Our goal is to give you the tools and confidence you need to improve your finances. Although we receive compensation from our partner lenders, whom we will always identify, all opinions are our own. Credible Operations, Inc. NMLS # 1681276, is referred to here as "Credible."

Content provided by Credible. Although we do promote products from our partner lenders who compensate us for our services, all opinions are our own.

This article first appeared on the Credible blog.

Student loans cover more than just tuition, fees, and books for school. You can also use them for other college-related costs — including living expenses.

Here’s what’s you should know about student loans for living expenses.

If you’re looking for a private student loan, you can use Credible to get started. With Credible, you can easily compare rates from multiple lenders, without affecting your credit.

How to use student loans for living expenses

If you need to cover your living expenses while attending college, it’s a good idea to start by filling out the Free Application for Federal Student Aid (FAFSA). Your school will use your FAFSA results to determine what federal student loans and other federal financial aid you qualify for.

Also be sure to take advantage of any college scholarships and grants — since unlike student loans, these don’t have to be repaid. There’s no limit to how many of these you can get, so apply for as many as you might be eligible for.

Tip: Keep in mind that it’s usually best to take out federal student loans first if you have to borrow for college. This is mainly because these loans come with federal benefits and protections, such as access to income-driven repayment plans and student loan forgiveness programs.

After you’ve exhausted your scholarship, grant, and federal student loan options, private student loans can help fill any financial gaps left over. If you decide to take out a private student loan, be sure to consider as many lenders as possible to find the right loan for your needs.

How student loans work for living expenses

Undergraduate, graduate, and professional students are all able to use student loans for living expenses. Student loan funds are typically disbursed directly to your school to cover tuition and fees. Any money left over will be refunded to you, which you can use to pay for housing and any other education-related costs.

Keep in mind that both federal and private student loans have their own student loan requirements. To qualify for federal student loans, you must have financial need and be enrolled at least half time at an eligible school. With private student loans, you’ll typically need good credit and verifiable income to qualify — though exact requirements can vary by lender.

Tip: Some private lenders offer student loans for bad credit — but these loans tend to come with higher interest rates compared to good credit loans. If you’re struggling to get approved for a private student loan, consider applying with a cosigner to improve your chances. Even if you don’t need a cosigner to qualify, having one could get you a lower interest rate than you’d get on your own.

What can student loans be used for?

- Tuition

- Fees

- Room and board

- Housing utilities

- Housing supplies and furnishings

- Meals and groceries

- Books

- Equipment

- Supplies

- A personal computer you’ll use for school

- Transportation costs

- Dependant childcare expenses

- Miscellaneous personal expenses

Before you take out a federal or private student loan to help cover these costs, it’s important to consider how much that loan will cost you in the future. This way, you can be prepared for any added expenses.

You can find out how much you’ll owe over the life of your federal or private student loans by using Credible’s student loan calculator. And if you’re ready to begin comparison shopping for a student loan, you can get started with Credible. It’s 100% free to compare rates from multiple lenders in minutes.

What shouldn’t student loans be used for?

While student loans can help cover quite a few expenses, keep in mind that you’ll have to pay back whatever you borrow. Because of this, it’s important to borrow only what you need so you can keep your future repayment costs as low as possible.

For example, some expenses you shouldn’t use your student loans for include:

- Vacations and travel

- A new vehicle

- Down payment on a house

- Entertainment

- Dining out often or expensive meals

- A new wardrobe

- Small business expenses

- Your other debt

- Anyone else’s expenses (like paying for a friend’s tuition)

What happens if you use student loans for something you shouldn’t?

Financial aid offices don’t track exactly how students use their funds, so it’s unlikely that you’ll get in trouble for using your financial aid or student loans in cases where you shouldn’t. But if you spend more money than what’s budgeted in your school’s official cost of attendance, you could end up with fewer funds than you need to pay for other expenses — such as college textbooks or fees.

Additionally, if your financial aid office finds out that you’ve spent funds inappropriately, you could:

- Be reported to the Department of Education

- Have your funds taken back retroactively

- Be responsible for paying back what you’ve already used to the school

There’s also a slim possibility that you could be investigated and prosecuted for abusing student loan funds if your financial aid office finds out — so be sure to spend your funds appropriately.

Tip: Before you spend extra financial aid or student loan money, ask yourself whether the expense you’re considering is something that you need for your education — such as college housing or textbooks. If it isn’t, it’s best not to use the funds. If you’re worried that you’ve already used some of your funds in the wrong way, chalk it up as a lesson for how not to spend funds in the future. You could also consider saving money from a job or other income source to replace those funds.

Alternatives to using loans for living expenses

While student loans are one way to pay for living expenses, they aren’t your only option. Here are a couple of other alternatives to consider:

- Apply for scholarships and grants: Because college scholarships and grants don’t have to be repaid, they can help keep your costs low while paying for living expenses. You might qualify for federal grants or school-based scholarships after filling out the FAFSA. There are also many private scholarships and grants available from nonprofit organizations, local and national businesses, and professional associations in your field.

- Get a job. Working a part-time job during college can help you earn extra money for living expenses while also building your resume. You could also consider applying for a job through a work-study program.

Other ways to potentially lower your costs overall include:

- Buying used textbooks or renting them

- Living off-campus and getting a roommate (or living at home if possible)

- Carpooling with a friend that has a similar schedule to you

What to do with leftover student loan money

It’s best to borrow only what you need to pay for school and related costs so you can avoid excessive student loan payments in the future. But if you end up with extra federal or private student loan funds, there are a couple of ways to handle it:

- Pay it back. If you don’t need all of your student loan money, you could pay it back to lower your overall loan balance. With federal student loans, you can cancel some or all of your disbursement within 120 days and return the money to your school.

- Save it for necessary expenses. If you have fluctuating or limited income, you might have a hard time getting the money you need for rent or other necessities each month. Saving your extra loan funds for upcoming payments or expenses can give you something to fall back on in case your other income doesn’t come through. If you don’t end up using the money, you can always pay it back toward your loans later.

Just remember that you’ll have to pay back whatever you borrow — so be sure to only keep your extra funds if you need to.

Frequently asked questions

Here are the answers to several commonly asked questions regarding student loans for living expenses:

How can I live off student loans?

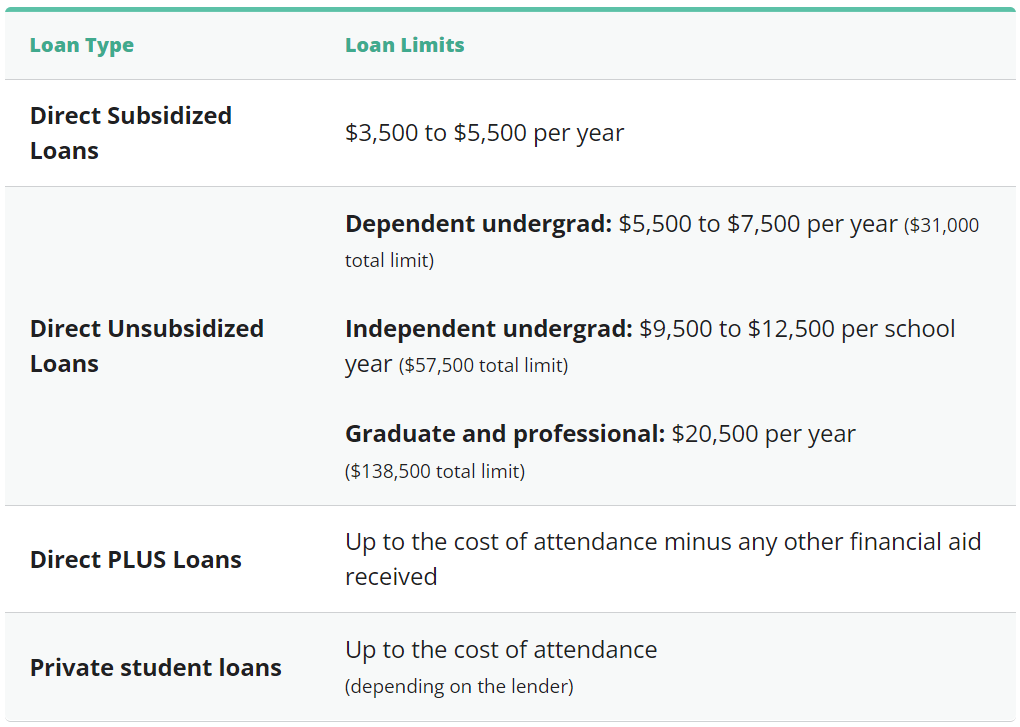

You can use student loans for almost any education-related expense — meaning you can potentially live on them. However, keep in mind that some loans come with student loan limits that will determine how much you can borrow.

Here are the undergraduate and graduate student loan limits you can expect:

How do I get financial aid for living expenses?

To get financial aid for living expenses, you’ll need to complete the FAFSA. How much you’ll receive in financial aid will depend on several factors, including your school’s cost of attendance, your year in school, and whether you’re an independent or dependent student.

If you’re a dependent student, it will also be affected by your Expected Family Contribution (EFC) — which is how much your family is expected to contribute toward your education.

How should students pay for monthly expenses?

There are several ways you can pay for monthly costs as a student. For example, any extra financial aid or student loan money after your tuition is paid for will be refunded to you. You can then use these funds to pay for rent or other monthly expenses.

Do student loans go to your bank account?

This depends on how you’ve set up your student account at your school. If you’ve provided bank account information, you’ll typically receive any leftover student loan money as a direct deposit.

In other cases, your school might send you a check or deposit your funds on a prepaid debit card — however, these options could take longer compared to a bank deposit.

Can I use my student loan to buy a car?

Generally no — buying a car doesn’t fall under necessary education expenses, so you can’t use a student loan for it. However, you could use a student loan to help pay for gas or other transportation expenses.

Can I use my student loan to pay off credit cards?

If you’ve covered education expenses with a credit card while waiting for your student loan funds, you could pay off your card with those once you’ve received them. But in other cases, it could be considered an improper use of your student loan funds to pay off credit card debt.

Keep in mind: Using your student loan to pay off other debt could lead you to need more student loans in the future — meaning you could end up with more debt than what you started with.

If you decide to take out a private student loan for living expenses, remember to consider as many lenders as you can to find the right loan for you. This is easy with Credible: You can compare your prequalified rates from multiple lenders in two minutes — without affecting your credit.

About the authors: Dori Zinn is a student loan authority and a contributor to Credible. Her work has appeared in Huffington Post, Bankate, Inc, Quartz, and more. Jamie Young contributed to the reporting for this article.