Credible takeaways

- Getting control of a large student loan balance means moving beyond minimum payments and using a strategy to lower your interest rate and free up cash.

- Start by getting a clear look at your loan types and rates so you can build a plan that actually fits your situation.

- Cut down total costs with things like autopay discounts and putting any extra cash directly toward your principal balance when possible.

- Try splitting your monthly bill into biweekly payments to sneak in one extra full payment every year without feeling a major pinch.

- Don't just settle for the default repayment plan if an income-driven option or a forgiveness program could save you more in the long run.

Americans collectively owed $1.85 trillion in student loans at the end of the 2024-25 school year, according to the Consumer Financial Protection Bureau. In total, more than 46 million Americans have either federal or private student loans. Repaying them can be very stressful.

A 2023 University of Georgia analysis of Twitter and Reddit posts revealed that many borrowers described poor mental health, sadness, and fear because of their educational debt. And, owing a large amount can exacerbate these issues.

If you're worried about having a large student loan balance, these tips from financial advisers could help you get a handle on your debt and move forward in a positive way.

Current student loan refinance rates

1. Focus on understanding your student loans and planning first

Typically, you must start repaying student loans when you graduate or drop below half-time enrollment. You'll usually have a grace period and, for federal student loans, will be put on the standard 10-year repayment plan by default.

A study from the National Bureau of Economic Research revealed that many borrowers stick with the default to their detriment — even though they qualify for plans that are a better fit, because they don't understand or research their options.

If you have a large loan balance, sticking with the status quo could lead to unmanageable payments. That's why Patrick Yono, founder of Sure Life Financial, says his best tip for handling student loans is to start with a careful review of your loans and repayment options.

“Before tackling your student loan debt, it’s important you actually understand your loan,” Yono warns. “Many throw money toward their student loan debt, not understanding the clear picture of their situation. Once you understand your loan, you’re able to develop a plan.”

Key details to review to build a student loan repayment strategy

Yono recommends focusing on:

- Whether you have a private or federal student loan: “Federal loans have the possibility of being forgiven in the future, whereas private loans do not,” he says. This should affect your decision-making as you focus on which loans to prioritize or pay off early.

- Find out how your interest rate works: Federal student loans have fixed interest rates, but that's not always true of private student loans. “A fixed rate means you’ll have the same interest throughout the entire life of the loan, whereas a variable rate can go up and down,” Yono says. Variable-rate student loans are usually a higher priority for payoff or may be worth refinancing because of the risk of rates rising.

- Explore your payoff timeline: Loans have different repayment periods, and Yono stresses the importance of understanding the schedules, as this can also affect which loans you'll be focused on first.

Planning isn't just something you do once, either — especially if you have a large loan balance. “A student loan payoff plan should be reviewed every year to amend your plan to reflect your current financial situation,” Yono says.

This may, for example, mean moving onto an income-driven plan if you started a new job at a nonprofit and could potentially qualify for forgiveness. Or it could mean opting to move to a standard plan if your income has been going up and you want to get out of debt ASAP.

2. Do what you can to reduce the student loan interest you pay

One of the more frustrating things for student loan borrowers is that they can make payments, sometimes for years, and find themselves with their balance barely declining because of interest. This is an especially big issue if you have a large balance, as interest can add up quickly.

Domenick D'Andea, a certified plan fiduciary advisor (CPFA) and co-founder of DanDarah Wealth Management, says his best tip for tackling student loans is to try to pay as little interest as possible. You can do this by making strategic moves to reduce your rate and eliminate high-interest debt as soon as possible.

“Pay more than the minimum on your highest-interest-rate debt,” D'Andrea advises. “Make sure the extra payment is allocated to the principal, as this will decrease the amount of interest that you pay over time.”

D'Andrea also suggests taking advantage of autopay discounts, which can lower your student loan interest rate by as much as one-quarter of a percent.

Or, he says, you could consider refinancing private student loans — or even federal student loans if the “lower interest rate is worth giving up any potential benefits a federal loan offers over a private loan.”

Ways to reduce your student loan interest costs starting now

Signing up for autopay can be the quickest and easiest way to lower your interest rate if your lender offers a discount. However, D'Andrea also has other suggestions for cutting interest costs.

Some of the best ways you can reduce your rate or the total interest you pay include:

- Budgeting each month to pay extra toward the principal on high-interest student loans

- Getting quotes from multiple refinance lenders and evaluating carefully whether refinancing makes sense

- Focusing on paying off your most expensive student loans first. The sooner you can repay high-interest debt, the lower your total financing costs end up being

3. Find creative approaches to reduce your student loan balance

Finally, the last key tip comes from Daniel Milan, investment adviser representative and managing partner at Cornerstone Financial Services. Milan urges borrowers to carefully select their payment plan and to find creative ways to try to pay off the debt ASAP — especially if they owe a lot.

Milan says that, when possible, you should begin by exploring forgiveness options to see if you're eligible.

If you can't qualify, you can tweak your payment schedule in a way that brings your balance down faster without a lot of extra sacrifice.

“Looking at student loan payments as biweekly, rather than monthly payments, can be beneficial,” advises Milan. “This way, you can add extra full payments each year, which quietly reduces interest paid over time.”

How small payment shifts can reduce your student loan balance faster

Consistently paying even a little bit extra each month can make a big difference in your student loan repayment efforts. However, if you struggle to commit a large amount of money to extra payments, you can implement Milan's creative alternative.

This tip works because most people get paid every two weeks. If half of each student loan payment comes out of each paycheck, you'll make 26 payments during the year. That gives you an extra full week of payments annually, without any real extra effort on your part.

Since that extra payment can reduce your principal balance, instead of just being eaten up by interest, it can make a big difference in helping to bring your student loan debt balance down quickly. Getting the principal paid down faster has an especially big impact when you have a large loan balance.

Common mistakes borrowers with high student loan balances make

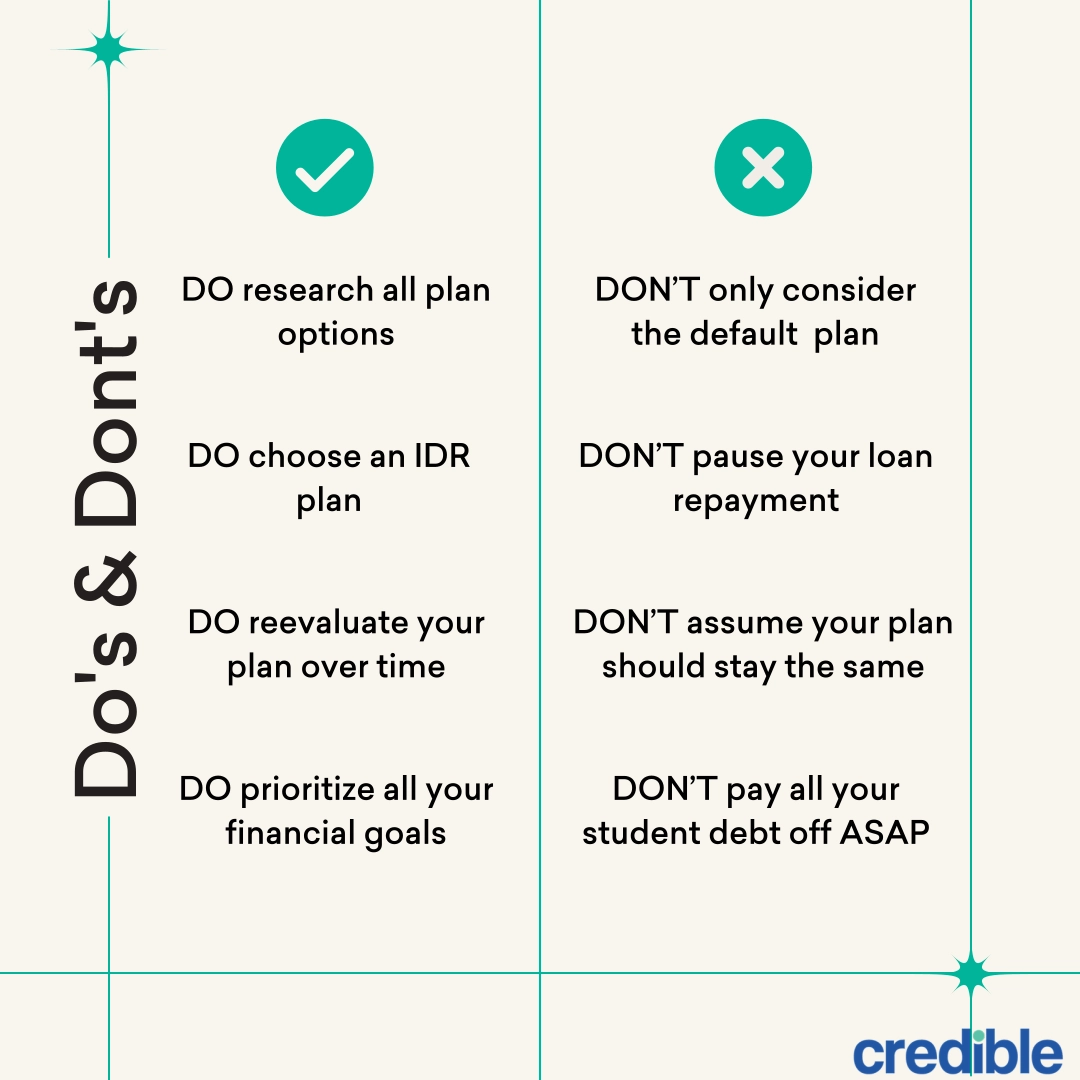

Many borrowers make mistakes when they owe a lot of money on their student loans. The following mistakes can make payoff much harder:

- Sticking with the default payment plan without exploring options: When you are put on a 10-year standard payment plan, your payments may be so high you can't accomplish any other goals. Research all the options to find something that works for your budget.

- Choosing deferment or forbearance over income-driven repayment: Income-driven repayment plans can result in you paying very little on your loans while still getting credit toward income-driven forgiveness. Explore these options before pausing your loan repayment.

- Failing to reevaluate your plan over time: You may be paying off your high-interest student debt for many years. Don't assume your plans and payments should stay the same over time. You also want to understand your goals for the plan, such as whether you want to save the most money or have the lowest monthly payments.

- Assuming you should focus on paying all your student debt off ASAP: In some cases, if you have low-interest federal student loans, it may make sense to prioritize other financial goals over paying them off early.

Avoiding these mistakes and making a smart plan for payoff can help you to manage even large amounts of student loan debt.

FAQ

How do I manage student loans if I owe a lot of money?

Open

Should I refinance student loans or stay on a federal repayment plan?

Open

When does refinancing student loans make sense for high balances?

Open

What are common mistakes when managing large student loan balances?

Open

Does having a high student loan balance change the best repayment strategy?

Open