Credible takeaways

- Federal student loans are your best option, as most don't require a credit check.

- While it's possible to get a private student loan with bad credit, you'll likely need to add a creditworthy cosigner to your application to get approved.

- Some alternatives to student loans include grants, scholarships, and income-share agreements.

Student loans for bad credit can be challenging to find, but there are still ways to borrow money for college if you have a low credit score or limited credit history. Federal student loans have no credit score requirements, making them a popular option with bad-credit borrowers. Federal student loans made up 86% of all borrowing in the last academic year, according to the College Board.

If federal student loans aren't enough to cover the cost of your education, you can turn to private student loans to bridge the gap. While private loans have minimum credit score criteria, you can utilize strategies such as adding a cosigner to your application to improve your chances of qualifying for a loan.

Here's what you need to know about taking out student loans with bad credit.

Compare private student loan rates

What’s considered bad credit for student loans?

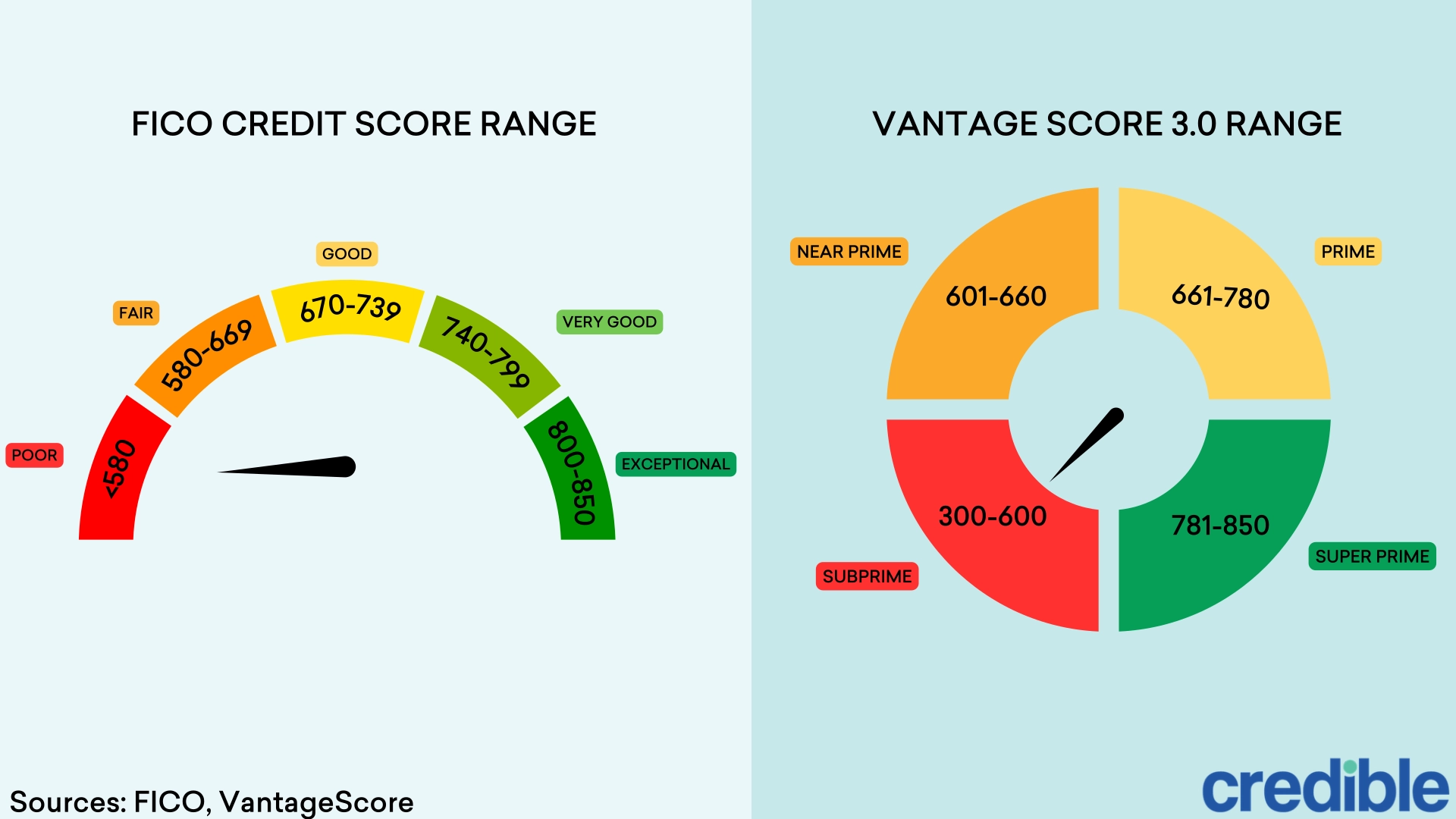

A bad credit score is a rating that signals to student loan lenders that you pose a higher risk as a borrower. The specific number that defines a “bad” score depends on the credit scoring model being used:

- FICO score: Anything below 580 is classified as “poor.”

- VantageScore 3.0: Anything below 600 is classified as "poor" or “very poor.”

How a bad credit score affects borrowing

- High risk: A bad credit score suggests a history of missed payments, high debt utilization, or poor credit management.

- Higher interest rates: To compensate for the risk, lenders charge bad-credit borrowers significantly higher interest rates for student loans.

- Loan denials: A bad score can make it difficult to get approved for student loans or other debt, such as mortgages and auto loans.

Can you get a student loan with bad credit?

You can get a student loan with bad credit, but your options depend entirely on whether you apply for federal or private student loans.

Credit scores affect your ability to secure funding in two main ways:

1. Federal student loans (best for bad credit)

For most federal student loans, your credit score doesn’t matter.

- No credit check: The government does not check your credit history for standard undergraduate Direct Subsidized or Unsubsidized federal student loans.

- Equal rates: Everyone receives the same fixed interest rate, regardless of their credit score.

2. Private student loans (most difficult for bad credit)

Private lenders view a low credit score as a major red flag.

- Credit requirements: To get approved on your own, you typically need "good" credit, which is a FICO score of at least 670.

- Higher costs: If you are approved with bad credit, lenders will charge you significantly higher interest rates, costing you more over the life of the loan.

- Fewer options: A low score limits your choice of repayment terms and lender perks.

Keep in mind

Credit score requirements for student loans vary. Most federal student loans have no credit requirement, while private lenders set their own criteria to determine loan approvals, including requirements for bad credit.

Federal vs. private student loans

Federal student loans for bad credit

If you have a low credit score, consider federal student loans first. A credit check generally isn’t part of the federal requirements for student loans, which is why maximizing the federal loan borrowing limit can be the best path forward in most situations.

Direct Subsidized and Unsubsidized Loans, the most common types of federal student loans, are available to students regardless of their credit history. If subsidized or unsubsidized Direct Loans aren’t enough, graduate and professional students can rely on grad PLUS loans to help pay for school.

Grad PLUS loans require a credit check, but not a minimum credit score. The Department of Education looks for an adverse credit history, like recent bankruptcy, foreclosure, or repossession. If you have one, you’ll need an endorser (the equivalent of a cosigner for private student loans) who has good credit or documentation showing that your adverse credit was due to extenuating circumstances. Either way, you must also complete credit counseling before you can get the loan.

Important

Grad PLUS loans will no longer be available to new borrowers starting July 1, 2026. Graduate and professional students will only be able to borrow Direct Unsubsidized Loans, which don’t require a credit check.

Submit a Free Application for Federal Student Aid (FAFSA) to see if you qualify for Direct Loans despite having bad credit.

Improve your credit before applying for a student loan

If you still have several years of school ahead before graduating, it might be a good idea to start improving your credit today. This could work in your favor the next time you need a loan.

Your credit is impacted by multiple factors, but here are some of the most immediate and effective ways to improve it:

- Repay debt on time: A large part of your FICO score (35%) is calculated based on your payment history. This includes whether you've made the minimum monthly payment on time for your outstanding debts. Make sure that you're paying off your student loans and other debts on time and for the full amount due.

- Lower unpaid debt balances: Your debt, such as credit card balances, can affect your student loan approval. If you lean on your credit too heavily, lenders might perceive you as a high-risk borrower who's financially overextended. Before applying for a student loan with bad credit, consider paying down your other revolving debt.

- Avoid opening new accounts: When you apply for new lines of credit, lenders conduct a hard credit check, which temporarily lowers your credit score. Applying for new credit cards or other installment loans in addition to your student loan within a short period could drag your score down when you're trying to improve it.

- Review your credit report: Sometimes your credit score might be dragged down by a data reporting error on your credit report. For example, your score could be lowered if the report includes a defaulted debt that's actually not yours. Request a copy of your free credit report from AnnualCreditReport.com, and if you see a mistake, submit a dispute with each of the three credit bureaus: Experian, Equifax, and TransUnion.

- Become an authorized user: Asking a responsible loved one to add you as an authorized user on their credit card can help you build and improve your credit, as their history of on-time payments gets added to your credit report.

Editor insight: “You may start to see small credit score improvements within 30 to 45 days of making on-time payments and lowering debt balances, but it can take several months to see a meaningful change. If you know you’ll need to borrow, I recommend working on your credit for a few months before applying for a student loan.”

— Renee Fleck, Student Loans Editor, Credible

Student loan options for parents with bad credit

If you're a parent with bad credit, you have two main student loan options:

Parent PLUS loans

Parent PLUS loans have historically allowed you to borrow up to your child’s school-certified cost of attendance, minus other financial aid received. A credit inquiry that checks for an adverse credit history — such as a recent bankruptcy or foreclosure — is required to qualify, but there’s no minimum credit score needed.

However, parent PLUS loans will be capped at $20,000 per year per dependent student and $65,000 total per student starting in the 2026-27 school year. Existing borrowers may be able to continue using parent PLUS loans under the full cost-of-attendance rules for up to three more academic years.

Private parent loans

Some private lenders offer parent loans, but they typically require a minimum credit score and strong income. If you have bad credit, qualifying may be more difficult — though a steady income or other financial strengths could improve your chances with certain lenders.

Use a cosigner to get a student loan with bad credit

Regarding private student loans, some lenders may offer the option to include a cosigner on your loan agreement. A cosigner is an individual who meets the lender’s income and credit criteria and agrees to take liability for any unpaid loan balance you fail to pay.

By leveraging a cosigner’s creditworthiness, you have a better chance of getting approved and securing a better interest rate and terms. Since this is a major responsibility, a cosigner is typically someone with a close relationship to the primary borrower (for example, the student’s parent, spouse, grandparent, or older sibling).

Some lenders offer a cosigner release feature in their loan agreements. If your credit improves later on, this feature lets you remove your cosigner’s obligation from the debt. But you’ll need to meet the lender’s release requirements first.

Keep in mind

Not all private student lenders accept cosigners. Those that do might not offer cosigner release. Make sure expectations are clear between you and your potential cosigner for a smooth borrowing process.

Look into private bad-credit student loans

Some private student loans are specifically designed for students with no or low credit. These loans operate similarly to a traditional private student loan but might offer lower borrowing amounts, higher interest rates, or a shorter term.

When shopping around for bad-credit student loans, make sure you’re weighing details like unique eligibility requirements, loan-related fees, deferment options (if any), and whether they offer flexible repayment (e.g., interest-only payments while in school).

Pros and cons of bad-credit student loans

Bad-credit student loans have benefits and downsides to consider.

Pros

- Offer access to the funds you need

- Can help you build credit

- A cosigner can help you get a better rate

Cons

- Higher interest rates

- Able to borrow less

- Could add to your cycle of debt

Details on the pros

- Offer access to the funds you need: While bad-credit student loans often have higher interest rates, they can allow you to get the funding you need for your education if you've hit your federal student loan limits.

- Can help you build credit: Making your student loan payments on time every month can help you boost your credit score.

- A cosigner can help you get a better rate: If you have a creditworthy cosigner, you can qualify for a lower rate on your loan, even if your credit is bad.

Details on the cons

- Higher interest rates: Bad-credit loans typically have higher interest rates, meaning you'll pay more for your loan than you would with good credit.

- Able to borrow less: Larger loans can take longer to pay off, so lenders typically won't approve borrowers with bad credit for large loan amounts.

- Could add to your cycle of debt: If your credit score is low because you're trapped in a cycle of credit card debt, for example, adding another loan on top of that can make the problem worse. If you're unable to make your student loan payments, your credit could suffer even more.

Alternatives to student loans for bad credit

Federal and private student loans are just one type of financial aid you can turn to. Alternative aid options to look into include:

- Grants: This kind of aid typically doesn't typically have to be repaid. You can find college grants at the federal and state levels, as well as through your school, private companies, and nonprofits.

- Scholarships: This is another form of gift aid that awards students based on financial need or merit. You can get a scholarship for certain areas of study, communities, interests, and/or skills.

- Income-share agreements (ISAs): ISAs are a type of alternative loan that offers lump-sum financing up front for school, which you'll repay using a fixed percentage of your future salary for a certain number of years.

FAQ

What are the 2026 changes to federal student loans?

Open

Can I get student loans for bad credit?

Open

What is considered bad credit when it comes to student loans?

Open

Are federal or private student loans better if I have bad credit?

Open

Which is the best private student loan lender for bad credit?

Open

Do I need a cosigner to get a student loan with bad credit?

Open

What credit score do you need for a student loan?

Open

Will applying for a bad-credit student loan affect my credit?

Open

How do I qualify for student loans with bad credit?

Open

Can you be denied a student loan because of bad credit?

Open

How do you apply for a student loan with bad credit?

Open