Credible takeaways

- The average total cost of a bachelor's degree is about $124,000 at a public in-state school and nearly $204,000 at a private university, based on 2025-26 data.

- The full cost of college includes tuition, fees, housing, meals, books, supplies, and other miscellaneous educational expenses.

- You can reduce your total costs by choosing a more affordable school, living at home, or earning college credits in advance to shorten your time in school.

- Common ways to pay for college include 529 savings plans, grants, scholarships, student loans, and employer tuition assistance.

The average cost to attend a four-year public in-state university is nearly $31,000 per year, according to the College Board. That brings the total cost of a bachelor's degree to about $124,000 — including tuition, fees, housing, books, and other expenses.

But that's just a starting point. Costs are much higher for out-of-state students at public colleges and even more for those attending private universities. What you'll actually pay depends on several key factors, including the type of school you choose and where you live while earning your degree.

This guide explores the average cost of a bachelor's degree across different types of institutions and offers tips to reduce your total costs.

Current private student loan rates

Average cost of a bachelor's degree by school type

One of the biggest factors that affects how much you'll pay for college is the type of school you attend. The table below shows the average cost of attendance for the 2024-25 academic year. These totals include tuition and fees, room and board, books and supplies, transportation, and other miscellaneous educational expenses.

Source: College Board

What factors influence the cost of college?

The cost of earning a bachelor's degree includes more than just tuition. Total college costs typically include tuition and fees, books and supplies, room and board, transportation, and other miscellaneous educational expenses.

How much you'll pay depends on several key factors:

- Type of school: Public in-state colleges tend to be the most affordable. Private schools and public out-of-state colleges usually cost more.

- Living situation: Living on campus is often the most expensive option. You can reduce costs by living off campus or staying at home with family.

- Time to graduate: The longer it takes to finish your degree, the more you'll spend on tuition and living expenses.

Keep in mind

You may have other indirect costs depending on your situation. For example, if you’re attending college on the other side of the country, you might need to budget for flights or long-distance travel.

According to the data, in-state public colleges are typically the most affordable, while private nonprofit schools are the most expensive. However, these numbers don't tell the whole story.

Robert Farrington, founder of The College Investor, recommends focusing on what you'll pay after financial aid is applied.

“The net price is what you actually pay (or need to borrow) out of pocket, and that's the metric you should focus on,” says Farrington. “The sticker price can be misleading. For example, many private colleges have high prices, but they also offer generous financial aid packages, making the net price significantly less.”

So while private colleges often look more expensive up front, they may be more affordable than you think once you factor in scholarships and grants.

How to save on the cost of a bachelor's degree

With the high cost of college, many families are looking for ways to cut expenses. Two of the biggest factors that affect how much you'll pay are the type of school you attend and your living situation. Choosing a lower-cost college or living at home while in school can significantly reduce your overall expenses.

Attending a nearby public university is often one of the most affordable options. If you're interested in a private college, look for schools that offer strong financial aid packages to help keep your out-of-pocket costs down.

Farrington also suggests getting a head start on your degree to save both time and money.

“The more college credits you start with, the less time (and money) you'll need for college,” he says.

Some students try to save money by starting at a less expensive college and transferring later. However, some experts advise against this approach.

According to Mark Kantrowitz, author of “How To Appeal for More College Financial Aid,” it often takes longer to earn a degree when students transfer, which can cancel out the potential savings.

Jack Wang, a wealth adviser who specializes in financial aid, agrees. He warns about what he calls “transfer leakage” — when students lose credits during the transfer process and have to take extra classes to graduate.

How to pay for your bachelor's degree

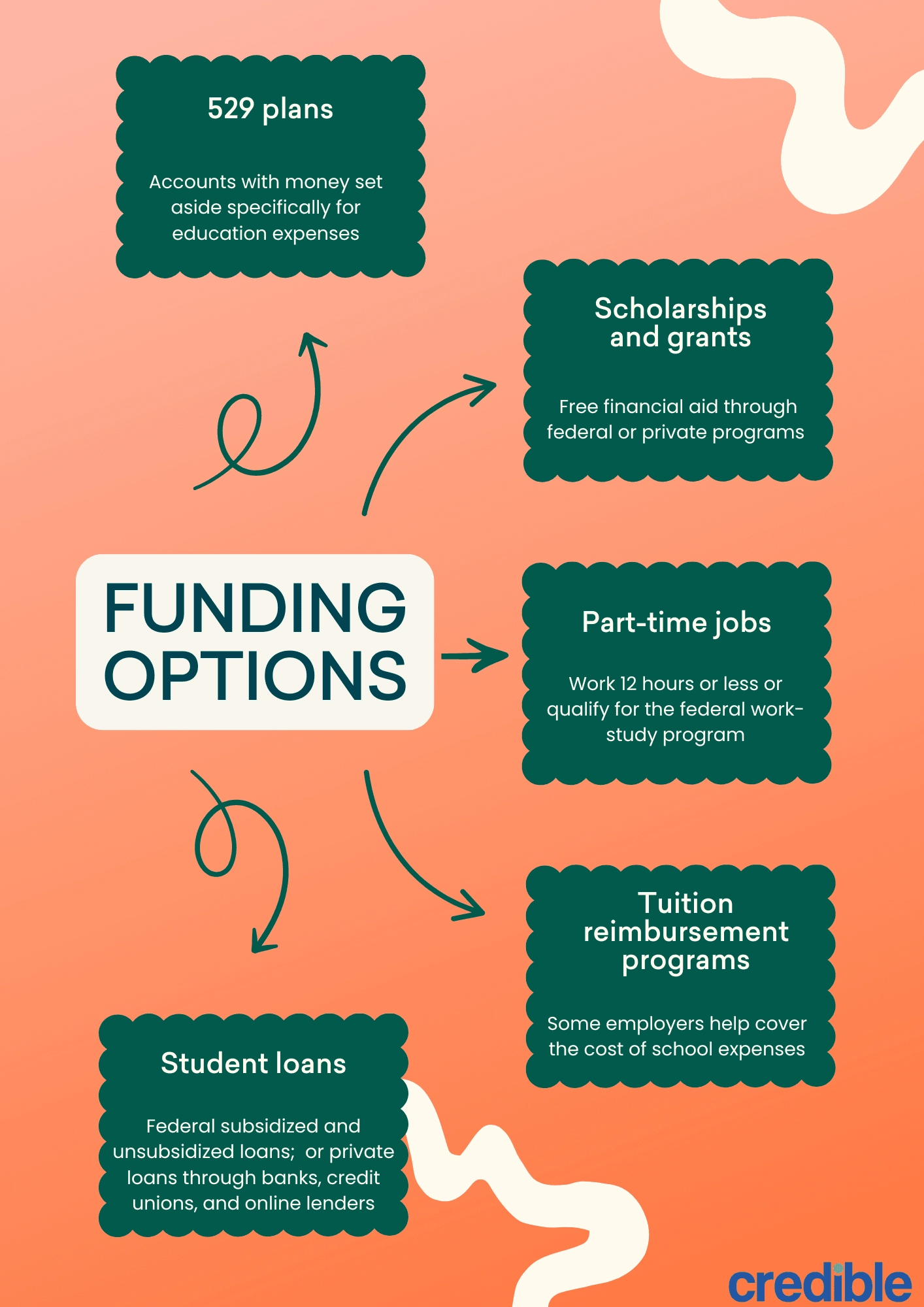

Paying for a bachelor's degree usually requires a combination of resources. Most families can't cover the full cost out of pocket, so it's important to understand your options.

529 plans

One way to plan ahead is with a 529 college savings plan. These accounts offer tax advantages for families who set aside money specifically for education expenses. Contributions grow tax-deferred, and withdrawals are tax-free when used for qualified education expenses like tuition, fees, books, and room and board.

You can open a 529 plan through your state or a financial institution. In some cases, your state may even offer a tax deduction or credit for contributing to its plan.

Scholarships and grants

In addition to savings, you can reduce your college costs by applying for financial aid. The most valuable type is free aid, such as scholarships and grants. Federal grants are available through programs like the Pell Grant, while colleges and private organizations may offer additional scholarships or need-based awards.

Part-time work

While many students work during college to help pay for tuition, Kantrowitz advises limiting your work hours, if possible. While it sounds counterproductive to lower your earnings during your college years, Kantrowitz notes that students who work full-time are less likely to graduate compared to those who work 12 hours or less.

Another option is the federal work-study program. This form of financial aid allows eligible students to earn money through part-time jobs while in school. Work-study is typically reserved for students with financial need, and the money earned doesn't have to be repaid.

Tuition reimbursement programs

If you're already in the workforce, check whether your employer offers a tuition reimbursement program. Some companies provide tax-free benefits to help cover the cost of tuition, books, and other school-related expenses, and in some cases, even student loan repayment.

Under IRS rules, employer-paid educational assistance is tax-free up to $5,250 per employee per year. That limit applies to both tuition and student loan repayment benefits combined. Any amount above that becomes taxable.

Student loans

Another common way to pay for college is with student loans. The federal government offers two main types: subsidized and unsubsidized loans. Subsidized loans are for students with financial need, and they don't accrue interest while you're in school, which can help keep your total costs lower. Unsubsidized loans start accruing interest right away, but they're one of the most accessible forms of student aid.

If federal loans don't fully cover your expenses, you can also apply for private student loans through banks, credit unions, or online lenders. These loans are based on your credit score and income, and they often come with higher interest rates, especially if you don't have strong credit.

Most undergraduates need a cosigner to qualify for a private loan. In fact, 84% of borrowers who applied for a private student loan in 2024 did so with a cosigner, according to data from the Credible marketplace.

Editor insight: “I strongly recommend submitting the FAFSA every year of your undergraduate studies, regardless of your family's income level. You might still be eligible for federal student loans, which usually have lower starting interest rates than private loans and more flexible repayment options. Plus, if you end up working in government or public service after graduation, you could qualify for loan forgiveness programs that aren't available with private loans.”

— Richard Richtmyer, Senior Student Loans Editor, Credible

What to know before taking out student loans

Student loans are one of the most common ways to pay for college, but they're also one of the most expensive. Many undergraduate students take out loans without fully understanding what it means for their financial future.

“Every dollar you borrow will cost about two dollars by the time you repay the debt,” says Kantrowitz. “Live like a student while you're in school, so you won't have to live like a student after you graduate.”

Kantrowitz also shares a simple rule of thumb: If your starting salary after college is higher than your total student loan balance, you'll likely be able to pay off your loans within 10 years. But if your salary is lower, repayment may take longer and could strain your budget.

Before you borrow, look up the average starting salary in your intended field. It's one of the best ways to make sure the debt you take on will be manageable after graduation.

FAQ

Is a bachelor’s degree worth the cost?

Open

What is the cheapest way to get a bachelor’s degree?

Open

How can I reduce the amount I borrow for college?

Open

What financial aid options are available?

Open

Can you make $100,000 a year without a degree?

Open