Paying off student debt can be a long-term financial issue for many Americans. To determine where this debt is impacting Americans most, we analyzed data from the U.S. Department of Education and the U.S. Census Bureau.

Our analysis reveals:

- States with the highest student loan debt per borrower

- States where it will take the longest to repay loans

- States where borrowers will pay the most in total over time

States where student loan debt is highest

Borrowers in Maryland carry the highest average student loan balance in the country, at $43,354 per borrower.

To calculate the average balance per borrower, we compared the total student loan debt to the number of borrowers in each state.

The top ten states with the most student loan debt per borrower are:

- Maryland — $43,354

- Georgia — $41,012

- Virginia — $39,532

- Florida — $38,874

- Illinois — $38,604

- New York — $38,501

- Hawaii — $38,328

- Delaware — $38,285

- California — $38,266

- North Carolina — $37,927

The states with the lowest average balances per borrower include North Dakota ($28,269), Iowa ($29,981), South Dakota ($30,249), Wyoming ($30,651), and Wisconsin ($31,548).

Editor insight: “High balances don't have to be a long-term burden. If you qualify for a lower interest rate, refinancing student loans can make repayment more manageable. An income-driven repayment plan, which caps your monthly federal student loan payments based on your income and family size, can also help.”

— Richard Richtmyer, Student Loans Managing Editor, Credible

States where student loans take the longest to pay off

We not only wanted to determine where Americans carry the heaviest student loan debt, but also in which states these debts will take the longest to repay, based on the state's median household income and the average loan balance.

By using the Federal Aid Office's Loan Repayment Simulator, we determined the states where Americans are projected to take the longest time to repay their student loans under the Income-Contingent Repayment (ICR) Plan.

Payments on the ICR plan equal the lesser of 20% of discretionary income or the amount you'd pay on a repayment plan with a fixed payment over 12 years, adjusted to your income. Under the ICR plan, Mississippi ranks first on the list as the state where student loans take the longest to repay. Those in Mississippi have a projected loan payoff date of May 2039, with the total amount paid coming to $54,768.

Other states with long payoff periods include:

- West Virginia — December 2038

- Louisiana — June 2038

- Arkansas — May 2038

- Kentucky — December 2037

Alabama, New Mexico, and Oklahoma all have estimated payoff dates of October 2037.

Editor insight: “Don't let a long repayment timeline derail your overall financial goals. Making extra payments as small as $25 a month or applying windfalls like employment bonuses toward your student loan balance can significantly shorten your loan term.”

— Richard Richtmyer, Student Loans Managing Editor, Credible

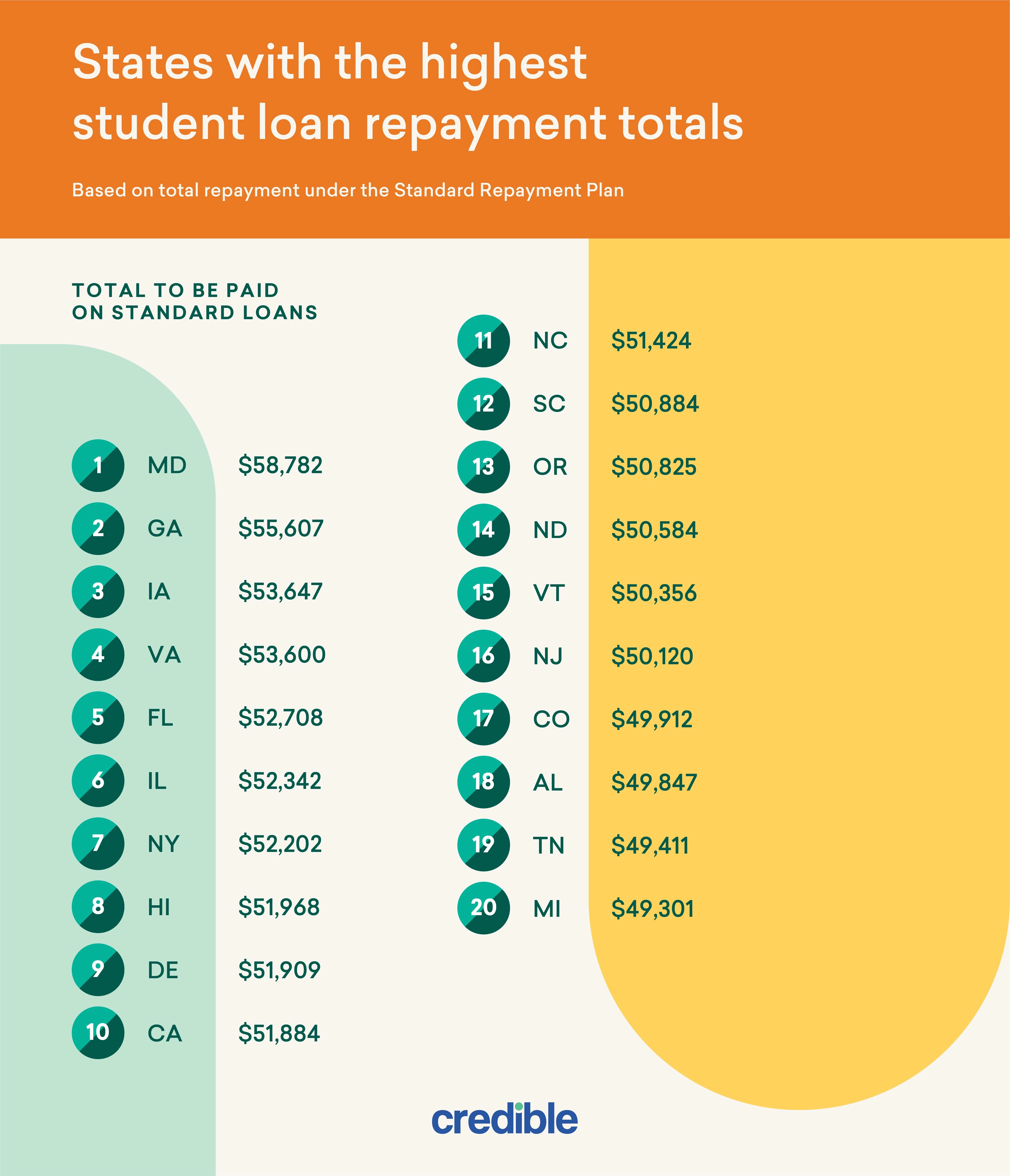

States Where Borrowers Pay the Most on Student Loans

While income-driven plans may stretch repayment timelines, borrowers on the Standard Repayment Plan (fixed monthly payments over 10 years) often pay more in total due to larger loan balances and interest.

We identified the states where borrowers are projected to pay the highest total amounts under the Standard Repayment Plan. Maryland leads the list, with borrowers expected to repay an average of $58,782 over the life of their loans.

Other high-repayment states include Georgia ($55,607), Iowa ($53,647), and Virginia ($53,600).

The states with the lowest repayment totals under the Standard Repayment Plan include South Dakota ($41,014), Wyoming ($41,559), Wisconsin ($42,775), and Oklahoma ($42,909).

Editor insight: “If your goal is to pay the least amount in interest, I recommend the debt avalanche method, where you focus on paying off your highest-interest loans first, while making minimum payments on the rest. This is especially beneficial if you have large, high-rate loans where interest can add up quickly.”

— Richard Richtmyer, Student Loans Managing Editor, Credible

Whether you're planning for college, repaying debt, or exploring options like income-driven plans or refinancing, understanding how your state stacks up can help you make more informed financial decisions.

Methodology

We used the most recent data available from the U.S. Department of Education's Federal Student Aid office and the U.S. Census Bureau to determine these rankings. Repayment projections were modeled using the Federal Student Aid Loan Simulator for both the Standard Repayment Plan and Income-Contingent Repayment (ICR) Plan.

For media inquiries, contact [email protected].

Fair Use

When using this data and research, please attribute by linking to this study and citing Credible.