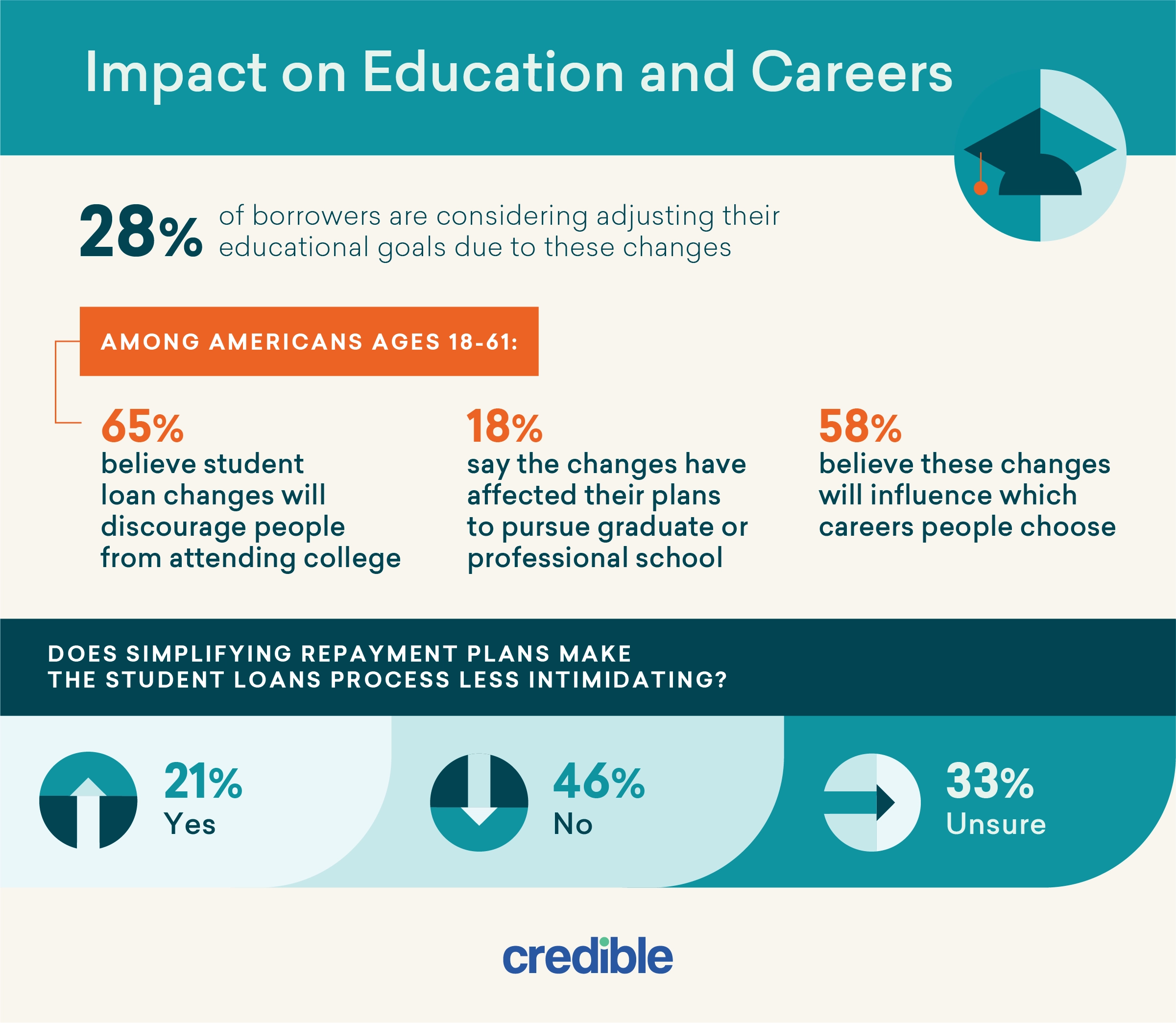

Nearly 2 in 3 say loan changes will discourage college attendance

Many Americans believe the changes to federal student loans could influence not only how people borrow, but whether they pursue higher education at all. Among borrowers, 28% are considering adjusting their educational goals due to these changes. Some are considering pausing or delaying their education, switching schools, or are deterred from pursuing graduate or professional schooling.

Nearly 2 in 3 respondents believe the policy changes will discourage people from attending college. About 58% believe these changes will influence which careers people choose. And 18% say the changes have affected their plans to pursue graduate or professional school

While one of the big changes is that there will be far fewer repayment plans to choose from, 46% of those surveyed say this doesn’t make the student loan process less intimidating, 21% say it does, and 33% are unsure.

Editor insight: If you have student loans or plan to borrow for college, don’t delay preparing for these changes. Start by carefully reviewing your loans, assessing how the new repayment plan may influence long-term costs, and exploring options like consolidation or refinancing. Taking those steps now can make the transition more manageable and reduce the risk of surprises.”

— Kelly Larsen, Student Loans Editor, Credible

As the July 1, 2026, deadline approaches, the burden of staying informed falls increasingly on the borrower. For borrowers seeking guidance, Credible offers resources and tools to help navigate student loan changes, compare refinancing options, and explore repayment strategies as the new policies take effect.

Methodology

In February 2026, Credible commissioned Digital Third Coast and Prolific to conduct a survey of 1,010 people ages 18 to 61 from across the U.S. about student loans. Among respondents, 50% identified as male, 49% as female, and 1% non-binary/rather not say. The median age of respondents was 37.

For media inquiries, contact [email protected].

Fair use

When using this data and research, please attribute it by linking to this study and citing Credible.