Our goal is to give you the tools and confidence you need to improve your finances. Although we receive compensation from our partner lenders, whom we will always identify, all opinions are our own. Credible Operations, Inc. NMLS # 1681276, is referred to here as "Credible."

Content provided by Credible. Although we do promote products from our partner lenders who compensate us for our services, all opinions are our own.

This article first appeared on the Credible blog.

The interest rate on a loan is a percentage of the loan principal that a lender charges as part of your overall loan cost — essentially, it’s a fee you pay to borrow money.

When you take out a student loan, you might have a choice between:

- A fixed interest rate, which will stay the same throughout the life of the loan

- A variable interest rate, which can fluctuate depending on the market conditions

An important step in deciding between a fixed or variable rate student loan is to compare how each type of rate will affect your loan costs. Credible makes it easy to compare private student loan rates from multiple lenders.

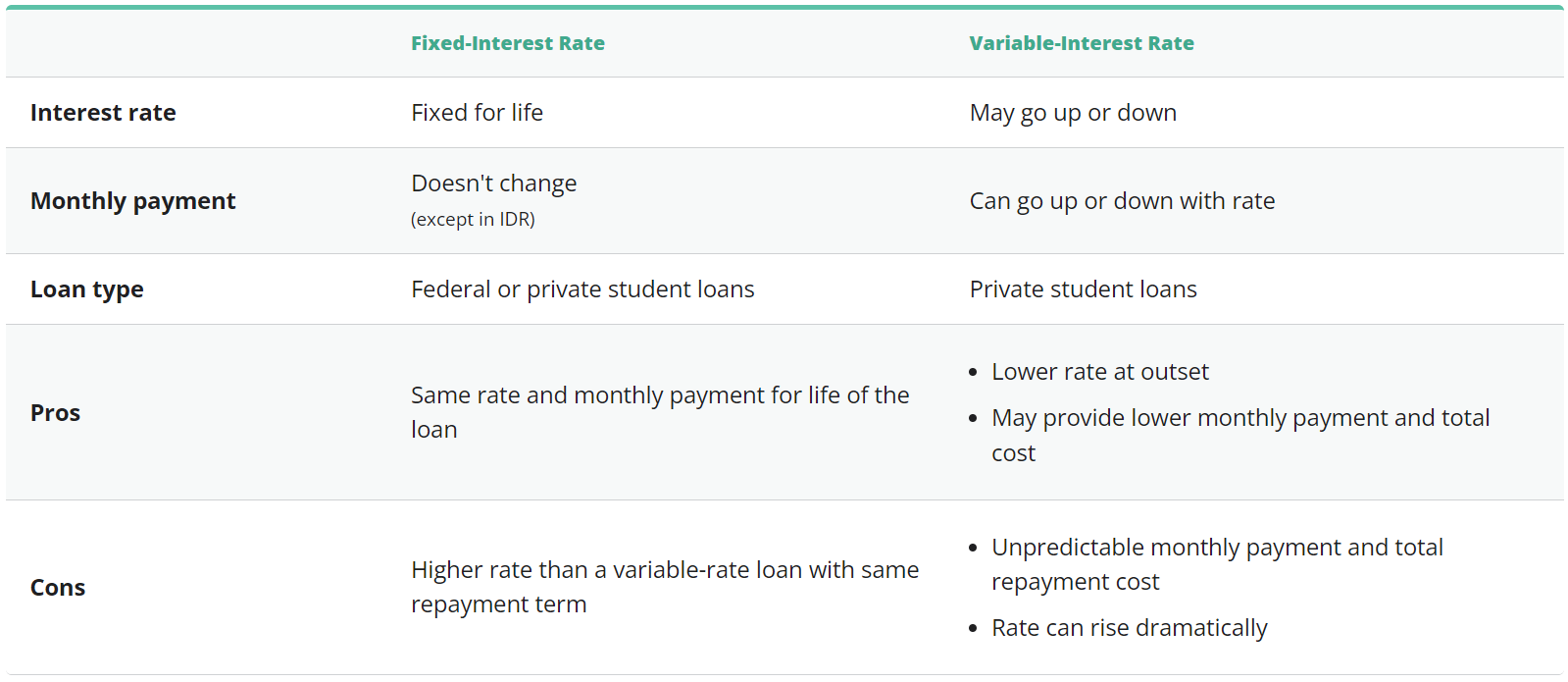

Fixed vs. variable student loan interest rates

If you’re comparing a fixed vs. variable interest rate on a student loan, it’s important to consider your overall repayment strategy to choose the most optimal rate for your needs. Here are a few important points about both rate types to keep in mind:

No matter if you choose a fixed- or variable-rate student loan, it’s important to shop around and compare as many lenders as possible. This way, you can find the right loan for your needs.

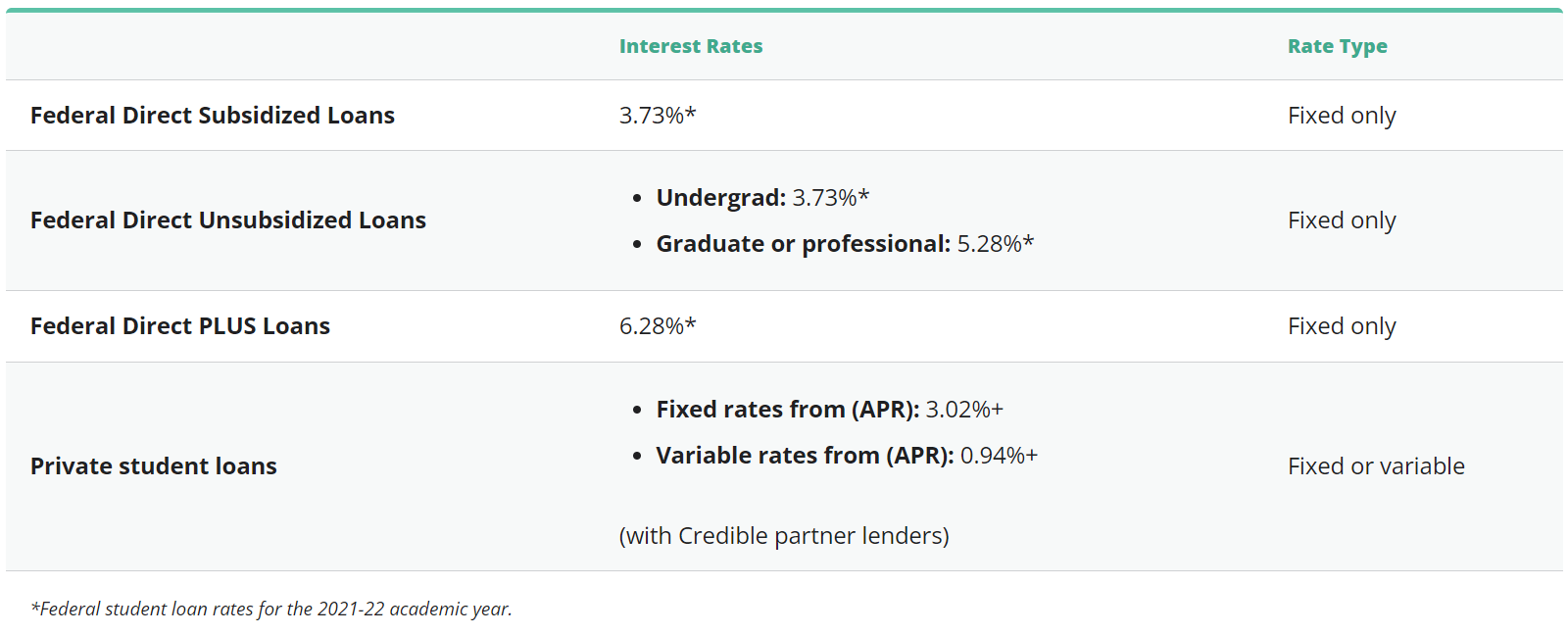

Interest rates for federal and private student loans

Here are the interest rates you can generally expect for federal and private student loans:

When to choose a fixed-rate student loan

In some cases, a fixed-rate student loan could be the right option for your finances. Here are a few reasons why you might choose a fixed interest rate:

- Predictable monthly payment: With a fixed interest rate, your monthly payment will stay the same throughout the life of the loan.

- Fixed repayment cost: Because a fixed interest rate won’t ever change, you’ll know exactly how much the loan will cost you.

- Could be less expensive for longer repayment periods: If you expect to repay your loan over several years, a fixed interest rate will likely be less expensive than a variable interest rate that could fluctuate over time.

When you might not want a fixed-rate student loan

While the predictability of fixed-rate student loans is appealing for many borrowers, there are also some potential drawbacks to keep in mind:

- Higher initial interest rate: Fixed interest rates generally start off higher compared to variable rates for the same repayment term, which means your payments will be more.

- Rate won’t ever drop: Unlike a variable rate that could shift over time, a fixed rate will stay the same throughout the life of the loan. This means a fixed interest rate won’t drop if market rates decrease.

- Higher loan cost for shorter repayment terms: If you plan to pay off your loan quickly, you could end up paying more on a fixed-rate loan compared to a variable-rate loan.

Comparing student loan interest rates is easy when you use Credible. It’s 100% free to check your rates and doing so won’t affect your credit score.

When to choose a variable-rate student loan

There are also some situations where a variable-rate student loan might be the best choice for your needs. Here are a few benefits of variable rates to consider:

- Lower initial interest rate: Variable rates generally start off lower than fixed interest rates, which could be especially helpful if you plan to pay off your loan quickly before the rate can change too much.

- Lower initial payments: Because variable rates are usually lower than fixed rates to start, your initial payments will start off lower in comparison. This might be appealing if you expect your income to rise over time.

- Potential for interest rate drops: Depending on market conditions, a variable rate might drop in the future. This also means your monthly payments will be reduced.

When you might not want a variable-rate student loan

Although a variable rate might be appealing in some cases, here are a few drawbacks to think about:

- Interest rate could change: A variable rate can rise or fall along with market conditions. This could make it difficult to estimate your overall repayment cost.

- Unpredictable payments: Any changes in your variable rate will also mean shifts in your monthly payments.

- Potentially more expensive overall: Depending on how quickly you pay off your student loan, you might find yourself paying much more over time with a variable rate compared to a fixed rate.

Keep in mind: Depending on the lender, a variable-rate student loan could come with an interest rate cap, which is the highest variable rate allowed by the lender. Your rate will never increase past this amount. This can help keep your interest costs lower as well as offer some peace of mind. However, you might still end up paying more in interest with a capped variable-rate loan than you would with a fixed-rate loan — especially if you can’t pay off your loan before your rate has a chance to change.

Student loan refinancing: Better to get a fixed or variable rate?

Student loan refinancing is the process of paying off your old loans with a new private student loan, leaving you with just one loan and payment to manage.

If you choose to refinance your student loans, you’ll also typically have a choice between a fixed or variable rate — this means you can switch the kind of rate you currently have.

Keep in mind: Your financial needs as a graduate will likely have changed from when you were first attending school — so it’s important to carefully consider again which kind of rate will be best for your situation.

Pros and cons of a fixed-rate refinanced loan

While a fixed-rate refinanced loan could be a good choice for some borrowers, it isn’t right for everyone. Here are some pros and cons to keep in mind as you consider your options:

Pros and cons of a variable-rate refinanced loan

Like fixed-rate loans, variable-rate loans also come with their own pros and cons when it comes to refinancing, such as:

How do student loan interest rates work?

Your interest rate is the main factor that will determine how much you’ll pay for a student loan over time. Here’s how student loan interest rates work for federal and private student loans:

Federal student loan interest rates

All federal student loans have fixed rates that will stay the same throughout the life of the loan. Federal rates are set by Congress and are updated each year. The rate you get on a federal student loan will depend on the type of loan you choose as well as your year in school.

Tip: If you need to borrow money to pay for college, it’s usually a good idea to start with federal student loans. This is mainly because these loans come with federal benefits and protections — such as access to income-driven repayment plans and student loan forgiveness programs. Additionally, most federal student loans don’t require a cosigner or a credit check.

Here are the rates you can expect for the 2021-22 academic year as well as how rates have changed over time:

- Direct Subsidized Loans: 3.73%

- Direct Unsubsidized Loans (for undergraduate students): 3.73%

- Direct Unsubsidized Loans (for graduate and professional students): 5.28%

- Direct PLUS Loans (for graduate students and parents): 6.28%

Private student loan interest rates

The interest rates on private student loans are set by individual lenders based on market conditions. Many private lenders offer both fixed- and variable-rate student loans.

Keep in mind: The rates you’re offered on private student loans will mainly depend on your credit. Typically, you need good to excellent credit to qualify for a private student loan as well as to get the most favorable rates. In general, the better your credit score, the lower your rate will be. There are also some lenders that offer private student loans for bad credit. However, these loans usually come with higher interest rates compared to good credit loans.

You can check your prequalified rates for private student loans without affecting your credit score when you use Credible.

How to get the lowest student loan rate

Here are a few strategies that could help you get a good interest rate on a private student loan:

- Have good credit. Your credit score is one of the main factors that will determine the rates you’re offered. You’ll generally need good to excellent credit to qualify for the lowest interest rates — a good credit score is usually considered to be 700 or higher.

- Apply with a cosigner. If you have less-than-perfect credit, applying with a cosigner could make it easier to get approved for a private student loan. Having a creditworthy cosigner might also get you a lower interest rate than you’d get on your own.

- Choose a shorter repayment term. Many lenders offer lower rates for shorter repayment terms. It’s usually a good idea to pick the shortest term you can afford to keep your interest costs as low as possible.

- Compare lender options. It’s important to research and compare your options from as many lenders as possible. This way, you can find the right loan with the most favorable rate for your needs.

How to calculate student loan interest

Before you take out a student loan, it’s important to consider how much that loan will cost you over time. This way, you can be prepared for any added expenses.

You can see what your estimated monthly payment will be along with your total interest costs by using Credible’s student loan calculator.

About the authors: Emily Guy Birken is a Credible authority on student loans and personal finance. Her work has been featured by Forbes, Kiplinger’s, Huffington Post, MSN Money, and The Washington Post online. Matt Carter contributed to the reporting of this article.