Our goal is to give you the tools and confidence you need to improve your finances. Although we receive compensation from our partner lenders, whom we will always identify, all opinions are our own. Credible Operations, Inc. NMLS # 1681276, is referred to here as "Credible."

Credible Operations, Inc. NMLS# 1681276, “Credible.” Not available in all states. www.nmlsconsumeraccess.org.

This article first appeared on the Credible blog.

Rising home values mean 44 million Americans now have more than $6 trillion in wealth tied up in their homes. If you’re one of them, you can probably tap your home equity to get cash for a home improvement project, pay off high-interest debt, or take care of unexpected bills.

But first, you’ll need to decide between a home equity loan vs. home equity line of credit (HELOC). A cash-out refinance is another option for tapping your home equity, and if you’re considering a refinance Credible makes it easy to get started. Visit Credible to compare your prequalified rates from multiple lenders in just minutes.

HELOC vs. home equity loan

A home equity loan and a HELOC are both second mortgages. That means you’re taking on additional debt and putting your home up as collateral as a guarantee that you’ll pay back your loan.

But home equity loans and home equity lines of credit differ in important ways that can make one more advantageous than the other. It all depends on your situation.

Differences between a HELOC loan and home equity loan

Here’s a roundup of the most important differences between a home equity loan and a home equity line of credit.

With both a home equity loan and a HELOC, pay attention not just to the interest rate, but closing costs and lender fees, which will factor into your total repayment costs. To help you assess the impact of these fees, lenders must factor them into your annual percentage rate (APR).

With a home equity loan, you often have the option of paying a lender “points” to get a lower interest rate. Keep in mind that if you choose to pay points to get a lower rate on your loan, it will take some time to recoup that expense.

You won’t reap the full benefit of paying points if you pay off your mortgage ahead of schedule. If you take out a 10-year home equity loan and sell your home three years later, for example, you’ll typically be required to pay off your loan at that time.

When a HELOC makes sense

- You might need money in the future, but you don’t know how much

- You have unpredictable ups and downs in your income

- You’re comfortable with a variable interest rate

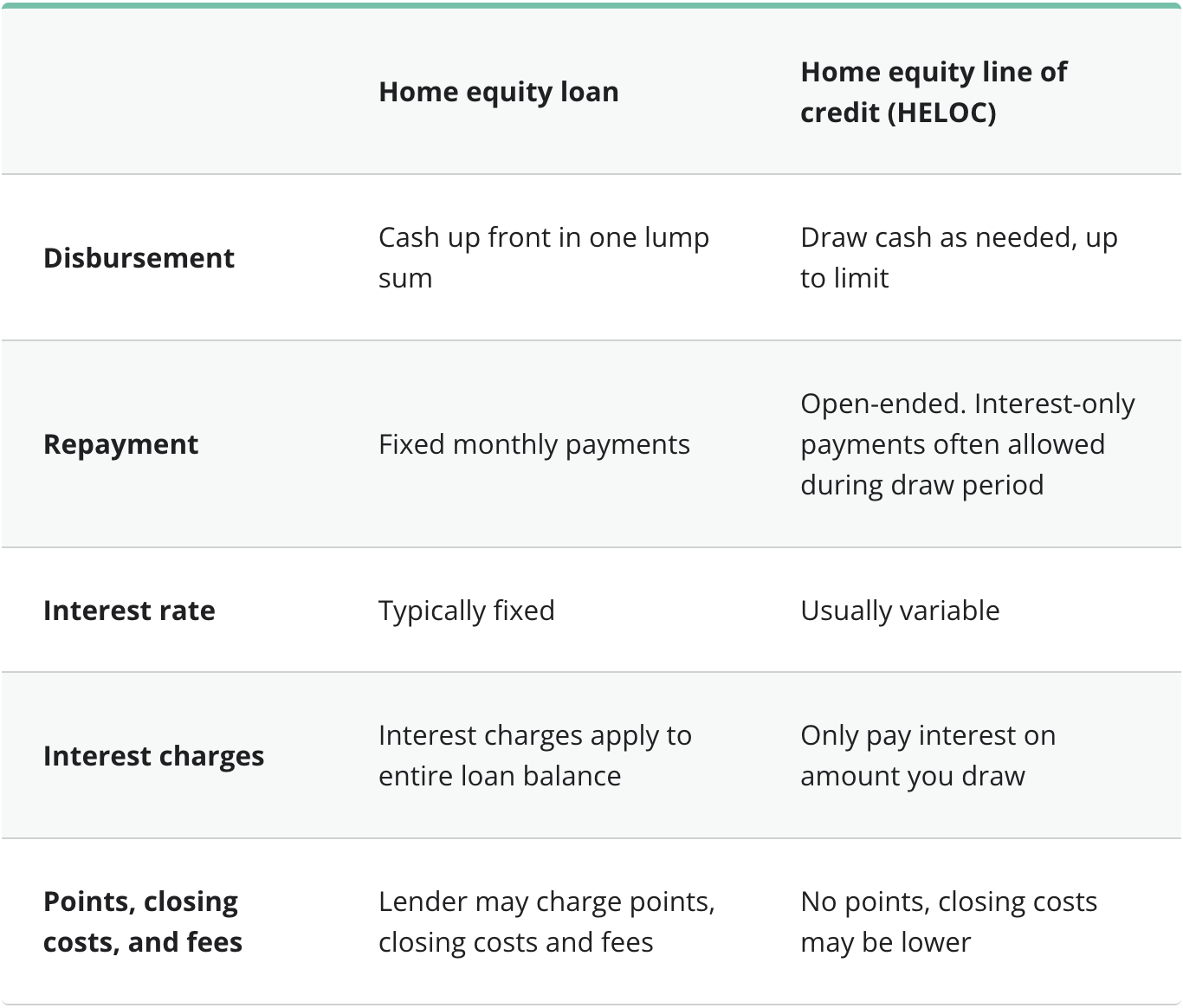

The main difference between a HELOC and a home equity loan is that, with a home equity loan, you receive your loan all at once — the proceeds are “disbursed” to you in a single upfront payment.

A HELOC is a revolving line of credit that works more like a credit card — you’re approved for an upper limit that you can draw against as needed. But like credit cards, HELOC rates are typically higher than for other types of loans, and they’re also variable.

The primary advantage of a HELOC is that you only make interest payments on the portion of your credit line that you’ve tapped. That can be helpful if you have unpredictable ups and downs in your income and expenses. If you’re self-employed, for example, you’ll often have more income coming in during some months than others.

A HELOC can help you make it through lean times, without paying interest on money that you don’t need. But keep an eye out for minimum draw requirements, which could require you to access some or all of your HELOC’s credit limit right away.

Pros and cons of HELOCs

Pros

- Only pay interest on the equity you’re actually tapping at any given time

Cons

- Typically available only from banks and credit unions

- Interest is usually a variable rate, making monthly payments less predictable

- Open-ended loan, making it harder to predict how long you’ll be making payments, and what your total repayment costs will be

Find out if refinancing is right for you. With Credible, you can see actual prequalified rates without impacting your credit score.

When a home equity loan makes sense

- You need money now (short term), and you know exactly how much

- You need to pay off high-interest debt

- You want the certainty of a fixed interest rate

If you know exactly how much you need to borrow, a home equity loan can be a better option than a HELOC. Home equity loans tend to have lower interest rates than HELOCS, and the rates are usually fixed for the life of your loan.

Since you’ll also have a fixed repayment period — of typically 10 or 15 years — you’ll know exactly what your monthly payment will be when you take out your loan.

A home equity loan can be a better choice than a HELOC when you know that you need a predetermined amount of money for a specific purpose, like a home improvement project or paying off high-interest debt. That’s because you’ll typically get a lower, fixed rate than you’d pay on a HELOC.

When using a home equity loan to pay off higher interest debt, keep in mind that you may end up stretching out your payments over a longer period of time, which wipe out some or all of the savings you get by lowering your rate.

If you pay off a five-year car loan with a 10- or 15-year home equity loan, for example, you’ll be making twice or three times as many monthly payments. They’ll be much smaller, but it will take you longer to pay down your loan principal. Make sure to compare the total repayment costs of both options.

Pros and cons of home equity loans

Pros

- Fixed interest rate

- Monthly payment, term, and total repayment costs are fixed

Cons

- A home equity loan is a second mortgage, so interest rates may be higher than your first mortgage

How to calculate your home’s equity

How much you can borrow with a HELOC or home equity loan depends on how much of your home you actually own, and how much of your equity your lender will let you tap.

To calculate the amount of equity you have in your home, subtract your current mortgage balance from the market value of your home.

Let’s say your home was recently appraised for $300,000. If you only owe $200,000 on your mortgage, you have $100,000 in equity.

It wouldn’t be a good idea to cash out all of your equity, and most lenders will require you to keep at least a 10% ownership stake in your home. To be on the safe side, many homeowners will maintain a 20% ownership stake. Think of the amount of equity that lenders will allow you to take out of your home as your “tappable equity.”

How to calculate your tappable equity

Lenders calculate your tappable equity by dividing your combined mortgage debt by your home’s value. The higher your combined loan-to-value (CLTV) ratio, the less equity you have in your home.

To calculate how much you can borrow against your home, multiply your home value by the lender’s maximum CLTV, and then subtract your existing mortgage debt.

Example: 90% CLTV

Let’s say the lender’s maximum CLTV is 90%, and I’m comfortable borrowing up to that limit, which will leave me with a 10% ownership stake in my home.

If I multiply my home’s assessed value of $300,000 by 90%, that’s $270,000 — the maximum amount of combined mortgage debt this particular lender will let me take on. If I already owe $200,000 on my first mortgage, that means I have room borrow another $70,000.

Example: 85% CLTV

Let’s look at another more conservative example. A lender is willing to let me borrow up to 85% of the value of my home, but I’m not comfortable having less than a 20% ownership stake. So my own, self-imposed CLTV is 80%.

Multiplying my home’s assessed value of $300,000 by 80%, I see I have $240,000 in total mortgage borrowing power. If I still owe $200,000 on my first mortgage, I could take out a second mortgage for $40,000 and still have a 20% ownership stake.

Cash-out refinancing is another option

Another way to tap the equity in your home is to refinance your existing mortgage, taking some cash out in the process.

With cash-out mortgage refinancing, you don’t need to take out a second mortgage. Instead, you pay off your existing mortgage with a new mortgage that’s big enough so that there’s money left over. You can then use that money for debt consolidation, or stash it in the bank.

Because it’s a first mortgage, a cash-out refinance will typically offer a lower interest rate than a home equity loan or a HELOC. But remember that whatever interest rate you qualify for, it will apply to your entire mortgage balance, and not just the cash you’re taking out of your house.

No matter which method you use to tap into your home equity, it’s a good idea to compare rates and terms that you can qualify for with different lenders, to avoid overpaying.

Get the cash you need and the rate you deserve. Credible makes it easy to compare lenders and prequalify in minutes.

About the author: Matt Carter is an expert on student loans. Analysis pieces he’s contributed to have been featured by CNBC, CNN Money, USA Today, The New York Times, The Wall Street Journal and The Washington Post.