Our goal is to give you the tools and confidence you need to improve your finances. Although we receive compensation from our partner lenders, whom we will always identify, all opinions are our own. Credible Operations, Inc. NMLS # 1681276, is referred to here as "Credible."

Content provided by Credible. Although we do promote products from our partner lenders who compensate us for our services, all opinions are our own.

This article first appeared on the Credible blog.

When you’re in school, it can be easy to rack up student loan debt without realizing how bad the situation really is.

The number of borrowers who have six figures’ worth of student loan debt (far more than the average student loan debt) is on the rise. For example, as of 2021, about 900,000 federal student loan borrowers owed $200,000 or more in federal student loans, according to StudentAid.gov.

The good news is that while paying off such a large balance can be difficult, it’s not impossible.

Here’s how to pay off $200,000 in student loans.

1. Refinance your loans

Best for:

- Borrowers with high monthly payments

- Borrowers with good to excellent credit

- Borrowers with a creditworthy cosigner

- Borrowers with large private student loans

If you have high-interest student loans, going through the student loan refinance process makes a lot of sense. When you refinance, you work with a private lender to take out a new loan for the amount of your old ones, paying those off and getting a new loan with a new interest rate.

The new loan typically has different terms, including interest rate and length of repayment. You can refinance medical school loans, refinance law school loans, and more.

If you have good credit, you could qualify for a loan with a lower interest rate, helping you save money over the length of your loan. Or you can extend your repayment term to get a lower monthly payment that you can afford.

Just know that a longer term typically means you’ll pay more in interest over the life of the loan.

Keep in mind: While you can refinance federal student loans, you’ll lose your federal benefits and protections, including access to income-driven repayment plans and student loan forgiveness programs.

If you decide to refinance your student loans, be sure to consider as many lenders as possible to find the right loan for your situation.

This is easy with Credible. You can compare your prequalified rates from Credible partner lenders in two minutes.

2. Add a cosigner to improve your interest rate

Best for:

- Borrowers with poor or fair credit

- Borrowers who know someone willing to cosign their loan

You’ll typically need good to excellent credit to qualify for refinancing — a good credit score is usually considered to be 700 or higher. There are also several lenders that offer refinancing for bad credit, but these loans typically come with higher interest rates compared to good credit loans.

If you have less-than-perfect credit and are struggling to get approved, consider applying with a creditworthy cosigner to improve your chances. Even if you don’t need a cosigner to qualify, having one might get you a lower interest rate than you’d get on your own.

Tip: A cosigner can be anyone with good credit — such as a parent, another relative, or a trusted friend — who is willing to share responsibility for the loan. Just keep in mind that if you can’t make your payments, your cosigner will be on the hook.

If applying with a cosigner helps you get a better interest rate, you could save money on interest charges over the life of your loan. You can use a calculator to see how much you can save by refinancing your student loans. If you decide refinancing is right for you, Credible makes it easy to compare student loan refinance rates from multiple lenders.

3. Sign up for an income-driven repayment plan

Best for:

- Borrowers with high monthly payments in relation to their income

- Borrowers with high federal student loan balances

If you can’t afford your current monthly payments and you have federal student loans, consider signing up for an income-driven repayment (IDR) plan.

Under an IDR plan, your loan servicer extends your repayment term to 20 to 25 years and sets your monthly payment at a percentage of your discretionary income. Some borrowers even qualify for $0 payments.

After 20 to 25 years of making payments, your remaining balance is forgiven. The discharged amount is taxable as income, but this approach can still give you substantial relief.

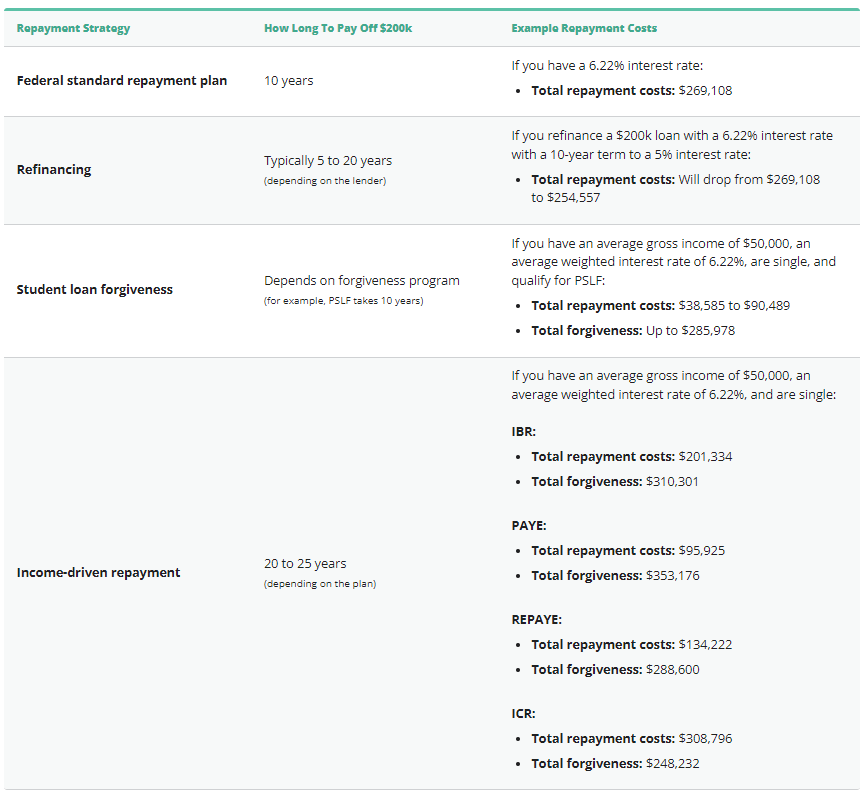

Here’s how the four main IDR plans compare to a few other federal repayment plan options:

4. Pursue student loan forgiveness

Best for:

- Employees of government or nonprofit organizations

- Borrowers with high federal student loan balances

- Borrowers with high monthly payments in relation to their income

There are several student loan forgiveness programs available if you have federal student loans. Most require you to have a certain type of employment and to make eligible payments for a set amount of time.

For example: If you have federal student loans and work for a qualifying nonprofit organization or a government agency, you might qualify for Public Service Loan Forgiveness (PSLF). Under this program, you get loan forgiveness if you work for 10 years at a qualifying organization and make 120 monthly payments. The remaining balance is discharged tax-free, so the savings can be significant.

Some common careers that might qualify for student loan forgiveness include:

- Government employees

- Nonprofit employees

- Teachers

- Doctors

- Nurses

- Lawyers

- AmeriCorps or Peace Corps volunteers

Keep in mind: Unfortunately, private student loan forgiveness doesn’t exist. But if you have private student loans, there are other options available that might help you pay your loans off more easily, such as refinancing for a lower interest rate.

5. Use the debt avalanche or debt snowball method

Best for:

- Borrowers who can afford a larger monthly payment

- Borrowers who want to get out of debt quickly

In some cases, you might need to simply concentrate on paying off your loans as quickly as possible — such as if you have multiple loans and can’t qualify for forgiveness. Here are a couple of strategies that could help:

Debt avalanche method

With the debt avalanche method, you’ll focus on paying off your loan with the highest interest rate first while making the minimum payments on your other loans.

After this loan is paid off, move on to the loan with the next-highest interest rate — continuing until all of your loans are repaid.

Tip: Although the debt avalanche method can save you money, it can be a slow process. If you’re motivated more by small wins, you might consider the debt snowball method instead.

Debt snowball method

With the debt snowball method, you’ll focus on repaying your smallest loan first while making the minimum payments on your other loans.

Once the smallest loan is repaid, move on to the next-smallest loan — continuing until all of your loans are paid off.

Tip: The debt snowball method is usually a faster option. But if you’d rather save more money on interest and don’t mind waiting to see your results, you might consider the debt avalanche method instead.

If you’re wondering how long it’ll take to pay off your student loans, you can use a student loan calculator.

How long will it take to pay off $200k?

This will depend on how you approach your repayment. For example, paying off a refinanced loan might take a shorter time than pursuing forgiveness through an IDR plan.

Here’s how long you can expect the various repayment strategies to take as well as some examples of the associated costs:

Does student loan debt go away?

Sadly, there’s no magic trick to make your student loan debt simply go away. But one of the options above could help you tackle your loans once and for all — or even have them forgiven.

There are also some circumstances where your federal student loans might be discharged, such as if:

- You’re totally and permanently disabled

- Your school closed while you were enrolled

- You have Perkins Loans and have served for a certain amount of time in an eligible career

Don’t be discouraged: There are 43 million student loan borrowers in the U.S. The average student loan debt is $33,654, but 2.8 million borrowers owe 100,000 or more. So if you have a high student loan balance, don’t worry — you’re definitely not alone.

If you decide to refinance your student loans, be sure to consider as many lenders as possible to find the right loan for you. Credible makes this easy — you can compare your prequalified rates from multiple lenders in two minutes.

About the author: Eric Rosenberg is a finance, travel, and technology writer in Ventura, California. His work has been featured at Business Insider, Investopedia, The Balance, The Huffington Post, MSN Money, Yahoo Finance, Mint.com, and many other fine outlets.