Our goal is to give you the tools and confidence you need to improve your finances. Although we receive compensation from our partner lenders, whom we will always identify, all opinions are our own. Credible Operations, Inc. NMLS # 1681276, is referred to here as "Credible."

Refinancing is a good idea if:

- You want to save money. By refinancing your student loans, you can typically secure a lower interest rate, and you can save money over the life of your loan.

- Your finances are in good shape. If you have a good credit score and a steady income (or you have a cosigner with a qualifying score and income), you are a great candidate for refinancing. A good FICO credit score is usually considered to be 670 or higher.

Student loan refinancing calculator

Step 1. Enter your loan balance

Step 2. Enter current loan information

Step 3. Enter your new loan information to start calculating your savings

If you refinance your student loan at % interest rate, you can save will pay an additional $ monthly and pay off your loan by . The total cost of the new loan will be $.

Does refinancing make sense for you?

Compare offers from top refinancing lenders to determine your actual savings.

Check Personalized Rates

Checking rates won't affect your credit score

If you know the terms of your loans, you can enter them into the student loan refinancing calculator below to see how much money you might save through refinancing.

Here’s the information you’ll need:

- Loan balance: This is the amount you want to refinance. Keep in mind that you can choose to refinance some or all of your student loans.

- Remaining term: This is the number of years left on your current loan term.

- New loan term: This is the repayment term you’re considering for your new loan. Terms on refinancing loans generally range from 5 to 20 years, depending on the lender.

- Interest rate: In the interest rate fields, enter the interest rate for your current loan and enter the potential interest rate you might have after refinancing your student loan.

- Monthly payment: While the monthly payment will populate automatically after you add the interest rate and loan term, adjusting the amount will show you how increasing or decreasing your payment could affect your loan term and overall cost.

How to decide if you should refinance your student loans

While refinancing could be the best choice in some cases, it isn’t right for everyone. Here are two key factors that can help you decide whether you should refinance your student loans:

1. How much do you owe?

The first step to deciding if refinancing is right for you is knowing how much you owe and what your interest rates are. Here’s how you can check this information, depending on the type of loans you have:

- To find your federal student loan balance: Check your dashboard on StudentAid.gov or with your school’s financial aid office.

- To find your private student loan balance: Check your credit report to find your private lender, then contact them or log in to their site to view your balance.

Learn More: How To Find Your Student Loan Balance

2. What rates can you qualify for?

To be eligible to refinance your student loans at a better interest rate, you’ll typically need a good credit score and steady income. This tells lenders that you should be able to repay your student loans without an issue.

| Lender | Rates from (APR) | Min. credit score | Min. annual income |

|---|---|---|---|

| Fixed:

3.99%+

Variable: 4.31%+ | 720 | $30,000 with cosigner $60,000 without |

|

| Fixed:

5.74%+1

Variable: 5.98%+1 | Does not disclose | $24,000 | |

| Fixed:

6.99%+2

Variable: 6.99%+2 | Does not disclose | Does not disclose | |

| Fixed:

4.15%+5

Variable: 5.22%+5 | 700 | $30,000 |

| Fixed:

4.88%+3

Variable: 4.86%+3 | 680 | $35,000 | |

| Fixed:

5.54%+4

Variable: 7.51%+4 | 670 | $36,000 | |

| Fixed:

6.94%+

7 Variable: N/A | 670 | None | |

| Fixed:

4.54%+

Variable: 4.53%+ | 700 | $40,000 |

| Fixed:

6.2%+

Variable: N/A | 670 | $24,000 | |

| Fixed:

3.99%+

Variable: N/A | 680 | $40,000 |

| Fixed: Check with lender Variable: Check with lender | Does not disclose | Does not disclose |

Compare Rates Now |

|||

All APRs reflect autopay and loyalty discounts where available | 1Citizens Disclosures | 2College Ave Disclosures | 5EDvestinU Disclosures | 3 ELFI Disclosures | 4INvestEd Disclosures | 7ISL Education Lending Disclosures | 8Nelnet Bank Disclosures |

|||

Should I refinance my federal student loans?

While you can refinance both federal and private loans, refinancing federal student loans will cost you access to federal benefits and protections — such as income-driven repayment plans and student loan forgiveness programs.

Consolidating your federal student loans is always encouraged over refinancing. You can consolidate your federal loans into one Direct Consolidation Loan with one monthly payment. By consolidating, the interest rate on your loans is determined by the weighted average of all the rates you’re consolidating, but rounded up to the nearest one-eighth of a percent. Additionally, your repayment term can also be extended up to 30 years.

In some cases, refinancing your federal student loans might be a good idea. Here are a few scenarios where refinancing could be worth it and others where it probably isn’t the best idea:

| Scenario | Should you refinance? |

|---|---|

| You have high interest rates and your credit is strong | Yes, refinancing might make sense |

| You have stable income and want to pay off your loans faster | Yes, refinancing might make sense |

| You know someone with strong credit who is willing to cosign your loan | Yes, refinancing might make sense |

| You’re on track to qualify for loan forgiveness | No, you likely shouldn't refinance |

| You have poor credit and no cosigner | No, you likely shouldn't refinance |

| Your income is low or unstable | No, you likely shouldn't refinance |

Keep Reading: How To Consolidate Your Student Loans

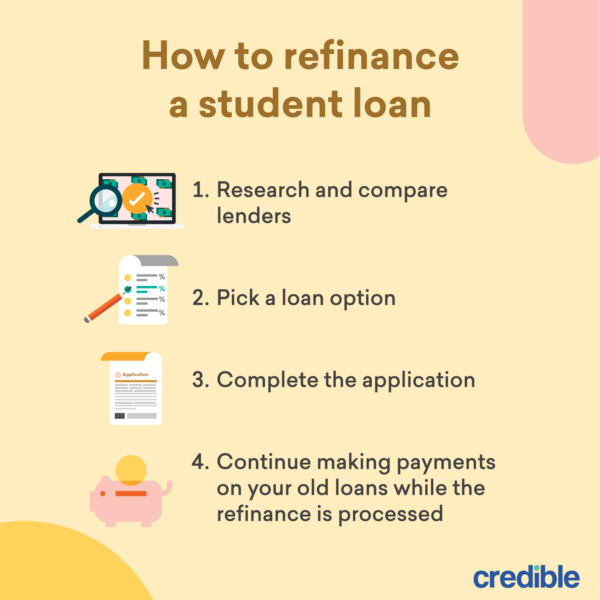

How to refinance your student loans

If you’re ready to refinance your student loans, follow these four steps:

- Research and compare lenders. Your first step should be to compare lenders. Consider key factors, such as interest rate, repayment terms, monthly payment, and fees.

- Pick a loan option. Choose whichever lender best fits your situation.

- Complete the application. Even if you’ve already prequalified, you’ll need to complete an application to refinance. Once the lender does a hard credit pull (which impacts your credit), you’ll find out if you’re approved for the loan.

- Continue making payments on your old loan. You’ll need to keep making your payments on your old loan until your new one is processed. Missing any payments on your current loan can impact your credit.

Check Out: How To Refinance Your Student Loans

Frequently asked questions

Here are the answers to several commonly asked questions about student loan refinancing:

When should I refinance my student loans?

A good time to refinance is when you can qualify for lower interest rates than those on your existing student loans. Typically, this is once you’ve graduated, have a steady job, and have established your credit.

If you don’t qualify to refinance right after graduation on your own, you could be eligible with a cosigner who has strong credit (or you can try again once your financial situation improves). But if you’re still not sure if you qualify, Credible makes it easy to see your prequalified rates from multiple lenders in just two minutes.

Related: Learn more about refinancing your student loans

When you refinance your student loans, you’re likely to see some savings.

Learn More: When To Refinance Student Loans

How much will refinancing my student loans save me?

According to a recent analysis of self-reported data provided by borrowers who refinanced their student loans through Credible, Credible users who refinanced into a shorter term loan saved an average of $16,943 over the life of their new loan.1

But keep in mind the amount you save will depend on your specific situation.

How can I qualify for refinancing?

Qualifying for student loan refinancing depends on a number of factors, like your credit score, debt-to-income ratio (DTI), the school you graduated from, and how much you want to refinance.

Adding a cosigner with strong credit could also improve your chances of prequalifying for a loan. Credible allows you to compare options with different cosigners, so you can see which helps you prequalify with better rates.

Check Out: How To Improve Your Credit

Do I make enough to refinance?

Some lenders have minimum income requirements if you want to refinance your student loans with them. The minimum income varies by lender and the number also depends on whether you have a qualifying cosigner or not. Income is generally considered by lenders as part of their DTI calculation to determine if you have enough to cover your current monthly debts.

However, the most important thing is that you have a steady job and consistent income. This can help show lenders you’re responsible and can pay your loans back.

How often can I refinance my student loans?

Although many refinance their student loans just once, there’s actually no limit to how often you can refinance your student loans. In some situations, refinancing again could help you save even more money than you did when you first refinanced your student loans.

Just make sure it makes sense to refinance a second or even third time. If you can’t get a lower rate, it probably isn’t the best idea for you.

How long before you can refinance student loans?

You can refinance your student loans as soon as you meet the requirements set by the lender, such as having good credit as well as verifiable income. You might also be required to have graduated before you can refinance, depending on the lender.

Some lenders allow borrowers to refinance their loans without a degree or even while they’re still in school. However, keep in mind that many students don’t yet have the required income and credit history to qualify for refinancing. In most cases, you’ll need to build a good credit history, secure a stable income, and possibly graduate (depending on the lender) before you can refinance your student loans.

Other student loan calculators

Here are a couple of other calculators that could come in handy:

Student Loan Interest Calculator

Best for:

- Estimating your monthly student loan payments

- Seeing how much you’ll pay in interest over time

- Checking whether a different interest or loan term will help you save money

Student Loan Repayment Calculator

Best for:

- Estimating how long it will take to pay off your loan

- Checking your expected interest costs

- Seeing how making extra payments could change your payoff date

Related: Learn more about refinancing your student loans

Rates displayed include Automatic Payment and Loyalty Discounts, where applicable. Note that such discounts do not apply while loans are in deferment. The lenders on the Credible.com platform offer fixed rates ranging from 3.39% - 17.99% APR and Variable interest rates from 4.13% - 17.99% APR. Variable rates will fluctuate over the term of the borrower's loan with changes in the Index rate. The Index will be either LIBOR or SOFR. Rates are subject to change at any time without notice. Your actual rate may be different from the rates advertised and/or shown above and will be based on factors such as the term of your loan, your financial history (including your cosigner’s (if any) financial history) and the degree you are in the process of achieving or have achieved. While not always the case, lower rates typically require creditworthy applicants with creditworthy co-signers, graduate degrees, and shorter repayment terms (terms vary by lender and can range from 5-20 years) and include Automatic Payment and Loyalty discounts, where applicable. Loyalty and Automatic Payment discount requirements as well as Lender terms and conditions will vary by lender and therefore, reading each lender’s disclosures is important. Additionally, lenders may have loan minimum and maximum requirements, degree requirements, educational institution requirements, citizenship and residency requirements as well as other lender-specific requirements. Lenders will conduct a hard credit pull when you submit your application. Hard credit pulls will have an impact on your credit