Credible takeaways

- Most flight training programs don't qualify for federal student aid because they aren't accredited.

- Some private lenders like Sallie Mae offer career training loans that can help cover flight school costs.

- Before borrowing to pay for flight school, explore airline-sponsored training programs and aviation scholarships and grants.

A career as a pilot can offer strong earning potential and the opportunity to travel while you work. Airline pilots earned a median annual salary of $232,140 in 2025, according to the Bureau of Labor Statistics, while commercial pilots averaged $123,220.

But flight training can be expensive. If you’re starting with no experience, earning your Airline Transport Pilot (ATP) certificate can cost around $123,995, according to ATP Flight School.

Here’s a look at the best flight school loans and how to compare your options.

Compare private student loan rates

Can you get a loan for flight school?

You can get federal or private student loans for flight school, but the type of loan available depends on your aviation training program.

“Flight schools offer loans primarily through private lenders, credit unions, and other organizations. Some might offer federal student loans, but they are in the minority,” says Dan Bubb, a former airline pilot and aviation historian at UNLV Honors College.

Because many flight schools don't meet federal aid requirements, students often need to turn to private lenders that finance career training or certificate programs. Some schools also offer their own financing options.

Editor insight: “Taking on debt for flight school can be risky, especially if you rely on private student loans with higher interest rates and fewer protections than federal options. Before borrowing, I suggest looking into scholarships and airline-sponsored training programs to reduce or even replace the need for loans.”

— Renee Fleck, Student Loans Editor, Credible

Federal flight school loans

Federal student loans from the Department of Education are available to help finance flight school, but eligibility is contingent on the school being accredited, participating in Title IV federal financial aid programs, and offering qualifying degree or certificate programs.

ATP Flight School, the nation's leading flight training program, does not participate in federal student aid. However, several four-year colleges offer aviation degree programs that qualify, including:

- Polk State College

- Aviator College

- Orange Coast College

- Purdue University

- The Ohio State University

- Baylor University

- University of Oklahoma

To determine whether your school qualifies for federal financial aid, you can search the Department of Education's accreditation database. Below are the federal student loan options and their interest rates for the 2025-26 school year:

Source: U.S. Department of Education

You must satisfy several criteria to be eligible for federal student loans. These include being a U.S. citizen or an eligible noncitizen, having a valid Social Security number, enrolling in an accredited degree program at an approved school, and maintaining satisfactory academic progress.

To apply for these loans, students must complete the Free Application for Federal Student Aid (FAFSA).

Note

Many flight schools do not qualify for federal student loans as they are often classified as trade schools and lack accreditation.

Private lenders offering flight school loans

Private student loans can potentially fund your aviation training if you can't get federal student loans. These loans are typically only available to students enrolled in a four-year degree-granting program. However, some private lenders offer loans for a certificate- or career-based program, which may allow you to get a loan for flight school. Some loan options and lenders include:

- Sallie Mae Airline Career Loan

- Ascent Career Training Loan

- College Ave Undergraduate and Graduate Career Loans

Private vs. federal flight school loans

When comparing federal vs. private flight school loans, be aware that private loans don't have the same repayment options or benefits as federal loans. Private lenders don't offer income-driven repayment plans or loan forgiveness opportunities. You also may be unable to take advantage of deferment or forbearance options.

“Federal loans are preferable because there is much greater flexibility when it comes to repayment,” says Martin Lynch, president of the Financial Counseling Association of America. “Private lenders have not been very creative when it comes to repayment plans that suit the income of their borrowers.”

Most students are likely to be able to get lower interest rates with federal loans, which are set by the government, do not require a credit check, and are the same for all borrowers. Most private lenders determine your student loan interest rates based largely on your credit score and financial history. A creditworthy cosigner could help you get a lower rate on a private student loan for flight school.

Pros and cons of flight school loans

While loans can help, it’s important to weigh the advantages against the drawbacks of borrowing for flight school before taking on the debt.

Pros

- Can cover the full cost of training

- Federal loans offer flexible repayment options

- Some private lenders accept certificate programs

- Airline stipends or bonuses may reduce debt

Cons

- Not all schools qualify for federal aid

- Private loans may require a cosigner

- Limited income-based repayment options

- High overall cost of becoming a commercial pilot

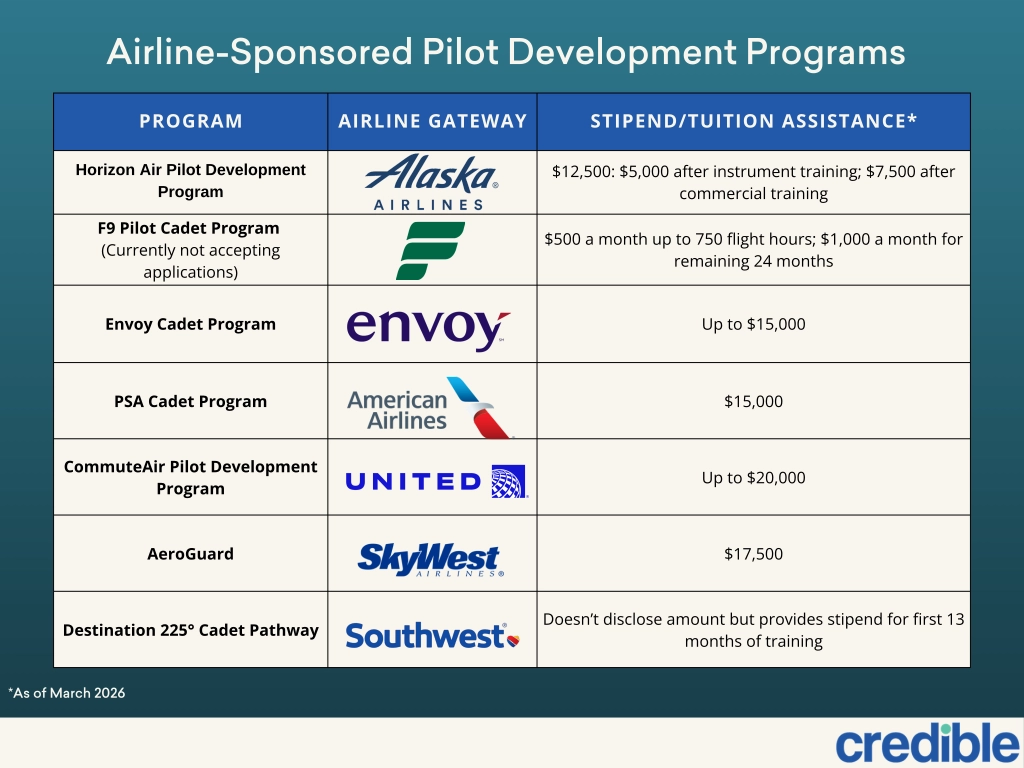

Airline-sponsored pilot training programs

Some airline-sponsored training programs offer stipends or tuition assistance to help you finance your education, giving you a pathway to flying for a major airline. These are several of the ones to consider:

Scholarships and grants for flight school

You can get financial awards through scholarships and grants that you don't have to pay back. Aviation students can look into these:

- Amelia Earhart Memorial Scholarships: Aviation scholarships for females; qualifications vary by scholarship type.

- Navigate Your Future Scholarship: Must be a senior in high school and accepted or enrolled in an aviation-related program at an accredited university.

- EAA scholarships: Requires a 2.5 GPA or higher; applications open Oct. 1.

- AOPA Flight Training Scholarships: Awards range from $250 to $14,000. The 2026 application periods are April 1 to June 30, and Oct. 1 to Dec. 31.

- Lyons Aviation Foundation scholarships: Offers $1,500 minimum and up to the entire cost of a private pilot certificate.

- National Business Aviation Association (NBAA): Available to college students studying aviation.

- Delta Propel Scholarship Path: Available to candidates nominated by Delta's affiliate organizations for flight training, and provides a direct route to a Delta cockpit.

- United Aviate Academy: Various scholarships available after acceptance into the program.

“Students can go to the Federal Aviation Administration's website to see which scholarships and grants are available, in addition to doing an Internet search to find out which private foundations offer scholarships and grants. Flight schools also might have scholarship and grant information,” says Bubb.

FAQ

Is there a way to get flight school paid for?

Open

Which loan is best for pilot training?

Open

Do airlines pay for flight school?

Open

Will FAFSA pay for pilot school?

Open

Can I qualify for a flight school loan if I attend school half-time?

Open

Is it hard to get a loan for flight school?

Open

How do most people pay for pilot school?

Open

What is the cheapest way to become a pilot?

Open

Are there any federal grants for flight school?

Open

How do lenders decide if I qualify for a flight school loan?

Open

How long does it take to get a flight school loan?

Open

When do I start repaying my flight school loan?

Open