With Credible personal loans, you get access to a free online marketplace and dozens of lenders providing same- and next-day loans for debt consolidation, home improvement, medical expenses, and more. You can compare interest rates, loan amounts, and terms — for free, with no effect on your credit score.

Over 60,000 people got a personal loan through the Credible personal loan marketplace last year. There are no appointments, subscription fees, or AI-generated sales pitches — just an online experience dedicated to helping you make the best decision for your personal and financial goals.

What to watch out for

You can prequalify for a personal loan through Credible to see estimated rates and terms without hurting your credit score. But prequalification is an estimate only and not an offer of credit. The rates and terms presented after you apply may differ from your prequalification results — it's also possible that you might not qualify.

And when you apply, most lenders conduct a hard credit check which could temporarily lower your credit score.

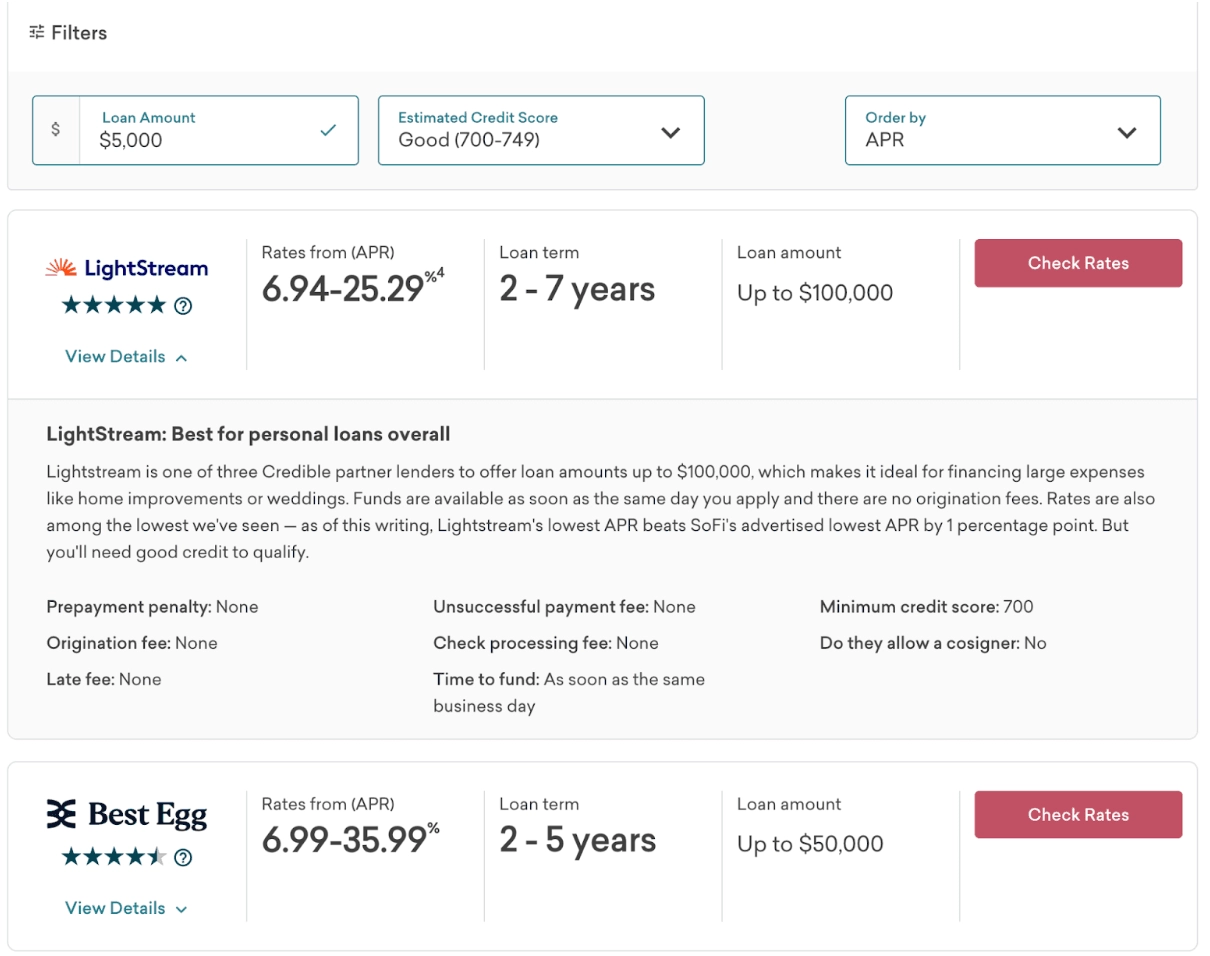

How Credible’s personal loan marketplace works

Credible personal loan marketplace is a one-stop shopping platform to compare personal loans and get customized quotes and answers to all your loan questions.

Our dedicated client success team, along with a library of personal loans content, is at your disposal free of charge. We’ll help you find the right lender — even if you have bad credit — and we’ll point you to loan alternatives if one of our lender partners isn’t right for you.

Compare lenders

Credible partners with more than 20 personal loan lenders. Each is thoroughly vetted and rated on a five-star scale across hundreds of data points according to a methodology that prioritizes low rates, low fees, options for fair and bad credit, and a high level of lender transparency.

You can filter and compare multiple lenders at once, based on essential criteria including:

- Loan APRs (annual percentage rates)

- Minimum and maximum loan amounts

- Minimum credit score requirements

- Loan purposes, such as debt consolidation, credit card financing, and home improvement

- Funding time, or how quickly you can receive your loan after approval

- Repayment terms, or how many years are required to pay back the loan

- Minimum credit score requirements

- Fees, such as origination fees and late fees

- Discounts, such as automatic payment or direct payment to creditors

- Lender pros and cons, objectively evaluated by expert writers and editors

Source: credible.com/personal-loan

If you want to dig even deeper, Credible offers in-depth profiles of dozens of individual lenders, such as LightStream, SoFi, Upstart, and Upgrade.

Good to know

A loan’s APR represents the annual cost of borrowing money based on that loan’s interest rate and any upfront fees. The lowest APRs are reserved for borrowers with excellent credit.

Related: How To Compare Personal Loans: A Step-by-Step Guide

Prequalify

You can prequalify with multiple lenders all at once with Credible, instead of having to visit individual lender websites — saving you time and letting you compare quotes in one place. In fact, some lenders, like BHG Financial and LightStream, don’t offer prequalification on their own websites, but do on Credible’s.

Prequalification is a way to get detailed loan quotes that include APRs, loan amounts, repayment terms, funding times, and fees. Prequalifying for a personal loan through Credible is free and involves a soft credit check, which doesn’t hurt your credit score. (Personal loan prequalification is an estimate, but not an offer of credit. Your final rate and terms could differ.)

When you prequalify through Credible, you’re asked:

- How much you want to borrow

- What you’ll use the loan funds for

- What your employment situation is (as in employed, self-employed, retired, etc.)

- What your annual income is

- For your name and email address

- For your date of birth

- Whether you rent or own

- For your monthly housing payment

- For the last four digits of your Social Security number

Good to know

Any information you agree to share with Credible or its lending partners is encrypted and protected by data security methods designed to keep your information confidential.

Prequalification can go one of two ways:

- If you’ve prequalified successfully with one or more lenders, you can compare quotes and choose the one that best fits your needs. At that point, you’re directed to the chosen lender’s website to complete your application. The lender will review your application and process the loan if an offer is extended and accepted.

- If you don’t meet a lender’s prequalification requirements, Credible will recommend other lending or debt settlement solutions based on your situation and financial criteria.

Get help

Credible's Client Success Team is available throughout the entire process, even after you've accepted a loan offer.

Team members are available by chat, phone, or email to offer assistance in areas including:

- Comparing lenders and prequalification quotes

- Troubleshooting technical issues

- Understanding rates and terms

- Facilitating communications with partner lenders

- How a personal loan affects your credit score

- Advice on managing repayment

How to contact Credible's Client Success Team by phone and email:

- (866) 540-6005: Monday through Thursday 9 a.m. to 9 p.m. ET; Friday 9 a.m. to 5 p.m. ET; Saturday 10 a.m. to 6 p.m. ET

- [email protected]

You can also chat via the Contact Us page.

Manage your debt and monitor your credit

Credible also offers free tools to help you manage debt, track loans and credit cards, and save money:

- Debt tracker: Summarizes your debt, visualizes your payoff timeline, and suggests ways to reduce interest costs.

- Proactive credit score monitoring: Tracks your credit score changes — alerting you when your score improves or if it falls. It also provides insights into factors impacting your score and offers tips to help you improve your credit score.

Common personal loan uses through Credible

Credible's lending partners offer personal loans for a broad range of uses. Borrowers can use personal loans approved through the Credible marketplace for more than 20 purposes, with the most common including:

Don’t forget other purposes that put the “personal” in personal loans, including vacations and weddings.

Learn More: What Are Personal Loans Used For?

What can’t I use a personal loan for?

Lenders typically prohibit using personal loans for certain purposes. Prohibited uses often include the obvious — such as gambling or illegal activity — but many lenders further specify that their personal loans can’t be used for purposes including:

- Cryptocurrency and other forms of investing

- Business expenses

- Making a down payment on a home

- College tuition and other post-secondary education expenses

If you visit the Credible personal loans marketplace in search of a specialty loan, you may be able to find what you’re looking for through Credible Student Loans or Credible Mortgages. These marketplaces also let you compare lenders and get prequalified quotes.

Learn More: What Can't You Use a Personal Loan For?

Good to know

In 2024, over 60,000 people saved money on interest by using the Credible personal loans marketplace.

Pros and cons of Credible personal loans

Depending on your situation, Credible personal loans might or might not be the best option. Here are some of the advantages and potential drawbacks:

Pros

- Credible's marketplace is free to use

- Compare multiple quotes in one place

- Lenders cover the full gamut of credit profiles

- Ratings and reviews are updated regularly

- Prequalify with no impact to your credit score

- Access to closed loans data allows Credible to make more informed recommendations than competitors

- Credible’s editorial team has decades of experience

- Credible’s Client Support Team offers assistance every step of the way

- Free tools for credit and debt management

Cons

- Some lenders have short lists of approved loan uses

- Some lenders have strict eligibility or underwriting requirements

- Credible is not a lender; borrowers need to complete the loan process with the lender

How Credible compares to other personal loan marketplaces

- Only a few other competitors, such as LendingTree, are true personal loan marketplaces with direct lender partnerships, customer support teams, and personal loans data that informs their ratings and recommendations.

- While Credible partners with more than 20 personal loan lenders, some competitors offer fewer options (or even route you to Credible to continue your personal loan journey).

- Loan amounts on most other websites are limited to $100,000. One of Credible’s lending partners, BHG Financial, offers personal loans of up to $250,000.

- Credible offers credit monitoring and debt management tools, plus a robust customer support team available by phone with extended service hours during evenings and weekends.

Credible personal loan requirements

Although lender requirements vary, here’s a list of common documents you may need to submit when you apply for a personal loan:

- Government-issued ID, such as a driver’s license or passport

- Proof of income

- Bank account information

- Tax forms, such as W-2s

Depending on the lender, you may also have to meet certain financial requirements, including:

- Minimum credit score

- Minimum income

- Maximum debt-to-income ratio (DTI), or the percentage of monthly income devoted to debt payments

Good to know

Lenders typically prefer a DTI of less than 36% for personal loans, but some will consider a DTI up to 50%.

How to get a personal loan through Credible

- Research and compare lenders.

- Prequalify with multiple lenders.

- Compare prequalification quotes.

- Select your lender.

- Follow the link to the lender's website to complete your application.

Borrowers who don’t qualify with main lenders may be directed to emergency lenders or debt relief options.

Read More: How To Apply for a Personal Loan

FAQ

Is Credible legit?

Open

How does Credible make money?

Open

How easy is it to get a personal loan from Credible?

Open

How big of a personal loan can I get from Credible?

Open

How long does it take to get a personal loan through Credible?

Open