Our goal is to give you the tools and confidence you need to improve your finances. Although we receive compensation from our partner lenders, whom we will always identify, all opinions are our own. Credible Operations, Inc. NMLS # 1681276, is referred to here as "Credible."

Content provided by Credible. Although we do promote products from our partner lenders who compensate us for our services, all opinions are our own.

This article first appeared on the Credible blog.

A personal loan can help you cover almost any personal expense — but before you get one, it’s important to compare as many lenders as you can to find the right loan for you.

As you consider lenders, keep in mind that the best personal loans should provide competitive interest rates, a wide selection of loan terms, and inclusive eligibility requirements. Credible makes it easy to compare personal loan rates from multiple lenders.

Best personal loans for every situation

Each borrower has unique needs and financial circumstances. Thankfully, a wide variety of personal loan lenders offer personal loans to fit nearly every situation.

Here are Credible’s partner lenders that offer personal loans:

Achieve

Best for: Consolidating high-interest debt

Achieve personal loans range from $10,000 to $50,000 with terms from two to five years. If you use at least 85% of your loan proceeds to pay off existing debt, you could get a better rate. You might also qualify for a lower rate by adding a cosigner or showing proof of retirement savings.

Pros

- Could get a better rate by using at least 85% of the loan to consolidate debt, adding a cosigner, or showing proof of retirement savings

- Quick approval decisions

- Fast loan funding

Cons

- Must borrow at least $10,000

- Origination fees from 1.99% to 4.99%

- Not available in Nevada

Avant

Best for: Borrowers with poor credit

With Avant, you can borrow $2,000 to $35,000 with repayment terms from two to five years. If you’re approved, you could get your funds as soon as the next business day.

Pros

- Accepts poor and fair credit scores

- Fast loan funding

- Variety of loan uses

Cons

- Not available in Colorado, Iowa, Hawaii, Vermont, Nevada, New York, or West Virginia

- Origination fees up to 4.75%

- Charges late and dishonored payment fees

Axos Bank

Best for: Borrowers with excellent credit

Axos Bank offers personal loans from $10,000 to $50,000 with repayment terms from three to six years. If you’re approved, you could get your funds as soon as the next business day.

Keep in mind that you’ll need good to excellent credit to qualify for a loan from Axos Bank.

Pros

- Fast loan funding

- Variety of loan uses

- No prepayment penalty

Cons

- Could be difficult to qualify if you don’t have good credit

- Origination fees from 0% to 2%

- Charges late and insufficient funds fees

Best Egg

Best for: Borrowers with good credit

Best Egg offers loans from $2,000 to $50,000 with terms from two to five years. In addition to your credit score, Best Egg also considers more than 1,500 proprietary credit attributes from sources that include external data providers and your “digital footprint” — which means you might have an easier time qualifying with Best Egg compared to traditional lenders.

Pros

- Competitive rates

- Fast loan funding

- Accepts borrowers with poor and fair credit

Cons

- Origination fees from 0.99% to 8.99%

- Charges late fees

- Not available in Iowa; Vermont; Washington, D.C.; or West Virginia

Discover

Best for: Long repayment terms

If you’re looking for a longer repayment term, Discover might be a good option for you — you can borrow $2,500 to $35,000 with terms from three to seven years. Just keep in mind that choosing a longer term means you’ll pay more in interest over time.

Pros

- Repayment terms up to seven years

- No origination fees

- If you decide you don’t want the loan, you can return the funds within 30 days interest-free

Cons

- Charges late fees

- Might be difficult to qualify if you have poor credit

- No discounts

LendingClub

Best for: Borrowers who need a cosigner

If you need a cosigner, LendingClub could be a good choice — it’s one of the few lenders that allow cosigners on personal loans. You can borrow $1,000 to $40,000 with a three- or five-year repayment term.

Pros

- Accepts borrowers with poor or fair credit

- Allows cosigners

- Being turned down doesn’t hurt your credit score

Cons

- Origination fees from 3% to 6%

- Charges late fees

- Funding time can be longer compared to other lenders

LendingPoint

Best for: Borrowers with near-prime credit

LendingPoint specializes in working with borrowers who have near-prime credit — usually meaning a credit score in the upper 500s or 600s. With LendingPoint, you can borrow $2,000 to $36,500 with terms from two to six years.

Pros

- Accepts near-prime credit

- Streamlined approval and application process

- Fast loan funding

Cons

- Origination fees from 0% to 8%

- Not available in Nevada or West Virginia

- Rates can be higher than other lenders

LightStream

Best for: Large loan amounts

LightStream could be a good option if you need to borrow a large amount — you can borrow $5,000 to $100,000 and could have your funds as soon as the same business day if you’re approved.

Most LightStream loans have terms ranging from two to seven years, but if you use your loan for home improvements, you could have up to 12 years to repay it.

Pros

- Can borrow up to $100,000

- Fast loan funding

- 0.50% autopay discount

Cons

- Might be difficult to qualify if you have poor credit

- Not available in Rhode Island or Vermont

- Doesn’t disclose minimum income requirements

OneMain Financial

Best for: Borrowers with below-average credit

Unlike many other lenders, OneMain Financial doesn’t have a minimum required credit score — which means you might be able to qualify with poor or even no credit. In addition to your credit, OneMain Financial will also consider your financial history, credit history, income, expenses, and loan purpose to determine creditworthiness.

You can borrow $1,500 to $20,000 with terms from two to five years. Keep in mind that collateral might be required in some cases.

Pros

- No minimum credit score

- Fast loan funding

- Previous customers might qualify for larger loans

Cons

- Rates can be higher than other lenders

- Might require collateral

- Will have to visit a branch location to discuss your options if you’re approved

Payoff

Best for: Consolidating credit card debt

If you’re looking to consolidate credit card debt, Payoff could get a good option — its personal loans can only be used for this purpose. You can borrow $5,000 to $40,000 with repayment terms from two to five years.

Pros

- Free FICO score updates

- If you lose your job, Achieve will work with you on payments

- Offers scientific personality, stress, and cash flow assessments to help you get a better understanding of your personal finances

Cons

- Origination fees from 0% to 5%

- Loans can only be used for credit card consolidation

- Not available in Massachusetts, Nevada, or Ohio

PenFed

Best for: Borrowers who need a cosigner

If you only need a small loan, PenFed could be a good option — you can borrow as little as $600 up to $50,000 with terms from one to five years.

Keep in mind that while you don’t have to be a PenFed member to apply for a loan, you’ll have to join the credit union if you are approved and want to accept the loan.

Pros

- Can borrow as little as $600

- Allows cosigners

- No fees

Cons

- Must join the credit union to accept a loan if you’re approved

- Doesn’t disclose minimum income requirements

- Funds are disbursed by mail, which can take longer

Prosper

Best for: Home improvement loans

Prosper offers personal loans from $2,000 to $50,000 with terms from two to five years. Keep in mind that because Prosper is a peer-to-peer lender, loan funding can take longer compared to other lenders — however, you might also get your funds in as little as one business day.

Pros

- No minimum income requirement

- No prepayment penalty

- Can borrow up to $50,000

Cons

- Origination fees from 2.4% to 5%

- Charges late fees

- Not available in Iowa or West Virginia

SoFi

Best for: Borrower perks

With SoFi, you can borrow $5,000 to $100,000 with repayment terms from two to seven years. SoFi borrowers also have access to several perks, such as unemployment protection, career coaching, and investing advice.

Pros

- Can borrow up to $100,000

- No fees

- Borrower perks like unemployment protection and investing advice

Cons

- Doesn’t disclose minimum income or credit requirements

- Not available in Mississippi

- Funding can take longer compared to other lenders

Universal Credit

Best for: Borrowers who want to build their credit

Universal Credit offers a variety of tools and resources to help borrowers build their credit, such as free credit score monitoring and personalized recommendations. Loan amounts range from $1,000 to $50,000.

Pros

- Fast loan funding

- Free credit score monitoring, educational tools, and personalized recommendations to help you build your credit

- If you’re using your loan to consolidate credit card debt, you might get a lower rate by allowing Universal Credit to pay off the cards directly

Cons

- Rates can be higher than other lenders

- Origination fees from 5.25% to 8.99%

- Not available in Arkansas; Kansas; Maine; South Carolina; Vermont; Washington, D.C.; Wisconsin; or West Virginia

Upgrade

Best for: Fast loan funding

Upgrade offers personal loans from$1,000 to $50,000 with three- or five-year terms. If you’re approved, you could get your funds within a day of clearing necessary verifications.

Pros

- Accepts poor and fair credit

- Fast loan funding

- Free credit monitoring and educational resources

Cons

- Origination fees from 1.85% to 8.99%

- Not available in West Virginia

- Doesn’t disclose minimum income requirements

Upstart

Best for: Borrowers with little to no credit history

In addition to your credit, Upstart will consider your education and job history to determine creditworthiness — which means you might qualify even if you have little to no credit history. Upstart offers loans from $1,000 to $50,000.

Pros

- Might be able to qualify with little to no credit history

- Accepts poor and fair credit

- No prepayment penalty

Cons

- Origination fees from 0% to 10%

- Charges late and returned check fees

- Not available in Iowa or West Virginia

You can easily compare your prequalified rates from these lenders with Credible. It’s 100% free and checking your rates won’t affect your credit.

Methodology

To find the “best companies,” Credible looked at loan and lender data points from 10 categories to give you a well-rounded perspective on each of our partner lenders. Here’s what we considered:

- Interest rates

- Repayment terms

- Repayment options

- Maximum loan amount

- Loan funding time

- Fees

- Discounts

- Customer service availability

- Whether the minimum credit score is available publicly

- Whether consumers could request rates with a soft credit check

Our hope is that this will be a win-win situation for you and us — we only want to get paid if you find a loan that works for you, not by selling your data. This means Credible will only get paid by the lender if you finish the loan process and a loan is disbursed. Additionally, Credible charges you no fees of any kind to compare your loan options.

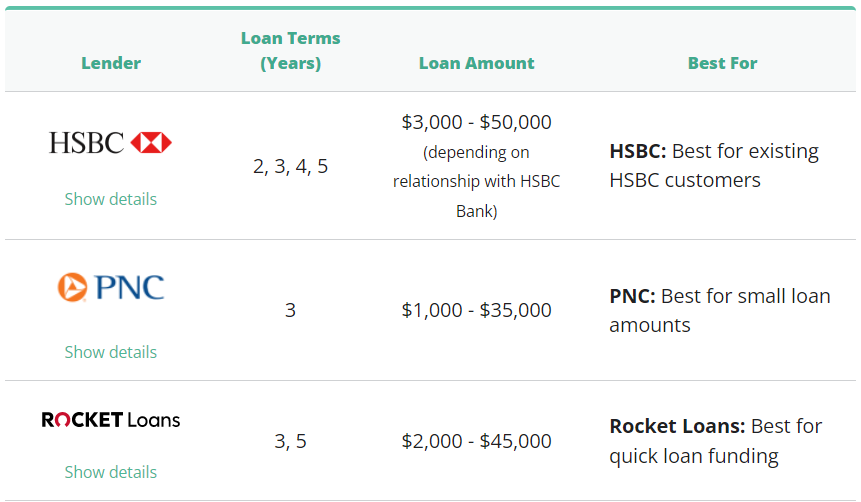

Other personal loans to consider

Here are more personal loan companies Credible evaluated. Keep in mind that these lenders aren’t offered through Credible, so you won’t be able to easily compare your rates with them on the Credible platform like you can with partner lenders listed above.

How to take out a personal loan

If you’re ready to take out a personal loan, follow these four steps:

- Research and compare lenders. Be sure to compare as many lenders as possible to find the right loan for your situation. Consider not only personal loan interest rates but also repayment terms, any fees charged by the lender, and eligibility requirements.

- Pick your loan option. After comparing lenders, choose the loan option that works best for you.

- Complete the application. Once you’ve picked a lender, you’ll need to fill out a full application and submit any required documentation, such as tax returns or pay stubs.

- Get your funds. If you’re approved, the lender will have you sign for the loan so the funds can be released to you. The time to fund for a personal loan is usually about one week — though some lenders will fund loans as soon as the same or next business day after approval.

Before you take out a personal loan, it’s important to consider how much that loan will cost you. This way, you can be prepared for any added expenses. You can estimate how much you’ll pay for a loan using a personal loan calculator.

How to qualify for a personal loan

While eligibility criteria can vary by lender, there are a few common requirements you’ll likely come across, including:

- Good credit: You’ll typically need good to excellent credit to get approved for a personal loan — a good credit score is usually considered to be 700 or higher. There are also several lenders that offer personal loans for poor and fair credit – for example, you might be able to get a personal loan with a 600 credit score or lower. However, keep in mind that these loans generally come with higher interest rates compared to good credit loans.

- Verifiable income: Some lenders have a minimum income requirement while others don’t — but in either case, you’ll likely have to show proof of income, such as from a traditional job, self-employment, or other source.

- Low debt-to-income ratio: Your debt-to-income (DTI) ratio is the amount you owe in debt payments each month compared to your income. Lenders typically like to see a DTI ratio of 40% or less — though some lenders might make exceptions to this.

If you don’t qualify

If you don’t qualify for a personal loan, here are a few other options to consider:

- Apply with a cosigner. If you have less-than-perfect credit, applying with a creditworthy cosigner could improve your chances of getting approved for a personal loan.

- Take on a side hustle. Another way to possibly earn some extra cash is by taking on a side hustle. For example, you could sign up to drive for Uber, perform tasks through TaskRabbit, or deliver food with DoorDash.

- Sell stuff you’re not using. See if there are items you’re no longer using in your home, such as electronics, gently used clothing and toys, or even a second vehicle. You might be able to sell them to get the cash you need.

Tip: If you need cash quickly, it might be tempting to take out a short-term loan, such as a payday loan, pawn shop loan, or car title loan. However, these types of loans can come with astronomical rates and fees, which could create a cycle of debt that’s nearly impossible to pay off. Because of these risks, these sorts of loans should only be used as a last resort.

Also be careful of personal loan scams that try to take advantage of people desperate for money. Some warning signs to look out for include lenders demanding upfront payment or pressuring to make an instant decision.

How to get the best personal loan rates

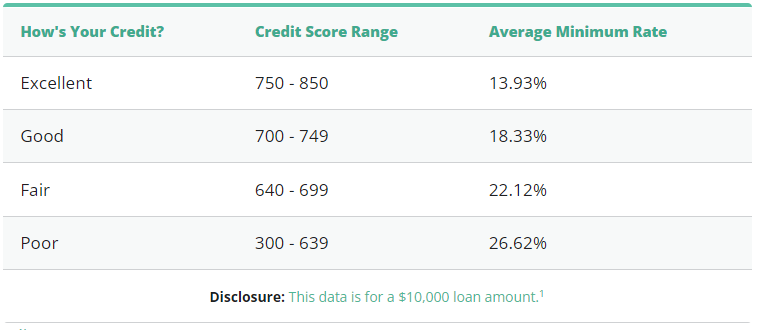

For borrowers who took out a personal loan through Credible during the week of June 28, 2021, three-year personal loan interest rates averaged 11.99% while rates on five-year personal loans averaged 14%.

However, it’s possible to qualify for better interest rates than this. To get the best personal loan rates, you’ll typically need good to excellent credit — in general, the better your credit, the lower your rate. Choosing a shorter loan term could also get you a better rate.

If you want to get approved for better interest rates, here are a few options to consider:

- Compare your rates from multiple lenders. To find the best rate you can get, it’s critical to shop around and compare your options from as many lenders as you can. You might get a better rate from one lender over another.

- Build your credit. If you can wait to take out a personal loan, it could be worth spending some time improving your credit before applying to qualify for a better rate in the future. A few possible ways to do this include paying all of your bills on time, paying down credit card balances, or becoming an authorized user on the credit card account of someone you trust.

- Find a cosigner. Even if you don’t need a cosigner to get approved for a loan, having one could qualify you for a lower interest rate than you’d get on your own. Just keep in mind that a cosigner shares responsibility for the loan, so they’ll be on the hook if you can’t make your payments.

Not all lenders allow cosigners on personal loans, but some do. Credible’s partner lenders that offer cosigned personal loans include:

- Achieve

- LendingClub

- LightStream

- Payoff

- PenFed

- SoFi

Ways to use a personal loan

A personal loan can be used to cover almost any personal expense — though some lenders might restrict their loans for certain purposes. For example, Payoff personal loans can only be used to consolidate credit card debt.

Here are some potential expenses you could cover with a personal loan:

Medical bills

Covering medical expenses is a common source of debt. A personal loan could help you pay for your procedures, then pay them off over a period of time.

Car repairs

If your car needs repairs, a personal loan could get you the funds you need quickly — depending on the lender you choose, you might get your funds as soon as the same or next business day.

Vacations

Vacations can come with a variety of expenses, such as travel and lodging — all of which could be covered by a personal loan.

Debt consolidation

If you use a personal loan to pay off your debt, you might qualify for a lower interest rate than you’ve been paying. This could save you money on interest and potentially help you pay off your debt faster.

Home improvements

A personal loan for home improvements could get you the money you need for home improvements, repairs, or a remodel.

Additionally, home improvement personal loans sometimes offer longer repayment terms that could help keep your monthly payments low — for example, you could have up to 12 years to repay a LightStream home improvement loan.

Major purchases

A personal loan can be used for almost any personal expense — this includes major purchases such as cars, boats, or recreational vehicles.

Moving costs

No matter if you’re moving to another state or just across town, it can be expensive. With a personal loan, you can cover various expenses that come with moving, such as renting a truck or hiring movers.

Coronavirus and personal loans

Due to the financial impact of the COVID-19 pandemic, many lenders began offering various types of coronavirus assistance options to their borrowers, such as deferment and forbearance.

If you have an outstanding personal loan and can’t afford your current payments because of coronavirus, contact your lender to discuss your options. Some lenders are providing special payment relief programs that might help.

Tip: Although the pandemic wears on, many COVID-specific programs are set to expire. If you need additional financial assistance, be sure to talk to your lender to see what options are available to you.

Additionally, consider contacting your local benefits office to see if you’re eligible to receive help with food, insurance, or housing costs. Small business owners might also still qualify for expanded loans or other programs, such as the U.S. Small Business Association’s debt relief options or the Shuttered Venue Operators Grant.

Frequently asked questions about personal loans

Here are the answers to several commonly asked questions regarding personal loans:

What is a personal loan?

A personal loan is a type of installment loan — meaning you borrow a specific amount of money and make payments over a set period of time. Personal loans typically range from $600 up to $100,000 or more with repayment terms from one to seven years, depending on the lender.

Most personal loans are unsecured, so you don’t have to worry about collateral. Also keep in mind that unlike revolving credit (such as credit cards), you can’t access your loan amount more than once. If you want to borrow more, you’ll have to take out another loan.

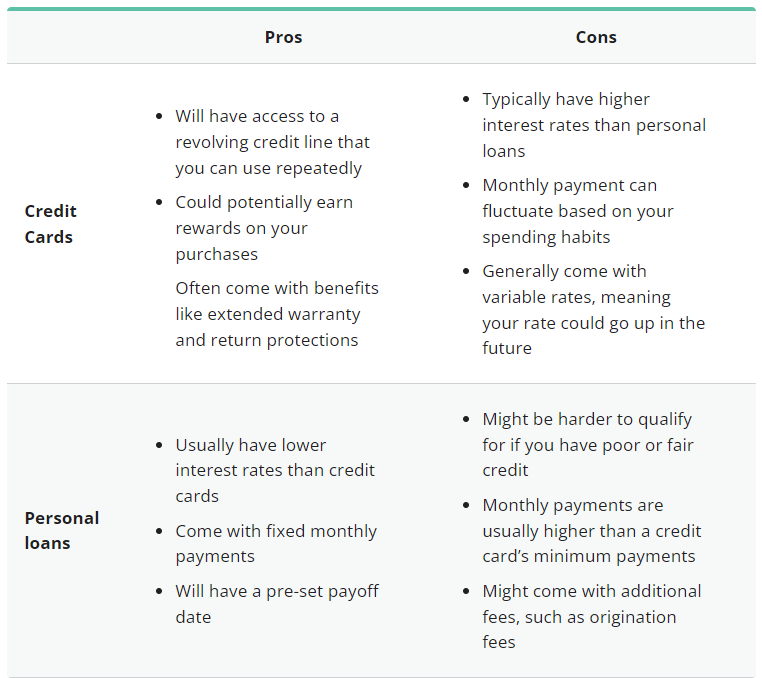

Which is better: a credit card or a personal loan?

When deciding between a personal loan vs. credit card, the right option for you will ultimately depend on your needs and spending habits. Here are a few pros and cons to keep in mind as you compare the two:

What interest rate can I expect?

Interest rates can vary widely from lender to lender, and from borrower to borrower. Keep in mind that the interest rates you’ll be offered depend primarily on three factors:

- Your credit score

- The repayment term you choose

- The lender you pick

What is the difference between APR and interest rate on a personal loan?

The annual percentage rate (APR) and interest rate on a personal loan both refer to borrower costs — though they’re slightly different.

- The interest rate is how much you pay each year to borrow money, expressed as a percentage. Personal loan interest rates are usually fixed, which means your rate and payments won’t ever change. However, some lenders also offer variable-rate loans – meaning your rate and payment could fluctuate over the life of the loan.

- The APR includes not only the interest rate but also other loan fees, such as origination fees. This gives you a more complete picture of your loan costs compared to just the interest rate.

Do personal loans have fees?

This depends on the lender — while some lenders charge fees with personal loans, others don’t. Some potential fees that could come with personal loans include:

- Origination fees, which are deducted before your loan is disbursed

- Late fees, which are charged if you miss your payment due date

- Returned payment fees, which are assessed if you don’t have the funds in your bank account to cover your loan payment

Can I get a personal loan with bad credit?

While you typically need good to excellent credit to qualify for a personal loan, there are some lenders that offer personal loans for bad credit. Keep in mind, though, that borrowers with poor credit generally receive higher interest rates compared to borrowers with good credit.

You could also consider applying with a cosigner to improve your chances of getting approved. Having a cosigner might also help you get a better interest rate, which can save you money on your loan.

Do personal loans hurt your credit?

When you apply for a new loan, the lender will use a hard credit check to review your creditworthiness. This could cause a temporary drop in your credit score — typically five points or less.

However, this impact is usually only temporary, and your score will likely go back up in a few months. Plus, if you make on-time payments on your new personal loan, you might see further improvements to your credit.

How many years can I finance a personal loan?

Generally, personal loan terms range from three to seven years. Available terms vary by lender, so be sure to consider multiple lenders to find a term that fits your needs.

Also keep in mind that the longer the term, the more interest you’ll pay — so it’s usually a good idea to choose the shortest term you can afford.

How much will I qualify for?

Personal loans can range from $600 to $100,000 or more. But the actual amount you’ll qualify for when applying for a personal loan will depend on two factors: the lender’s loan limit and how much of your available monthly income will be required to make your loan payments.

For example, while some lenders will approve $100,000 personal loans, you’ll also have to meet their debt-to-income requirements.

How can I get a quick loan online?

There are several online lenders that offer simple online application processes to get a personal loan. Additionally, many of these lenders offer approval decisions within just a few minutes.

The time to fund for an online personal loan is usually about five business days — but with some lenders, you could have your loan funded as soon as the same or next business day if you’re approved.

Is it better to get a personal loan from your bank?

This depends on your bank. With some banks, borrowers who already have accounts could qualify for loyalty discounts if they take out a personal loan with them. If your bank offers these discounts or other perks, you might be able to reduce your overall loan costs.

However, it’s still important to compare as many lenders as you can in addition to your bank. This way, you can be sure you’re getting the right loan for your needs.

Can I pay my loan off early?

If you can afford it, paying off your loan early can be a great way to save money on interest charges. Many personal loan lenders don’t charge prepayment penalties (fees assessed if you pay off your loan ahead of schedule), but some do.

What happens if I can’t pay back my loan?

Most personal loans are unsecured and don’t require collateral, so your assets aren’t at risk if you default on your loan. However, that doesn’t mean there aren’t consequences.

If you fall behind on your loan payments, the lender will report it to the credit bureaus, which could severely damage your credit score. A loan default can remain on your credit report for up to seven years, which could affect your eligibility for other types of credit later on.

Keep in mind: Lenders can also send your account to collections and pursue legal action against you to force you to repay the loan.

What is the difference between a secured loan and an unsecured loan?

While most personal loans are unsecured, some lenders also offer secured personal loans. Here’s how they compare:

- Secured loans require collateral, such as a vehicle or other item of value. Because these loans are less risky to the lender, they tend to come with lower interest rates compared to unsecured loans. You might also have an easier time getting approved for a secured loan if you have bad credit. However, if you can’t keep up with your payments, the lender could seize your property.

- Unsecured loans don’t require collateral. These loans are riskier for lenders, so they often come with stricter requirements as well as smaller loan amounts. You’ll likely need good to excellent credit to qualify for an unsecured loan.

If you’re ready to find your personal loan, Credible can help: You can compare your prequalified rates from Credible partner lenders in two minutes.

About the authors: Angela Brown is a student loan, personal finance, and real estate authority and a contributor to Credible. Her work has appeared in Fox Business, LendingTree, FinanceBuzz, and Yahoo Finance. Kat Tretina contributed to the reporting for this article.