Credible takeaways

- You must be enrolled at least half-time in an eligible school and program to qualify for federal student loans.

- Some private lenders offer student loans to part-time students even if they're enrolled less than half-time.

- Part-time enrollment allows for more flexibility in your schedule, but it also comes with downsides, like taking longer to graduate.

- You can still qualify for grants, scholarships, and the federal work-study program as a part-time student.

Federal student loans require at least half-time enrollment to be eligible, which generally means taking at least six credit hours each semester. However, even if you're only taking one or two classes, you have options for less-than-half-time student loan funding.

Some private lenders offer student loans for students enrolled less than half-time. However, approval depends on other factors such as your credit profile and whether you apply with a cosigner. Abe, College Ave, and Ascent are among lenders on the Credible platform that stand out for their flexible eligibility criteria.

Here's what you need to know about finding the best part-time student loans and how to qualify as a part-time student.

Compare part-time student loan lenders

Advertiser DisclosureThe rates that appear are from companies from which Credible receives compensation. This compensation does not impact how or where products appear within the table. The rates and information shown do not include all financial service providers or all of the displayed lenders' available services and product offerings.

Lender

Fixed (APR)

Loan Amounts

Min. Credit Score

Credible rating

To determine the best student loan companies, Credible evaluated lenders based on several different categories, including: rates and fees, loan terms, eligibility, repayment options, and customer support. We assigned a score out of five stars to each lender based on our findings.

Read our full methodology.

$1,000 up to 100% of school-certified cost of attendance

Overview

Sallie Mae offers the Smart Option Student Loan for undergraduate students, a suite of loans for graduate students, and parent loans that allow credit-qualified parents, guardians, or other sponsors to borrow directly to help cover a student's costs. You can borrow up to your school-certified cost of attendance and apply just once annually to get the funds you need for the entire academic year. Plus, applying for a Smart Option Student Loan with a cosigner may help you get a better rate.

Through Sallie Mae, you can find a variety of loans designed for specific needs, including loans for MBA programs, law school, medical school, and health profession programs.

pros

- Can borrow up to school-certified cost of attendance

- No prepayment or origination fees

- Loans available to noncitizens with an eligible cosigner

- Cosigner release after 12 on-time payments

- Parent loan options

cons

- Does not offer student loan refinancing

- Loan terms not disclosed until after you apply

Loan terms

10 to 15 years for the Smart Option Student Loan; 15 years for law school, MBA, and graduate school loans; 20 years for medical school loans

Loan amounts

$1,000 up to school-certified cost of attendance. Student must be listed as the borrower, and a parent may cosign.

Cosigner release

After making 12 on-time principal and interest payments, plus meet certain credit requirements

Eligibility

Must be a U.S. citizen or permanent resident enrolled in an eligible program. Noncitizens residing and attending school in the U.S. may qualify by applying with a creditworthy cosigner, who must be a U.S. citizen or permanent resident, and providing an unexpired government-issued photo ID.

Credible rating

To determine the best student loan companies, Credible evaluated lenders based on several different categories, including: rates and fees, loan terms, eligibility, repayment options, and customer support. We assigned a score out of five stars to each lender based on our findings.

Read our full methodology.

$1,000 up to 100% of the school-certified cost of attendance

Overview

College Ave offers student loans for almost every type of degree program, with a range of repayment options, including a unique 8-year repayment term. Additionally, you can get extended grace periods of as long as 36 months on graduate, dental, and medical student loans.

About 90% of undergraduates applying with a cosigner are approved for additional student loans. However, you must complete at least half of your repayment term before you can remove a cosigner for your loan. Some lenders allow cosigners to be released much sooner, after as few as 1 to 2 years of payments.

pros

- Rate discount of one-quarter of a percentage point for using autopay

- Does not charge origination or application fees

- Grace periods between 9 and 36 months for graduate, MBA, law, dental, and medical school loans

cons

- Parent borrowers are required to pay at least the interest while the student is in school

- Cosigners not eligible for release until at least half the repayment term of the loan is completed

Loan terms

5, 8, 10, or 15 years for most borrowers (law, dental, medical, and other health profession students have up to 20 years)

Loan amounts

$1,000 minimum up to your school’s annual cost of attendance; lifetime limits depend on your degree and credit profile

Cosigner release

Available after more than half of the scheduled repayment period has elapsed and other requirements are met

Eligibility

Must be a U.S. citizen or permanent resident at an eligible institution. International students with a Social Security number and a qualified cosigner may also qualify. Applicants who can’t meet financial, credit, or other requirements may qualify with a cosigner.

Credible rating

To determine the best student loan companies, Credible evaluated lenders based on several different categories, including: rates and fees, loan terms, eligibility, repayment options, and customer support. We assigned a score out of five stars to each lender based on our findings.

Read our full methodology.

$1,000 up to school-certified cost of attendance (aggregate $300,000 limit for an undergraduate loan, $350,000 limit for a graduate or graduate certificate loan)

Overview

Abe's private student loans are available to undergraduates, graduate students, and students enrolled in graduate certificate programs. Abe is unique in allowing you to borrow even if you're enrolled less than half-time.

Abe offers rate discounts and payment relief that other lenders don't, such as a reduction in your rate with autopay and for every six months of consecutive on-time principal and interest payments, up to a total of 0.50 percentage points. Borrowers can also extend their grace period up to an additional six months or up to nine months for Abe Law students. Plus, you can lengthen your repayment term by five years, which can be helpful if you need to lower your monthly payments or request a hardship forbearance for up to 12 months.

pros

- Offers 2% principal reduction after graduation

- Doesn’t charge late fees

- Can reduce interest rate by making on-time payments

- Possible repayment term and grace period extension

cons

- Doesn't allow parents to borrow on behalf of their child

- Student loan refinancing not available

Minimum income

$1 (must have positive income)

Loan terms

5, 7, 10, 15, or 20 years

Loan amounts

$1,000 and your school-certified cost of attendance, minus other financial aid. The aggregate loan limit is $300,000, or up to $350,000 if you're in an advanced degree program.

Cosigner release

Available after making 12 consecutive on-time monthly principal and interest payments

Eligibility

Must be a U.S. citizen or permanent resident. Available to international students and DACA recipients attending a Title IV-eligible school in the U.S. who apply with a cosigner who is a U.S. citizen or permanent resident alien. Lender Disclosures

Credible rating

To determine the best student loan companies, Credible evaluated lenders based on several different categories, including: rates and fees, loan terms, eligibility, repayment options, and customer support. We assigned a score out of five stars to each lender based on our findings.

Read our full methodology.

Overview

While Ascent provides traditional student loans for undergraduate, graduate, and medical programs, it also stands out with some options that are uncommon among private student loan lenders. For example, its Outcomes-Based Loan, which doesn't require established credit or a cosigner, is available to juniors and seniors. When assessing your application, Ascent considers factors including your school, major, and GPA to determine if you're eligible.

Ascent also offers its Progressive Repayment plan to qualified borrowers. It allows you to begin with smaller payments at the start of the repayment term and then gradually pay more each month over time. If you borrow with a cosigner, they can be released after you make as few as 12 monthly payments. However, cosigners on loans for international students do not qualify.

pros

- Doesn’t charge application fees or origination fees

- Offers discounts of 0.50 to 1 percentage points when making automatic payments

- Can get a 1% cash-back reward after you graduate

- Grace periods from 9 to 36 months

cons

- May find lower interest rates with some competitors

- International students don’t have option to release cosigners

Minimum income

$30,000 (waived with a cosigner or for undergrads with less than two years of credit history)

Loan terms

5, 7, 10, 12, 15, or 20 years

Loan amounts

$2,001 minimum up to your school’s annual cost of attendance; lifetime limits of $200,000 for undergrads and $400,000 for graduates

Eligibility

Must be a U.S. citizen or DACA student enrolled at least half time at an eligible institution. International students with a qualified cosigner may also qualify. Applicants who can’t meet financial, credit, or other requirements may qualify with a cosigner.

Credible rating

To determine the best student loan companies, Credible evaluated lenders based on several different categories, including: rates and fees, loan terms, eligibility, repayment options, and customer support. We assigned a score out of five stars to each lender based on our findings.

Read our full methodology.

Overview

Nelnet Bank (Member FDIC) provides private student loans at competitive rates for undergraduate, graduate, and health professional degrees. You'll need a FICO credit score in the mid to high 600s to qualify. Borrowers with bad credit can apply with a cosigner, which may help them qualify and could reduce their interest rate.

Cosigners on Nelnet student loans can be released after 24 consecutive on-time payments (see disclaimer). You can also get a 0.25% interest rate reduction when you sign up for automatic payments (see disclaimer). There are no loan origination or application fees, but Nelnet does charge fees for late payments of insufficient funds.

pros

- Rates are competitive for borrowers or cosigners with strong credit

- Rate discount of 0.25 percentage points for autopay

- Cosigners can be released after 24 on-time payments

- Offers deferment and payment assistance programs

cons

- Charges fees for late payment and insufficient funds

- Doesn’t guarantee deferment and forbearance options

Loan terms

5,10,15* (IO, Deferred, Immediate)

Loan amounts

$1,000 to $125,000 for undergraduate, $1,000 to $175,000 for graduate, $1,000 to $500,000 for graduate health professions

Eligibility

All states and US Territories

Credible rating

To determine the best student loan companies, Credible evaluated lenders based on several different categories, including: rates and fees, loan terms, eligibility, repayment options, and customer support. We assigned a score out of five stars to each lender based on our findings.

Read our full methodology.

Overview

SoFi offers fixed- and variable-rate student loans to help undergraduates, graduates, and parents finance their education. These loans can cover up to the total cost of attendance, with a minimum loan of $1,000. Students must be enrolled at least half-time in a degree-seeking program at an eligible school and be a U.S. citizen, a U.S. permanent resident, or a non-U.S. permanent resident alien.

SoFi has multiple repayment plans, allowing students to pick terms that best fit their financial situations, with cosigner release after 12 months of consecutive on-time payments. Borrowers can reduce their rates by 0.25% or 0.125% with SoFi's Continuing Scholar Discount on subsequent loans. Plus, a $250 cash bonus with a 3.0 GPA or higher for full-year loans or $100 cash back for single-semester loans.

Lender Disclosures

pros

- Top customer service ratings

- Valuable member benefits

- No fees

- Cosigner release after 12 months of on-time payments

cons

- No disclosed credit or income requirements

- Shorter repayment terms than some lenders

Loan amounts

$1,000 minimum, up to your school’s annual cost of attendance

Eligibility

Must be a U.S. citizen or DACA student enrolled at least half-time at an eligible institution. International students with a qualified cosigner may also qualify. Applicants who can’t meet financial, credit, or other requirements may be eligible with a cosigner.

Credible rating

To determine the best student loan companies, Credible evaluated lenders based on several different categories, including: rates and fees, loan terms, eligibility, repayment options, and customer support. We assigned a score out of five stars to each lender based on our findings.

Read our full methodology.

$1,000 up to school-certified cost of attendance (aggregate $300,000 limit for an undergraduate loan, $350,000 limit for a graduate or graduate certificate loan)

Overview

Custom Choice offers undergraduate loans ranging from $1,000 to $300,000 and graduate or graduate certificate loans up to $350,000.

You can get a 0.25% autopay discount, and up to a 0.25% on-time payment discount, plus a 2% principal reduction for graduating with at least a bachelor’s degree. You may apply with a cosigner if you can't qualify on your own, and you can release them after making 12 consecutive on-time principal and interest payments.

Custom Choice doesn't charge any fees whatsoever, even late fees. The lender also offers a forbearance program that lets you pause payments if you experience a financial hardship, an existing or persisting medical condition, a natural disaster, or suffer temporary unemployment.

pros

- You can reduce your rate by 0.5 percentage points with autopay and on-time payments

- Cosigner release available after 12 consecutive on-time monthly principal and interest payments

cons

- No mobile app for managing student loans

- Does not offer refinancing options for existing student loans

Minimum income

$1 (must have positive income)

Loan terms

5, 7, 10, 15, or 20 years

Loan amounts

$1,000 to $300,000 for an undergraduate loan, or up to $350,000 for a graduate or graduate certificate loan (In Iowa, the minimum is $1,001, and in Massachusetts, it’s $6,001.)

Cosigner release

After making 12 consecutive on-time principal and interest payments

Eligibility

Available to borrowers in all 50 states. The student must be a U.S. citizen or permanent resident alien, and must be the legal age of majority at the time of application or at least 17 years of age if applying with a cosigner who meets the age of majority requirements in the cosigner's state of residence. Eligible noncitizens, such as international students and DACA residents, can also qualify by applying with a cosigner who’s a U.S. citizen or permanent resident. Lender Disclosures

Credible rating

To determine the best student loan companies, Credible evaluated lenders based on several different categories, including: rates and fees, loan terms, eligibility, repayment options, and customer support. We assigned a score out of five stars to each lender based on our findings.

Read our full methodology.

$1,500 up to school’s certified cost of attendance less aid

Overview

Massachusetts Educational Financing Authority (MEFA) offers student loans to borrowers with good credit. However, you won't be able to see your potential rate before applying.

The lender doesn't charge any fees and its rates are competitive, though MEFA only offers two repayment terms. You can add a cosigner to your loan if you're unable to qualify, but only one repayment plan allows you to release your cosigner.

pros

- Doesn’t charge any fees

- Low maximum rate compared with some lenders

- Can borrow up to the school-certified cost of attendance

cons

- No discounts for borrowers

- Limited repayment terms

- No prequalification available

Loan amounts

$1,500 minimum, up to school-certified cost of attendance

Eligibility

Must be a U.S. citizen or permanent resident, enrolled at least half-time at a degree-granting, nonprofit institution, and must maintain satisfactory academic progress. Must have no history of default on an education loan and no history of bankruptcy or foreclosure in the past 60 months.

Credible rating

To determine the best student loan companies, Credible evaluated lenders based on several different categories, including: rates and fees, loan terms, eligibility, repayment options, and customer support. We assigned a score out of five stars to each lender based on our findings.

Read our full methodology.

Loan Amounts

$1,000 up to 100% of school-certified cost of attendance

Overview

Sallie Mae offers the Smart Option Student Loan for undergraduate students, a suite of loans for graduate students, and parent loans that allow credit-qualified parents, guardians, or other sponsors to borrow directly to help cover a student's costs. You can borrow up to your school-certified cost of attendance and apply just once annually to get the funds you need for the entire academic year. Plus, applying for a Smart Option Student Loan with a cosigner may help you get a better rate.

Through Sallie Mae, you can find a variety of loans designed for specific needs, including loans for MBA programs, law school, medical school, and health profession programs.

pros

- Can borrow up to school-certified cost of attendance

- No prepayment or origination fees

- Loans available to noncitizens with an eligible cosigner

- Cosigner release after 12 on-time payments

- Parent loan options

cons

- Does not offer student loan refinancing

- Loan terms not disclosed until after you apply

Loan terms

10 to 15 years for the Smart Option Student Loan; 15 years for law school, MBA, and graduate school loans; 20 years for medical school loans

Loan amounts

$1,000 up to school-certified cost of attendance. Student must be listed as the borrower, and a parent may cosign.

Cosigner release

After making 12 on-time principal and interest payments, plus meet certain credit requirements

Eligibility

Must be a U.S. citizen or permanent resident enrolled in an eligible program. Noncitizens residing and attending school in the U.S. may qualify by applying with a creditworthy cosigner, who must be a U.S. citizen or permanent resident, and providing an unexpired government-issued photo ID.

Credible rating

To determine the best student loan companies, Credible evaluated lenders based on several different categories, including: rates and fees, loan terms, eligibility, repayment options, and customer support. We assigned a score out of five stars to each lender based on our findings.

Read our full methodology.

Loan Amounts

$1,000 up to 100% of the school-certified cost of attendance

Overview

College Ave offers student loans for almost every type of degree program, with a range of repayment options, including a unique 8-year repayment term. Additionally, you can get extended grace periods of as long as 36 months on graduate, dental, and medical student loans.

About 90% of undergraduates applying with a cosigner are approved for additional student loans. However, you must complete at least half of your repayment term before you can remove a cosigner for your loan. Some lenders allow cosigners to be released much sooner, after as few as 1 to 2 years of payments.

pros

- Rate discount of one-quarter of a percentage point for using autopay

- Does not charge origination or application fees

- Grace periods between 9 and 36 months for graduate, MBA, law, dental, and medical school loans

cons

- Parent borrowers are required to pay at least the interest while the student is in school

- Cosigners not eligible for release until at least half the repayment term of the loan is completed

Loan terms

5, 8, 10, or 15 years for most borrowers (law, dental, medical, and other health profession students have up to 20 years)

Loan amounts

$1,000 minimum up to your school’s annual cost of attendance; lifetime limits depend on your degree and credit profile

Cosigner release

Available after more than half of the scheduled repayment period has elapsed and other requirements are met

Eligibility

Must be a U.S. citizen or permanent resident at an eligible institution. International students with a Social Security number and a qualified cosigner may also qualify. Applicants who can’t meet financial, credit, or other requirements may qualify with a cosigner.

Credible rating

To determine the best student loan companies, Credible evaluated lenders based on several different categories, including: rates and fees, loan terms, eligibility, repayment options, and customer support. We assigned a score out of five stars to each lender based on our findings.

Read our full methodology.

Loan Amounts

$1,000 up to school-certified cost of attendance (aggregate $300,000 limit for an undergraduate loan, $350,000 limit for a graduate or graduate certificate loan)

Overview

Abe's private student loans are available to undergraduates, graduate students, and students enrolled in graduate certificate programs. Abe is unique in allowing you to borrow even if you're enrolled less than half-time.

Abe offers rate discounts and payment relief that other lenders don't, such as a reduction in your rate with autopay and for every six months of consecutive on-time principal and interest payments, up to a total of 0.50 percentage points. Borrowers can also extend their grace period up to an additional six months or up to nine months for Abe Law students. Plus, you can lengthen your repayment term by five years, which can be helpful if you need to lower your monthly payments or request a hardship forbearance for up to 12 months.

pros

- Offers 2% principal reduction after graduation

- Doesn’t charge late fees

- Can reduce interest rate by making on-time payments

- Possible repayment term and grace period extension

cons

- Doesn't allow parents to borrow on behalf of their child

- Student loan refinancing not available

Minimum income

$1 (must have positive income)

Loan terms

5, 7, 10, 15, or 20 years

Loan amounts

$1,000 and your school-certified cost of attendance, minus other financial aid. The aggregate loan limit is $300,000, or up to $350,000 if you're in an advanced degree program.

Cosigner release

Available after making 12 consecutive on-time monthly principal and interest payments

Eligibility

Must be a U.S. citizen or permanent resident. Available to international students and DACA recipients attending a Title IV-eligible school in the U.S. who apply with a cosigner who is a U.S. citizen or permanent resident alien. Lender Disclosures

Credible rating

To determine the best student loan companies, Credible evaluated lenders based on several different categories, including: rates and fees, loan terms, eligibility, repayment options, and customer support. We assigned a score out of five stars to each lender based on our findings.

Read our full methodology.

Overview

While Ascent provides traditional student loans for undergraduate, graduate, and medical programs, it also stands out with some options that are uncommon among private student loan lenders. For example, its Outcomes-Based Loan, which doesn't require established credit or a cosigner, is available to juniors and seniors. When assessing your application, Ascent considers factors including your school, major, and GPA to determine if you're eligible.

Ascent also offers its Progressive Repayment plan to qualified borrowers. It allows you to begin with smaller payments at the start of the repayment term and then gradually pay more each month over time. If you borrow with a cosigner, they can be released after you make as few as 12 monthly payments. However, cosigners on loans for international students do not qualify.

pros

- Doesn’t charge application fees or origination fees

- Offers discounts of 0.50 to 1 percentage points when making automatic payments

- Can get a 1% cash-back reward after you graduate

- Grace periods from 9 to 36 months

cons

- May find lower interest rates with some competitors

- International students don’t have option to release cosigners

Minimum income

$30,000 (waived with a cosigner or for undergrads with less than two years of credit history)

Loan terms

5, 7, 10, 12, 15, or 20 years

Loan amounts

$2,001 minimum up to your school’s annual cost of attendance; lifetime limits of $200,000 for undergrads and $400,000 for graduates

Eligibility

Must be a U.S. citizen or DACA student enrolled at least half time at an eligible institution. International students with a qualified cosigner may also qualify. Applicants who can’t meet financial, credit, or other requirements may qualify with a cosigner.

Credible rating

To determine the best student loan companies, Credible evaluated lenders based on several different categories, including: rates and fees, loan terms, eligibility, repayment options, and customer support. We assigned a score out of five stars to each lender based on our findings.

Read our full methodology.

Overview

Nelnet Bank (Member FDIC) provides private student loans at competitive rates for undergraduate, graduate, and health professional degrees. You'll need a FICO credit score in the mid to high 600s to qualify. Borrowers with bad credit can apply with a cosigner, which may help them qualify and could reduce their interest rate.

Cosigners on Nelnet student loans can be released after 24 consecutive on-time payments (see disclaimer). You can also get a 0.25% interest rate reduction when you sign up for automatic payments (see disclaimer). There are no loan origination or application fees, but Nelnet does charge fees for late payments of insufficient funds.

pros

- Rates are competitive for borrowers or cosigners with strong credit

- Rate discount of 0.25 percentage points for autopay

- Cosigners can be released after 24 on-time payments

- Offers deferment and payment assistance programs

cons

- Charges fees for late payment and insufficient funds

- Doesn’t guarantee deferment and forbearance options

Loan terms

5,10,15* (IO, Deferred, Immediate)

Loan amounts

$1,000 to $125,000 for undergraduate, $1,000 to $175,000 for graduate, $1,000 to $500,000 for graduate health professions

Eligibility

All states and US Territories

Credible rating

To determine the best student loan companies, Credible evaluated lenders based on several different categories, including: rates and fees, loan terms, eligibility, repayment options, and customer support. We assigned a score out of five stars to each lender based on our findings.

Read our full methodology.

Overview

SoFi offers fixed- and variable-rate student loans to help undergraduates, graduates, and parents finance their education. These loans can cover up to the total cost of attendance, with a minimum loan of $1,000. Students must be enrolled at least half-time in a degree-seeking program at an eligible school and be a U.S. citizen, a U.S. permanent resident, or a non-U.S. permanent resident alien.

SoFi has multiple repayment plans, allowing students to pick terms that best fit their financial situations, with cosigner release after 12 months of consecutive on-time payments. Borrowers can reduce their rates by 0.25% or 0.125% with SoFi's Continuing Scholar Discount on subsequent loans. Plus, a $250 cash bonus with a 3.0 GPA or higher for full-year loans or $100 cash back for single-semester loans.

Lender Disclosures

pros

- Top customer service ratings

- Valuable member benefits

- No fees

- Cosigner release after 12 months of on-time payments

cons

- No disclosed credit or income requirements

- Shorter repayment terms than some lenders

Loan amounts

$1,000 minimum, up to your school’s annual cost of attendance

Eligibility

Must be a U.S. citizen or DACA student enrolled at least half-time at an eligible institution. International students with a qualified cosigner may also qualify. Applicants who can’t meet financial, credit, or other requirements may be eligible with a cosigner.

Credible rating

To determine the best student loan companies, Credible evaluated lenders based on several different categories, including: rates and fees, loan terms, eligibility, repayment options, and customer support. We assigned a score out of five stars to each lender based on our findings.

Read our full methodology.

Loan Amounts

$1,000 up to school-certified cost of attendance (aggregate $300,000 limit for an undergraduate loan, $350,000 limit for a graduate or graduate certificate loan)

Overview

Custom Choice offers undergraduate loans ranging from $1,000 to $300,000 and graduate or graduate certificate loans up to $350,000.

You can get a 0.25% autopay discount, and up to a 0.25% on-time payment discount, plus a 2% principal reduction for graduating with at least a bachelor’s degree. You may apply with a cosigner if you can't qualify on your own, and you can release them after making 12 consecutive on-time principal and interest payments.

Custom Choice doesn't charge any fees whatsoever, even late fees. The lender also offers a forbearance program that lets you pause payments if you experience a financial hardship, an existing or persisting medical condition, a natural disaster, or suffer temporary unemployment.

pros

- You can reduce your rate by 0.5 percentage points with autopay and on-time payments

- Cosigner release available after 12 consecutive on-time monthly principal and interest payments

cons

- No mobile app for managing student loans

- Does not offer refinancing options for existing student loans

Minimum income

$1 (must have positive income)

Loan terms

5, 7, 10, 15, or 20 years

Loan amounts

$1,000 to $300,000 for an undergraduate loan, or up to $350,000 for a graduate or graduate certificate loan (In Iowa, the minimum is $1,001, and in Massachusetts, it’s $6,001.)

Cosigner release

After making 12 consecutive on-time principal and interest payments

Eligibility

Available to borrowers in all 50 states. The student must be a U.S. citizen or permanent resident alien, and must be the legal age of majority at the time of application or at least 17 years of age if applying with a cosigner who meets the age of majority requirements in the cosigner's state of residence. Eligible noncitizens, such as international students and DACA residents, can also qualify by applying with a cosigner who’s a U.S. citizen or permanent resident. Lender Disclosures

Credible rating

To determine the best student loan companies, Credible evaluated lenders based on several different categories, including: rates and fees, loan terms, eligibility, repayment options, and customer support. We assigned a score out of five stars to each lender based on our findings.

Read our full methodology.

Loan Amounts

$1,500 up to school’s certified cost of attendance less aid

Overview

Massachusetts Educational Financing Authority (MEFA) offers student loans to borrowers with good credit. However, you won't be able to see your potential rate before applying.

The lender doesn't charge any fees and its rates are competitive, though MEFA only offers two repayment terms. You can add a cosigner to your loan if you're unable to qualify, but only one repayment plan allows you to release your cosigner.

pros

- Doesn’t charge any fees

- Low maximum rate compared with some lenders

- Can borrow up to the school-certified cost of attendance

cons

- No discounts for borrowers

- Limited repayment terms

- No prequalification available

Loan amounts

$1,500 minimum, up to school-certified cost of attendance

Eligibility

Must be a U.S. citizen or permanent resident, enrolled at least half-time at a degree-granting, nonprofit institution, and must maintain satisfactory academic progress. Must have no history of default on an education loan and no history of bankruptcy or foreclosure in the past 60 months.

What is a part-time student?

A part-time student is someone who takes fewer credit hours than the number their school considers a full-time course load.

Being a part-time student usually means moving through a degree program at a slower pace, but it can also offer more flexibility. Students who want to balance school with work, parenting, or other responsibilities often choose part-time enrollment in college.

However, enrolling part-time can affect your financial aid options. Federal student loans require at least half-time enrollment, and some private lenders prefer borrowers to take more credits.

Full-time vs. part-time students

Whether you enroll full- or part-time affects more than your class schedule. It determines which types of financial aid you can access, how quickly your loans enter repayment, and how long it takes to earn your degree.

These are the main differences so you can see where part-time status helps, and where it limits your options:

| | |

|---|

| Students prioritizing fastest path to graduation | Students balancing work, family, or other obligations alongside school |

Credit hours per semester | | Fewer than 12 hours:

Half-time: 6 - 11 hoursLess-than-half-time: 5 hours or less |

Federal student loan eligibility | Eligible for Direct Subsidized, Unsubsidized, and PLUS loans | Eligible only if enrolled at least half-time; below half-time, no federal loan access |

Private student loan eligibility | Broadly available from nearly all lenders | Available from a smaller pool of lenders (e.g., Ascent, College Ave, Custom Choice, Abe); approval may be more difficult for loans under $2,000 |

Pell Grant, need-based grants | Full award amount, if eligible | Still eligible, but award is prorated based on enrollment status |

Federal work-study program | | Still eligible as a part-time student |

Repayment while enrolled in school | Loans remain in deferment while in school | Federal and most private loans enter repayment if you drop below half-time |

Your enrollment status is determined by the number of credit hours you're taking. A part-time student is generally one who's taking fewer classes than their school's definition of full-time enrollment. The Department of Education classifies full-time enrollment as at least 12 credit hours and half-time enrollment as at least six credit hours per term.

If your school uses “clock hour” programs or another nonstandard enrollment system, you can contact the school to find out what it considers full-time or half-time. Some schools consider 24 clock hours per week full-time enrollment, while schools with a quarter system may consider 36 quarter hours per academic year to be full-time.Keep in mind that many lenders prefer to issue larger loans over smaller ones, which may make it more difficult to qualify for a part-time student loan.

The rejection rate for private student loan applications of less than $2,000 is around 40%, compared with 13% for loan amounts of $15,000 or more, according to data compiled by Credible.

Can I get a student loan as a part-time student?

If you're enrolled for fewer than six credit hours, you fall below the half-time threshold for federal loans, including Direct Subsidized Loans, Direct Unsubsidized Loans, and Direct PLUS Loans. That doesn't mean you're out of options.

Applying for as many scholarships and grants as possible may help you cover the cost of your part-time education. It's still important to submit the FAFSA to find out what other aid you may qualify for.

Important

Grad PLUS loans are not available to new borrowers as of July 1, 2026. Parent PLUS loans will still be offered, but the loan limits have been lowered to $20,000 per year per dependent, with an aggregate limit of $65,000.

If you don’t qualify for federal student loans, you can look for private lenders that offer loans for students enrolled less than half-time. You'll generally need good to excellent credit to qualify for a private student loan. Some lenders offer private student loans for bad credit, but these loans generally come with higher interest rates compared to the rates offered to borrowers with good credit.

If you decide to take out private student loans to pay for school as a part-time student, be sure to consider as many lenders as possible to find the right loan for you.

No matter if you take out federal or private student loans, be sure to consider how much the loans will cost you over time. This way, you can plan for any added expenses.

Tips for finding the best part-time student loans

The following tips can help you find the best private part-time student loans:

- Prequalify with multiple lenders: Many lenders allow you to prequalify for a loan on their websites without affecting your credit. This is a good way to gauge the interest rate you may be offered.

- Compare rate quotes: Once you have a few quotes, compare them side by side to determine which is best for your financial situation. Consider factors like interest rates, repayment terms, fees, and discounts.

- Apply: Once you've selected the right lender for you, formally apply on its website. Note that you'll likely need to provide supporting documentation with your application, such as pay stubs or tax returns.

- Consider your options after receiving a decision: If the lender denies your application, think about applying with a cosigner or waiting until you've improved your credit before reapplying on your own. You typically need at least a 670 FICO score and a steady income for approval, so holding off until you can meet these requirements, or applying with someone who does, can improve your odds of getting a loan.

- Only borrow what you need: To minimize the amount of interest you pay, it’s best to only borrow what you truly need for your education. You can use your school’s cost of attendance as a starting point, but be sure to adjust it to your needs. For example, if you plan to live at home with your parents, you can avoid borrowing to cover on-campus housing costs.

How much can I borrow in part-time student loans?

If you're enrolled at least half-time, you can borrow up to the annual limit for federal student loans each year, which varies by your year in school, loan type, and dependency status (dependent vs. independent). For example, a first-year dependent undergraduate student can borrow up to $5,500, with no more than $3,500 in subsidized loans. Federal loans also have aggregate limits, and once you meet these, you can't borrow any more funds.

Private student loans generally come with minimum and maximum loan amounts. For instance, Custom Choice offers loans from $1,000 to $300,000 for undergraduate students.

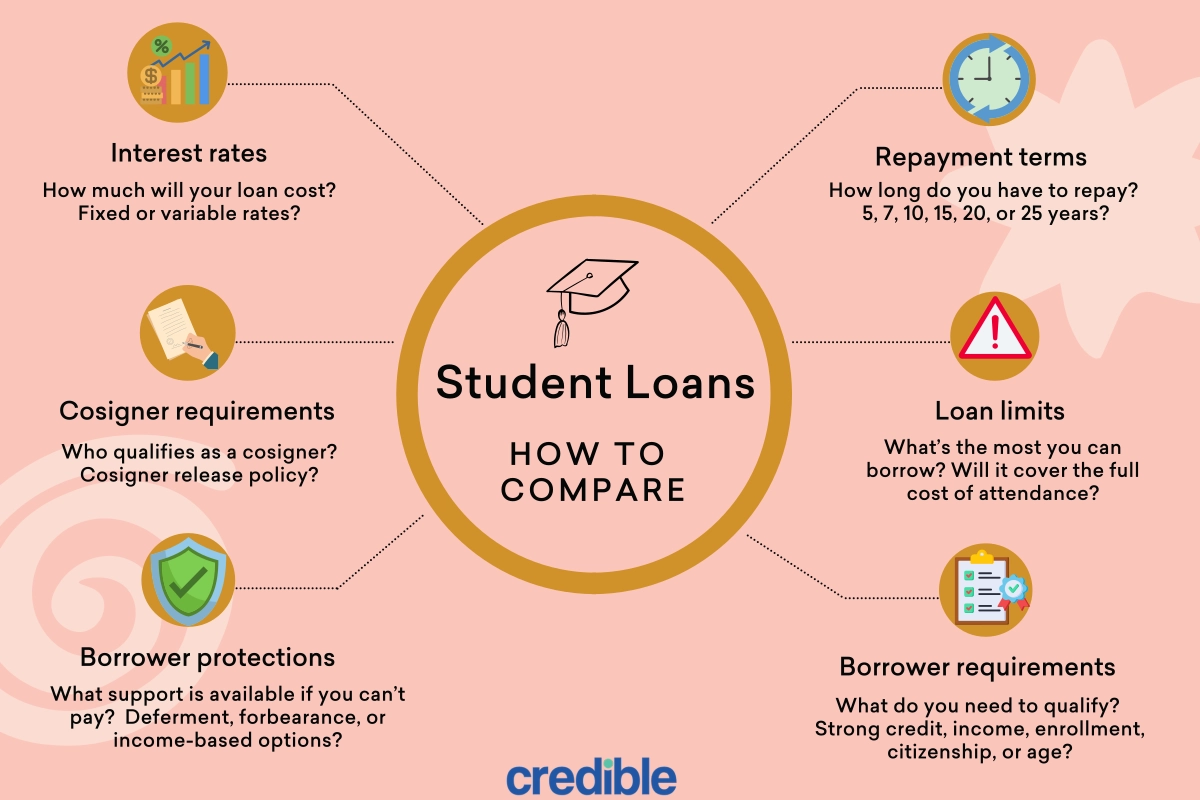

How to choose a part-time student loan

It’s typically best to start with federal student loans. But if you’ve exceeded your federal loan limits, you may need to turn to private student loans. When evaluating part-time student loan options, consider the following factors:

- Interest rates: Private student loans can have fixed or variable interest rates, and minimum and maximum rates vary by lender.

- Loan limits: The loan amount you’re offered depends on your credit, enrollment status, cost of attendance, and other factors.

- Repayment plans: Private lenders may offer the option to make full payments, interest-only payments, or fixed payments while you’re enrolled in school. Check repayment terms for how long you have to repay the loan.

- Borrower requirements: Pay attention to any fees the lender charges. Common fees include late fees, returned payment fees, and insufficient funds fees.

- Cosigner requirements: Find out whether you need a cosigner to get approved for a loan. It's also worth noting if they offer a cosigner release.

- Borrower protections: Not all lenders offer hardship options such as forbearance if you’re struggling to make payments, so it’s a good idea to ask potential lenders about this.

In addition, pay attention to any fees the lender charges, like late fees, returned payment fees, and insufficient funds fees. Look for any discounts the lender offers for enrolling in autopay or meeting other requirements. Rate discounts can help you save on your overall loan cost.

Editor insight: “If you're having trouble getting approved, I recommend applying with a cosigner. Even if you don't technically need one to qualify, having a cosigner with strong finances could help you secure a lower interest rate than you'd get on your own. Just make sure you both understand the responsibilities involved.”

— Renee Fleck, Student Loans Editor, Credible

How to borrow for school as a part-time student

If you decide to take out a part-time student loan, follow these four steps:

- Fill out the FAFSA: To apply for federal student loans and other federal aid, you'll need to complete the Free Application for Federal Student Aid (FAFSA). How much you qualify for in federal student loans will depend on your financial information, enrollment status, dependency status, and what year you are in school.

- Take any scholarships or grants first: You might qualify for school-specific college scholarships or grants through the FAFSA. Unlike student loans, you won't have to worry about repaying these types of financial aid. You can also find scholarships and grants elsewhere — such as through local or national businesses or nonprofit organizations.

- Opt for federal loans next: If you still need to borrow money to cover your school expenses, federal student loans are usually a good place to start. This is because federal student loans come with federal benefits and protections, including access to income-driven repayment plans and student loan forgiveness programs. Your school will let you know what federal student loans you're eligible for after you submit the FAFSA.

- Use private loans to fill the gaps: If you've exhausted your scholarship, grant, and federal student loan options, private student loans could help fill any financial gaps. A private student loan is also likely your only student loan option if you're enrolled less than half-time.

You'll generally need good to excellent credit to qualify for a private student loan. Some lenders offer private student loans for bad credit, but these loans generally come with higher interest rates compared to the rates offered to borrowers with good credit.

Good to know

You may not qualify for the maximum student loan amount, especially as a part-time student. Your school calculates your cost of attendance and subtracts your Student Aid Index and any financial aid received to determine how much you can borrow.

Alternative financial aid for part-time students

If student loans aren’t an option, you still have other ways to help cover the cost of school:

- Scholarships: Many scholarships require full-time enrollment, but some private scholarships are available to part-time students. Use scholarship search sites like Fastweb, GoingMerry, and Bold.org to filter through awards for part-time students.

- Grants: Grants, like scholarships, don’t have to be repaid. You can find grants for part-time students, though award amounts are typically smaller than those for full-time students. Federal grants you may be eligible for include the Pell Grant, Federal Supplemental Educational Opportunity Grant (FSEOG), and TEACH Grant. You can also get grants through your state, school, or private organizations.

- Part-time work: Income from a part-time job can help you cover some of your school expenses. Even a few hours a week can make a meaningful difference.

- Employer tuition reimbursement: Many employers offer tuition reimbursement benefits. Check with your HR department to see what’s available. Keep in mind that these programs often have requirements, such as staging with the company for a certain period after completing your coursework or choosing a program related to your job.

What happens to my student loans if I drop below half-time?

For most federal and private student loans, dropping below half-time status generally means you'll have to begin repaying your loans.

Before you drop any classes, make sure to double-check how it'll affect your enrollment status and whether you'll need to start making student loan payments.

If your student loans have a grace period (typically six months), you'll have that much time before you must start making payments if you drop below half-time.

Why trust Credible?

The Credible editorial team is independent and unbiased. Partners do not influence our editorial content. To help you find the best student loan for your situation, we conduct thorough research and analyze thousands of lender data points. Using data-driven methodologies, we score criteria that are important to you. This allows us to objectively rank student loan lenders and products. To learn more, read our methodology below.

Methodology

To determine the best part-time student loan lenders, Credible collected more than 1,000 points of data on two dozen companies and evaluated them on several different categories: repayment options, eligibility, interest rates, loan terms, and customer support. Based on our findings, we assigned a score out of five stars to each lender. Below are the weightings assigned to the general categories for the best student loan companies — which comprise individual criteria that are also weighted.

- Repayment options: 30%

- Eligibility: 25%

- Interest rates: 20%

- Loan terms: 15%

- Customer support: 10%

While the best lender for you will depend on your unique needs and financial circumstances, these findings should help answer your questions and assist you in your search for the best student loan.

Learn more about our methodology.

FAQ

What is half-time enrollment?

Can you get student loans if you’re part-time?

Which part-time student loan is the best?

Is there a downside to being a part-time student?

What is considered half-time for student loans?

How much of my Pell Grant will I get for part-time?

Can I get a scholarship if I’m enrolled part-time?

Can I use the FAFSA as a part-time student?

Meet the expert:

Kelly Larsen

Kelly Larsen is a student loans editor at Credible. She has spent over 10 years covering personal finance, with expertise in mortgage and debt management.