Our goal is to give you the tools and confidence you need to improve your finances. Although we receive compensation from our partner lenders, whom we will always identify, all opinions are our own. Credible Operations, Inc. NMLS # 1681276, is referred to here as "Credible."

Credible Operations, Inc. NMLS# 1681276, “Credible.” Not available in all states. www.nmlsconsumeraccess.org.

This article first appeared on the Credible blog.

A home loan can be the biggest debt you’ll ever have, so knowing how to refinance your mortgage is important in helping you meet your long-term financial goals. And whether you’re refinancing your mortgage to get a lower rate, or cashing out some home equity, it can be a much simpler process than when you first bought your home.

Credible makes it easy to compare mortgage refinance rates from multiple lenders in minutes. It’s 100% free to use and checking your rates won’t affect your credit.

Here’s how to refinance your mortgage in just six steps:

Step 1: Set a goal

Your approach to mortgage refinancing will depend on whether you’re most interested in getting a better rate, lowering your monthly payment, or tapping into your home’s equity. So, decide what your goal is first:

- I want a lower interest rate. The interest rate you can qualify for when refinancing a mortgage will depend on market interest rates, your credit score, and how long you want to take to repay your loan.

- I want a lower monthly payment. If you need some more room in your monthly budget, you might want to refinance to get a lower payment. One way to do this is to extend your repayment term. But keep in mind, this could cause you to pay more in interest over the life of your loan.

- I need to pay for home improvements or other big expenses. If you plan on making some home improvements, tapping into your home equity can be a smart way to finance it.

Step 2: Review your credit, DTI, and income

Before moving on, make sure your financial health is in order. Three major factors are involved in getting approved for a mortgage:

- Credit score: Get copies of your credit history from all three credit agencies through AnnualCreditReport.com and make sure there are no outstanding issues or mistakes. Anything you can do to improve your credit score can help you get a better rate.

- Debt-to-income ratio: Depending on your loan type, your maximum debt-to-income ratio for mortgage should be anywhere between 31% and 45%. The formula to calculate your DTI is: (Total monthly debt) / (Gross monthly income) x 100 = DTI. For example, if your total monthly debt payments are $2,300 and you earn $6,000, then your DTI is 38%.

- Income: Ensure your income is steady and stable before taking the next step to refinancing.

Step 3: Find out how much equity you have in your home

If you want to make some home improvements, using your home equity can be a good idea. Or if you need to pay for other larger expenses, you can use your home equity to get cash through a cash-out mortgage refinance.

To calculate how much equity you have, research your home’s value, then subtract your mortgage balance from the amount. For example, if your home is worth $300,000 and your mortgage balance is $200,000, your home’s equity is $100,000.

Tip: You’re generally limited to borrowing 80% of the equity in your home, though other lenders might have stricter limits. So if your equity was $100,000, for example, the maximum you could borrow would be $80,000.

Step 4: Compare lenders’ rates and fees

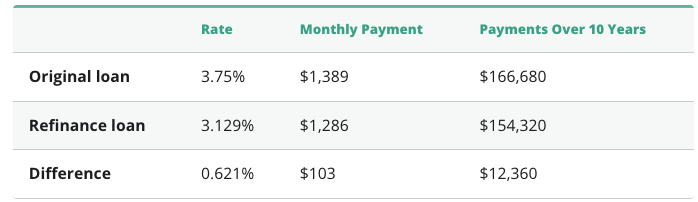

Because mortgage loans are so big, even small differences in interest rates can add up to thousands of dollars in savings. So it’s a good idea to compare lenders for the lowest rate.

Here’s an example of how much you could save by refinancing a $300,000 balance with another 30-year repayment term but at a lower rate:

Most experts agree that you should only refinance a loan when interest rates are 0.5% to 1% lower than your current interest rate. Consider applying for a 15-year refinance loan if you want an even lower interest rate and can afford the higher monthly payment. This shorter term also reduces your lifetime interest costs.

Refinance rates don’t tell the whole story either. Make sure you understand what fees you’ll pay with each of your options.

Credible lets you see your prequalified mortgage refinance rates in minutes, without affecting your credit.

Step 5: Get a loan estimate

Once you’ve compared real rates and fees from multiple lenders, you can get a loan estimate from the lender you’re seriously considering. The loan estimate is a standardized form that makes it easier to compare your options.

You’ll have to apply for a mortgage to get a loan estimate, which involves a hard credit check. But keep in mind: Rate shopping allows you to apply for the same type of loan multiple times within a certain time frame, and it will only hit your credit score as a hard inquiry once.

Step 6: Prepare your documents and apply

After you’ve compared multiple lenders and loan estimates, choose the option that’s the best fit for your goals. The lender you choose will want some basic documentation from you as well, to verify your income and assets.

You can generally expect to provide things like:

- Tax returns

- W-2s

- Pay stubs

- Bank, savings, and retirement account statements

- Details on any assets or investments

- A copy of your driver’s license

Credible makes it easy to compare mortgage refinance rates from various lenders, all in one place.

Frequently asked questions

What is mortgage refinancing?

With mortgage refinancing, you’re taking out a new mortgage to replace your current one. Essentially, your old mortgage is paid off and you’ll start making payments on the new home loan instead. This can help you get a lower interest rate or lower monthly payment, depending on your goals.

What are the benefits of refinancing a mortgage?

Mortgage refinancing has six main benefits, and in many cases, you can benefit from more than one:

- Lower interest rate: The interest rate you can qualify for when refinancing a mortgage will depend on market interest rates, your credit score, and how long you want to take to repay your loan.

- Lower monthly payment: If you’re able to refinance into a mortgage with a lower interest rate, that’ll often lower your monthly payment too. But another way to lower your monthly payment is by extending your repayment term.

- Fixed interest rate: If you’ve got an adjustable-rate mortgage (ARM), your interest rate and monthly payment can go up and down as the economy heats up or cools down. When rates are headed up, refinancing from an ARM to a fixed-rate mortgage protects you from uncertainty.

- Tap home equity for home improvements or other big-ticket items: When you’re ready to make home improvements, your home equity can be an affordable source of financing. Or if you have other big-ticket expenses, like paying for a child’s college education, you can convert some of your home equity into cash through a cash-out mortgage refinance.

- Pay off high-interest debt: Because you’re putting your home up as collateral, interest rates on a cash-out mortgage refinance can be hard to beat. Many homeowners tap their home equity to pay off student loans or high-interest credit card debt.

- Cancel your mortgage insurance: If you have at least 20% equity in your home, but are still paying costly FHA mortgage insurance premiums, now could be a good time to refinance into a conventional (non-FHA) loan.

What are the risks of refinancing a mortgage?

Before refinancing your mortgage, here are some risks to be aware of:

- The cost to refinance: Sometimes fees and other costs of refinancing can outweigh the savings. There are many origination charges to consider, such as loan-discount points, application fees, and underwriting fees; as well as third-party fees like title insurance, appraisals, and pest inspections.

- Home equity is a safety cushion: If you tap your home’s equity, you may have less room to maneuver if you experience financial hardship like unemployment. Home prices are unpredictable, and pulling too much cash out of a home can put homeowners at higher risk of foreclosure in a downturn.

- Might give up some tax benefits: If you took out a mortgage to buy or improve a home before Dec. 16, 2017, the interest you pay on up to $1 million in debt may be tax deductible. Now, you can only deduct the interest paid on up to $750,000. That means if you refinance an older $1 million mortgage, you’ll be subject to the lower $750,000 cap.

If you have questions about your specific situation, remember to consult with a tax professional or financial advisor.

How does refinancing work?

Refinancing replaces your existing mortgage with a new mortgage. After you refinance, you’ll receive a different monthly payment, interest rate, and repayment term. Most homeowners refinance their mortgage to secure a lower interest rate and smaller monthly payment, which can unlock more cash for other financial goals.

After you’ve applied for the refinance and locked in your rate, you’ll enter the underwriting process. This may include a home appraisal to estimate your property value and equity.

Tip: There’s generally no waiting period for refinancing a conventional loan — you can refinance immediately after closing on your original loan if you want. If your lender sets a waiting period, you can always get around this by shopping with another lender. Cash-out refinances, however, typically require a waiting period of at least six months.

Once the underwriters approve your application, you’ll begin the closing process and pay your closing costs. You may be able to roll some or all of these costs into your new mortgage. The final step is to start sending your payment to the new lender after signing the closing papers. Your new monthly payment now reflects your refinance rate and term.

When should I refinance my mortgage?

The reasons why you should refinance depend on your situation and your goals. If you’re most interested in lowering the interest rate on your mortgage, here are a few situations when it’s a good time to refinance:

- Interest rates are falling: Mortgage rates rise and fall when economic conditions change. If you took out your current mortgage when interest rates were higher than they are today, you could save thousands by refinancing.

- Your credit score improved: To get the best mortgage interest rates, you’ll want excellent credit. If your credit score has increased since taking out your current mortgage, you might be able to refinance at a lower rate.

- You can afford to switch to a 15-year mortgage: Most people take out a 30-year mortgage when they buy a home because it makes their monthly payments more affordable. But interest rates on 15-year mortgages can be considerably lower.

If you’re more interested in tapping your home’s equity, the best time to refinance your mortgage is when:

- Home prices are rising: Rising home prices can give homeowners a bigger equity stake in their homes. Your equity is equal to your home’s current value, minus what you still owe on the mortgage.

- You’ve paid down your mortgage balance: Even if your home hasn’t increased in value, if you’ve paid down some mortgage principal, you may have some equity that you can tap through a cash-out refinance.

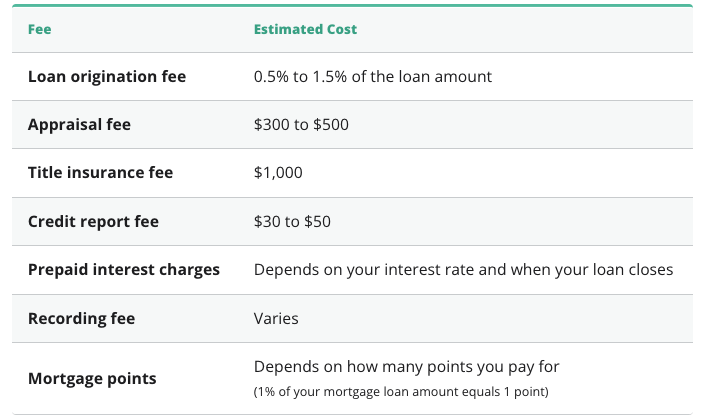

How much does refinancing cost?

The cost of refinancing your mortgage can vary from lender to lender. But closing costs for a refinance are generally between 2% and 5% of the total loan amount.

Here are some of the most common refinancing fees that you might encounter:

Should I refinance into another 30-year fixed loan?

If you’re thinking about refinancing into another 30-year loan, consider some of the pros and cons:

Pros

- Your monthly payments will likely be lower. If your payments are spread out over a longer period of time, your monthly payment won’t be as high. This gives you more flexibility in your budget.

- You have the option to pay your loan off in 30 years or less. Although you can take advantage of the lower payments for as long as you want, you can also choose to put more money toward your balance and pay your loan off sooner than 30 years.

Cons

- You’ll pay more in interest. Because you’ll be making more payments over a longer period of time, you’ll end up paying more in interest over the life of your loan, which would make it costlier overall.

- Your interest rate might be higher. Interest rates on 30-year mortgages are typically higher than those on shorter terms, like a 15-year mortgage.

How to get the best mortgage refinancing rate

Because every mortgage lender has its own methods for evaluating borrowers, getting the best mortgage rate requires that you do a little shopping around — which sometimes can be quite the chore. Be sure to get loan estimates from multiple lenders. Compare the rates, fees, and other loan costs.

Luckily, Credible does a lot of the legwork for you, so you don’t have to feel lost or overwhelmed. You can see your prequalified mortgage refinance rates from multiple mortgage lenders without affecting your credit score.

About the author: Jamie Young is an authority on personal finance. Her work has been featured by Time, Business Insider, Huffington Post, Forbes, CBS News, and more.