The best way to compare and buy insurance online

See real quotes from top carriers side-by-side. No agent calls, no spam, no surprises.

HOW CREDIBLE WORKS

Better coverage takes less time than you think

We pull what we can from public records so you only answer what we genuinely need.

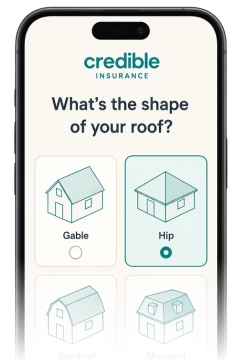

- Tell us a few things about you & your property

- Most questions are already filled in based on your address. You're just confirming.

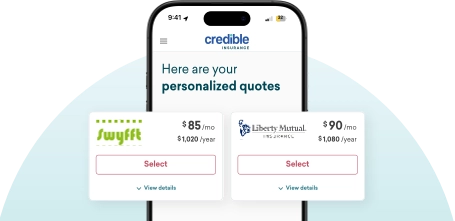

- Compare quotes from top carriers side-by-side

- Real prices, real deductibles. Customized by what matters to you most.

- Finish and bind your policy — all online

- Pick a quote, e-sign, and get covered. No phone calls with an agent unless you want one.