Our goal is to give you the tools and confidence you need to improve your finances. Although we receive compensation from our partner lenders, whom we will always identify, all opinions are our own. Credible Operations, Inc. NMLS # 1681276, is referred to here as "Credible."

Credible Operations, Inc. NMLS# 1681276, “Credible.” Not available in all states. www.nmlsconsumeraccess.org.

This article first appeared on the Credible blog.

Home equity loans allow you to borrow money using the equity in your home as collateral, possibly at a lower interest rate than a personal loan. You’ll get a lump sum loan that you can use for home renovations, paying down debt, or even to finance your child’s college education.

But keep in mind that home equity loans come with their own benefits and drawbacks — so they aren’t right for everyone.

What is a home equity loan?

A home equity loan is a second mortgage. You’re borrowing against the equity in your home, which is the difference between how much your house is currently worth and what you owe on your mortgage (and any other debt secured by your home). This means the lender can foreclose on your property if you can’t pay your loan back.

While this is a risk, tapping into your home’s equity could be a smart way to get access to more credit when you need it as long as you’re able to pay back the loan.

Here’s how it works: With a home equity loan, your house serves as collateral. Because it’s a secured loan, you might qualify for a lower interest rate compared to other forms of credit (like a personal loan).

How does a home equity loan work?

A home equity loan works much like a personal loan in that you’ll receive your funds in one lump sum a few days after closing. Home equity loans are fully amortizing, meaning each payment reduces your principal and interest. Assuming you make every payment, you’ll fully pay off your loan by the end of the term.

Loan terms vary by loan type and lender. The minimum term you’re likely to find is five years, however, some can be as long as 30 years. Home equity loans have fixed repayment terms and fixed interest rates.

Tip: If you sell your home before your home equity loan is fully repaid, you’ll have to pay the balance at closing (or repay your credit line), before ownership is transferred to the buyer.

Home equity loan rates

Home equity loans have fixed interest rates. These rates tend to be higher than rates for other products that let you access your equity, such as home equity lines of credit (HELOCs) and cash-out refinances. Factors that determine the specific rate you pay include:

- Credit score

- Amount of equity

- Debt-to-income ratio

- The loan-to-value ratio

- Lender

- Whether the loan is a first or second lien (home equity loans are commonly a second-lien loan)

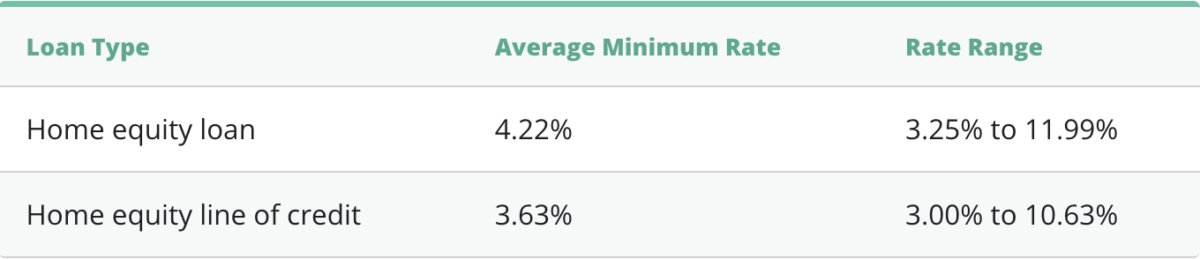

The following table shows the average minimum rate for a home equity loan and HELOC from a sampling of lenders, along with the lowest and highest rates sampled. Your rate may vary. Rates sampled are from February 18, 2022.

Get the cash you need and the rate you deserve on a home equity loan.

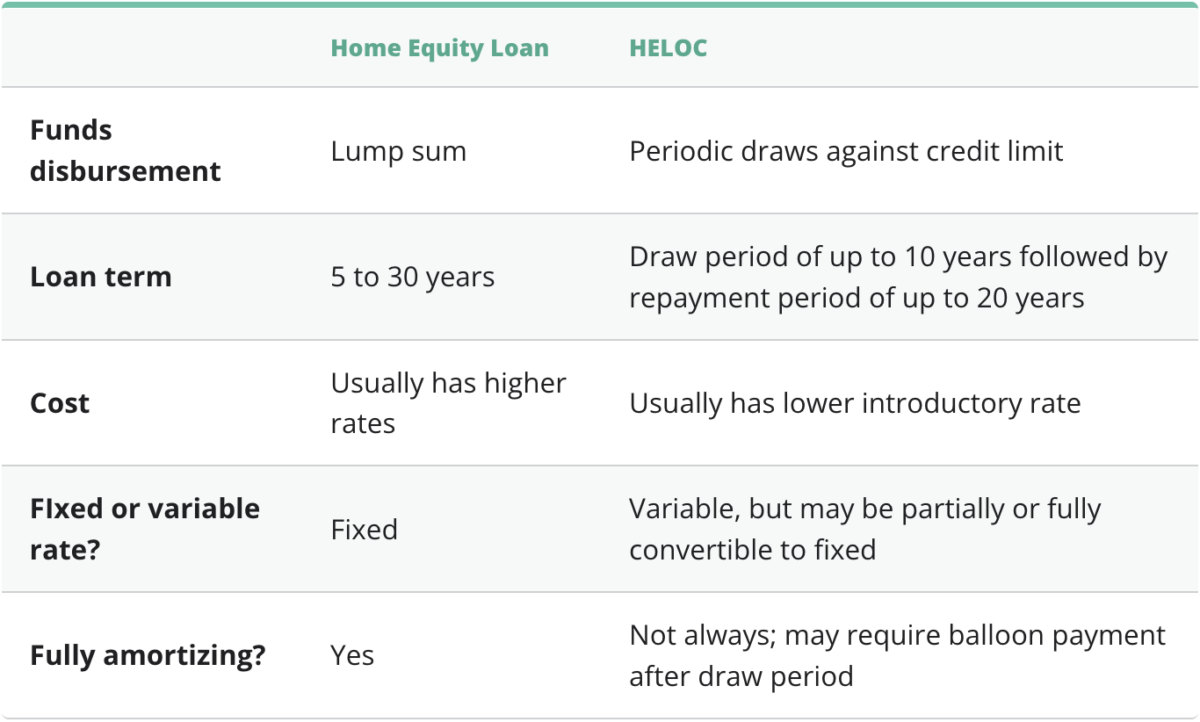

HELOC vs. home equity loan

Technically, home equity loans and HELOCs are two sides of the same coin. The difference is in how the loans are structured and how the money is disbursed.

A home equity loan is an installment loan where you’ll receive a lump sum and repay it in equal monthly payments over a number of years.

With a HELOC, you receive a line of credit that you can borrow from as needed for a fixed period of time (known as the draw period). Once the draw period ends, you’ll enter the repayment period and pay back what you borrowed plus interest. HELOCs often have variable interest rates.

Here’s a closer look at how home equity loans and HELOCs compare:

How much can I borrow with a home equity loan?

The amount you can borrow depends on the amount of equity you have in your home, your credit history, and how much of your monthly income is available to repay a loan.

How do I calculate my home’s equity? To calculate how much equity you have, look up your home’s current market or appraised value, then subtract your current mortgage balance from the amount.

For example, if your home is worth $300,000 and your mortgage balance is $200,000, your home’s equity is $100,000.

You’re generally limited to borrowing 85% of the equity in your home, though other lenders might have stricter limits. So if your equity was $100,000, for example, the maximum you could borrow would be $85,000.

How to qualify for a home equity loan

Getting approved for a home equity loan is similar to going through the process for a new mortgage. Your lender will review your application along with your credit report, credit score, debt-to-income (DTI) ratio, and your home’s equity.

While each lender has its own approval criteria, you’ll typically need the following to qualify for a home equity loan:

- Credit score: You’ll generally need a credit score of at least 680 to qualify for most home equity loans — though, the higher your score, the better your interest rate could be. And although you might get a loan with a score of 660, you could end up with a higher interest rate.

- DTI ratio: Your DTI ratio is the percentage of your monthly income that goes toward debt payments, including your mortgage, student loans, credit cards, and car payment. When applying for a home equity loan, your DTI ratio shouldn’t exceed 43%.

- Equity: To qualify for a home equity loan, you’ll need to have at least 15% to 20% equity in your home. If your house is worth $250,000 and you owe $200,000 on your mortgage, your home’s equity is $50,000, or 20%.

Pros and cons of a home equity loan

If you’re thinking about getting a home equity loan, pay close attention to both the pros and cons that come with using your home as collateral.

Pros

- Fixed repayment terms: Home equity loans typically have fixed repayment terms (usually five to 30 years) as well as fixed monthly payments. This means you’ll know exactly how much you’ll have to pay each month and when your loan will be paid off. You’ll likely have a fixed interest rate, too, meaning your interest rate will never change.

- Low interest rates: Because home equity loans are secured forms of credit, they typically have lower interest rates than you’d get with other loans, such as personal loans.

- No restrictions on how you can use the money: When you take out your loan, the lender will give you a lump sum to use as you wish. You can use your money for whatever you need, from home renovations to a dream vacation.

Cons

- Home as collateral: A home equity loan is secured by your house. If you default on your loan, the lender could foreclose on your home, and you could lose your house.

- Closing costs and fees: A home equity loan can have similar closing costs and fees that you’d expect with a home mortgage (though sometimes they can be waived). You can often roll these added fees into the loan, but they’ll likely add to the overall loan cost.

How to get a home equity loan

If you’ve decided to apply for a home equity loan, follow these steps to find the right loan for you:

1. Determine how much you want to borrow

Think about how much money you need for your desired goals or projects. Having a budget in mind will help you shop around for and compare lenders.

2. Calculate how much home equity you have

To figure out the amount of equity you have in your home, subtract your current mortgage balance from the market value of your home.

For example, say your home’s value has been appraised at $300,000, and you owe $150,000 on your mortgage (and any other debts secured by your house). This means you’d have $150,000 in equity: $300,000 (home value) – $150,000 (mortgage balance) = $150,000 (equity).

3. Figure out how much you can borrow

Most lenders will only let you take out a loan for up to 85% of your home’s equity. If you have $150,000 in equity, that means the maximum you could borrow would be $127,500.

4. Get interest rates from multiple lenders

Be sure to check your rates with multiple lenders to see if you’ll come out ahead by using a home equity loan. This will also help estimate what it will cost to repay your loan, which makes it easier to choose the right loan and lender for your situation.

Costs and fees of home equity loans

It’s important to be prepared for closing costs and fees when taking out a home equity loan. While these will vary from lender to lender (and sometimes can even be waived), they’ll typically be somewhere between 2% to 6% of your loan amount.

For example, on a $100,000 loan, you could expect to pay $2,000 to $6,000 in closing costs and fees.

Some common expenses include:

- Appraisal fees: A home appraisal determines how much your house is worth and affects your home’s equity. A typical appraisal fee is $300 to $400.

- Origination fees: An origination fee is what some lenders will charge to issue you a loan. These can range from $0 (with lenders that don’t charge an origination fee) to $125.

- Preparation fees: Some lenders will charge you for preparing your loan documents, which might include hiring lawyers and notaries. Preparation fees can range anywhere from $100 to $400.

- Credit report fees: Lenders will run a credit check to get your credit score. The fee is usually about $25.

- Title search fees: The lender will do a title search to ensure you own the home and search for liens and other issues with title. The title search fee is usually $75 to $100.

Alternatives to home equity loans

If a home equity loan isn’t quite right for you, here are a few other forms of credit that might be a better financing option:

- Cash-out refinance: If you have more equity in your home than you owe on the mortgage, a cash-out refinance might be a good choice. With this option, you’ll take out a new mortgage that’s big enough to pay off your old mortgage and leave you with left-over cash to use however you’d like.

- Personal loan: If you have a short-term financial need, you might be able to take out an unsecured personal loan. Getting an unsecured loan means you won’t have to use your property as collateral.

Credible makes getting a mortgage refinance easy.

About the author: Daria Uhlig is a contributor to Credible who covers mortgage and real estate. Her work has appeared in publications like The Motley Fool, USA Today, MSN Money, CNBC, and Yahoo! Finance.